What is Global Lithium Battery Tabs Market?

The Global Lithium Battery Tabs Market is a crucial segment within the broader lithium battery industry, serving as an essential component in the construction of lithium-ion batteries. These tabs are small metal strips that connect the battery cells to the external circuit, facilitating the flow of electricity. They are typically made from materials like aluminum, nickel, and copper, chosen for their excellent conductivity and durability. The market for lithium battery tabs has been expanding rapidly due to the increasing demand for lithium-ion batteries, which are widely used in various applications such as consumer electronics, electric vehicles (EVs), and energy storage systems. The growth in these sectors, particularly the surge in electric vehicle adoption, has significantly driven the demand for efficient and reliable battery components, including tabs. As technology advances, the market continues to evolve, with manufacturers focusing on improving the performance and efficiency of battery tabs to meet the growing energy demands and sustainability goals. This market is characterized by intense competition and innovation, as companies strive to develop advanced materials and designs that enhance battery performance and longevity. The global lithium battery tabs market is poised for continued growth, driven by technological advancements and the increasing shift towards renewable energy sources.

Al Lead Tab, Ni Lead Tab, Ni-Cu Lead Tab in the Global Lithium Battery Tabs Market:

In the Global Lithium Battery Tabs Market, various types of lead tabs are utilized, each offering distinct advantages based on their material composition and application requirements. Al Lead Tabs, or aluminum lead tabs, are commonly used in lithium-ion batteries due to their lightweight nature and excellent conductivity. Aluminum is favored for its ability to efficiently conduct electricity while adding minimal weight to the battery, making it ideal for applications where weight is a critical factor, such as in electric vehicles and portable consumer electronics. The use of aluminum also contributes to cost-effectiveness, as it is generally less expensive than other conductive materials. Ni Lead Tabs, or nickel lead tabs, are another popular choice, particularly valued for their high corrosion resistance and durability. Nickel's robust nature makes it suitable for batteries that are subjected to harsh environmental conditions or require a longer lifespan. This makes Ni Lead Tabs a preferred option in industrial applications and energy storage systems where reliability and longevity are paramount. Ni-Cu Lead Tabs, which combine nickel and copper, offer a balance of the properties found in both materials. Copper is known for its superior electrical conductivity, while nickel provides strength and corrosion resistance. This combination results in a lead tab that can efficiently conduct electricity while withstanding environmental stressors, making it suitable for high-performance applications. The choice between these tabs often depends on the specific requirements of the battery application, such as the need for lightweight materials, cost considerations, or the demand for high durability and conductivity. Manufacturers in the lithium battery tabs market continuously innovate to enhance the performance of these tabs, focusing on improving conductivity, reducing weight, and increasing resistance to environmental factors. This innovation is driven by the growing demand for more efficient and reliable batteries in various sectors, including consumer electronics, electric vehicles, and renewable energy storage. As the market evolves, the development of new materials and technologies is expected to further enhance the capabilities of lithium battery tabs, supporting the broader adoption of lithium-ion batteries across diverse applications. The competition among manufacturers is intense, with companies investing in research and development to create advanced lead tabs that meet the ever-increasing performance standards required by modern battery applications. This competitive landscape fosters innovation and drives the market forward, ensuring that lithium battery tabs continue to play a vital role in the advancement of energy storage technologies.

Consumer Use LIB, EV LIB, Energy Storage LIB in the Global Lithium Battery Tabs Market:

The Global Lithium Battery Tabs Market plays a significant role in various applications, particularly in Consumer Use LIB, EV LIB, and Energy Storage LIB. In consumer electronics, lithium-ion batteries are ubiquitous, powering devices such as smartphones, laptops, and tablets. The demand for lightweight, efficient, and long-lasting batteries in these devices has driven the need for high-quality battery tabs that can ensure optimal performance and reliability. The use of advanced materials in battery tabs helps in achieving the desired conductivity and durability, which are crucial for the seamless operation of consumer electronics. In the realm of electric vehicles (EVs), the importance of lithium battery tabs is even more pronounced. EVs require batteries that can deliver high power output and withstand frequent charging cycles. The efficiency and reliability of battery tabs directly impact the overall performance and range of electric vehicles. As the adoption of EVs continues to rise, driven by environmental concerns and government incentives, the demand for superior battery components, including tabs, is expected to grow significantly. Manufacturers are focusing on developing tabs that can enhance the energy density and longevity of EV batteries, contributing to the broader goal of sustainable transportation. In energy storage systems, lithium-ion batteries are increasingly used to store energy generated from renewable sources such as solar and wind. These systems require batteries that can store large amounts of energy and release it efficiently when needed. The role of battery tabs in these applications is critical, as they must ensure the efficient flow of electricity while withstanding the demands of large-scale energy storage. The development of robust and efficient battery tabs is essential for the advancement of energy storage technologies, which are key to achieving a sustainable energy future. As the global focus shifts towards renewable energy and reducing carbon emissions, the demand for energy storage solutions is expected to rise, further driving the growth of the lithium battery tabs market. Overall, the Global Lithium Battery Tabs Market is integral to the advancement of various technologies that rely on lithium-ion batteries. The continuous innovation and development in this market are crucial for meeting the growing energy demands and supporting the transition towards a more sustainable and energy-efficient future.

Global Lithium Battery Tabs Market Outlook:

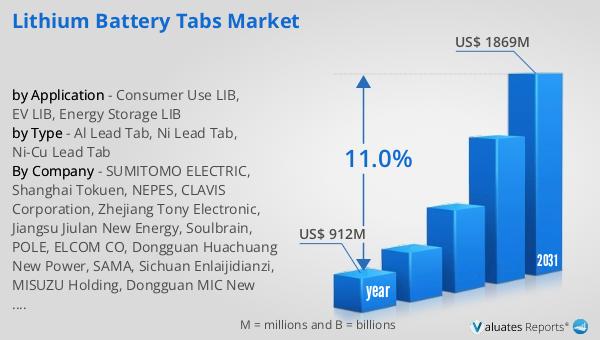

The outlook for the Global Lithium Battery Tabs Market indicates a promising growth trajectory. In 2024, the market was valued at approximately US$ 912 million, and it is anticipated to expand to a revised size of US$ 1869 million by 2031, reflecting a compound annual growth rate (CAGR) of 11.0% over the forecast period. This growth is largely driven by the increasing adoption of new energy vehicles, with global sales projected to reach 14.65 million units in 2023, marking a 35.4% increase from the previous year. Notably, China is expected to play a significant role in this growth, with its new energy vehicle sales reaching 9.49 million units, accounting for 64.8% of the global market. The competitive landscape of the lithium battery tabs market is characterized by the presence of leading companies such as SUMITOMO ELECTRIC, Shanghai Tokuen, NEPES, CLAVIS Corporation, Zhejiang Tony Electronic, Jiangsu Jiulan New Energy, Soulbrain, POLE, and ELCOM CO. Among these, the top five companies hold nearly 46% of the market share, highlighting the concentration of market power among key players. These companies are at the forefront of innovation, continuously striving to enhance the performance and efficiency of battery tabs to meet the evolving demands of the market. As the market continues to grow, driven by technological advancements and the increasing shift towards renewable energy sources, the role of these leading companies will be crucial in shaping the future of the Global Lithium Battery Tabs Market.

| Report Metric | Details |

| Report Name | Lithium Battery Tabs Market |

| Accounted market size in year | US$ 912 million |

| Forecasted market size in 2031 | US$ 1869 million |

| CAGR | 11.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | SUMITOMO ELECTRIC, Shanghai Tokuen, NEPES, CLAVIS Corporation, Zhejiang Tony Electronic, Jiangsu Jiulan New Energy, Soulbrain, POLE, ELCOM CO, Dongguan Huachuang New Power, SAMA, Sichuan Enlaijidianzi, MISUZU Holding, Dongguan MIC New Mstar Technology, Guangdong Zhengyee, Nets Co., Ltd, Gelonlib, Shinhwa IT, Futaba Corporation, Hebei Litonghang, YUJIN TECHNOLOGY |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |