What is Gynaecological Forceps - Global Market?

Gynaecological forceps are specialized medical instruments used primarily in the field of gynecology to assist in various procedures involving the female reproductive system. These instruments are designed to grasp, hold, or manipulate tissues and are essential in surgeries such as childbirth, where they may be used to assist in the delivery of a baby, or in procedures like the removal of fibroids or other growths. The global market for gynaecological forceps is a significant segment within the broader medical devices industry, driven by the increasing demand for advanced healthcare solutions and the rising prevalence of gynecological disorders. As healthcare systems worldwide continue to evolve, there is a growing emphasis on improving women's health, which in turn fuels the demand for specialized instruments like gynaecological forceps. The market is characterized by a wide range of products, from traditional designs to more advanced, ergonomically designed instruments that enhance precision and safety during procedures. Manufacturers are continually innovating to meet the needs of healthcare professionals, ensuring that these tools are both effective and easy to use. The global market for gynaecological forceps is poised for growth as awareness and access to healthcare services expand, particularly in developing regions.

Disposable, Reusable in the Gynaecological Forceps - Global Market:

The global market for gynaecological forceps can be broadly categorized into disposable and reusable types, each with its own set of advantages and considerations. Disposable gynaecological forceps are designed for single-use, offering a high level of convenience and safety by minimizing the risk of cross-contamination and infection. These instruments are particularly favored in settings where sterility is of utmost importance, such as in hospitals and clinics with high patient turnover. The use of disposable forceps eliminates the need for sterilization processes, saving time and resources for healthcare facilities. They are often made from lightweight materials, making them easy to handle and reducing the risk of fatigue for medical professionals during lengthy procedures. However, the environmental impact of disposable medical instruments is a growing concern, as they contribute to medical waste. On the other hand, reusable gynaecological forceps are designed for multiple uses and are typically made from durable materials like stainless steel. These instruments require thorough sterilization between uses to ensure patient safety, which can be resource-intensive but is often more cost-effective in the long run. Reusable forceps are favored in healthcare settings where sustainability and cost management are priorities. They offer the advantage of being more environmentally friendly compared to their disposable counterparts, as they generate less waste. The choice between disposable and reusable forceps often depends on the specific needs and policies of healthcare facilities, as well as considerations related to cost, convenience, and environmental impact. In the global market, both types of forceps are in demand, with manufacturers focusing on innovation to improve the functionality and safety of these instruments. As healthcare systems worldwide strive to balance efficiency, cost, and environmental responsibility, the market for both disposable and reusable gynaecological forceps is expected to continue evolving.

Hospital, Clinic, Other in the Gynaecological Forceps - Global Market:

Gynaecological forceps are utilized in various healthcare settings, including hospitals, clinics, and other medical facilities, each with its own unique requirements and challenges. In hospitals, gynaecological forceps are essential tools in the obstetrics and gynecology departments, where they are used in a wide range of procedures from assisting in childbirth to performing surgeries for conditions like endometriosis or uterine fibroids. Hospitals often have the resources to invest in both disposable and reusable forceps, allowing them to choose the most appropriate type based on the specific procedure and patient needs. The high patient turnover in hospitals necessitates a focus on efficiency and safety, making disposable forceps a popular choice for minimizing infection risks. In clinics, where the scale of operations is typically smaller than in hospitals, the use of gynaecological forceps is still critical for providing quality care. Clinics may opt for reusable forceps to manage costs effectively, especially if they have the necessary sterilization facilities. However, the choice between disposable and reusable forceps in clinics often depends on the volume of patients and the types of procedures performed. Other healthcare settings, such as specialized women's health centers or outpatient surgical centers, also rely on gynaecological forceps for various procedures. These facilities may have specific preferences based on their operational focus and patient demographics. For instance, a center specializing in minimally invasive gynecological surgeries might prioritize advanced, ergonomically designed forceps that enhance precision and reduce the risk of complications. Across all these settings, the demand for gynaecological forceps is driven by the need to provide safe, effective, and efficient care for women. As healthcare systems continue to evolve, the role of gynaecological forceps in improving women's health outcomes remains crucial, with ongoing innovations aimed at enhancing their functionality and safety.

Gynaecological Forceps - Global Market Outlook:

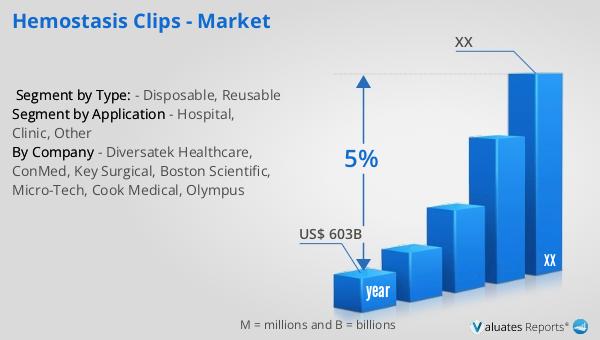

Based on our research, the global market for medical devices, which includes gynaecological forceps, is projected to reach approximately US$ 603 billion in 2023. This expansive market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for advanced medical technologies and the continuous evolution of healthcare systems worldwide. The medical devices market encompasses a wide range of products, from diagnostic equipment to surgical instruments, each playing a vital role in enhancing patient care and outcomes. The projected growth rate reflects the ongoing advancements in medical technology, as well as the rising prevalence of chronic diseases and the aging global population, which drive the need for innovative healthcare solutions. As healthcare providers strive to improve the quality and accessibility of care, the demand for specialized instruments like gynaecological forceps is expected to rise. This growth trajectory underscores the importance of continued investment in research and development to meet the evolving needs of healthcare professionals and patients alike. The global market for medical devices is a dynamic and rapidly evolving sector, with significant opportunities for innovation and expansion in the coming years.

| Report Metric | Details |

| Report Name | Gynaecological Forceps - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | MedGyn, Transact International, Kolplast Group, Lorien Industries, Medline Industries, Adeor Medical AG, Centrel, DTR Medical Ltd, Gyneas, Prince Medical, Parburch Medical, Hangzhou Kangji Medical Instrument Company Limited |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |