What is Global Rail Vehicle Braking System Market?

The Global Rail Vehicle Braking System Market refers to the industry focused on the development, production, and distribution of braking systems specifically designed for rail vehicles. These systems are crucial for ensuring the safety and efficiency of trains, subways, and other rail-based transportation. As rail networks expand and modernize worldwide, the demand for advanced braking systems has increased. These systems are engineered to provide reliable stopping power, enhance passenger safety, and improve the overall performance of rail vehicles. The market encompasses various types of braking technologies, including pneumatic, hydraulic, and electromagnetic systems, each offering unique advantages and applications. The growth of this market is driven by the need for improved rail infrastructure, increased urbanization, and the rising demand for efficient public transportation solutions. As countries invest in upgrading their rail systems to accommodate growing populations and reduce traffic congestion, the Global Rail Vehicle Braking System Market is expected to continue its upward trajectory, offering innovative solutions to meet the evolving needs of the rail industry.

Pneumatic Braking System, Hydraulic Braking System, Electromagnetic Braking System in the Global Rail Vehicle Braking System Market:

The Global Rail Vehicle Braking System Market includes several key technologies, each with its own set of characteristics and applications. The pneumatic braking system is one of the most widely used types in the rail industry. It operates using compressed air to apply pressure to the brake pads, which then create friction against the wheels to slow down or stop the train. This system is favored for its reliability and ease of maintenance. Pneumatic brakes are particularly effective for long trains, as the air pressure can be evenly distributed across multiple cars, ensuring consistent braking performance. However, they require a robust air supply system and regular maintenance to prevent leaks and ensure optimal performance. Hydraulic braking systems, on the other hand, use fluid pressure to activate the brakes. These systems are known for their precision and responsiveness, making them ideal for high-speed trains and applications where quick stopping power is essential. Hydraulic brakes offer smoother operation and can be more efficient than pneumatic systems, but they also require careful maintenance to prevent fluid leaks and ensure system integrity. Electromagnetic braking systems represent a more advanced technology, utilizing magnetic fields to generate braking force. These systems are highly effective for high-speed rail applications, as they provide rapid deceleration without the risk of wheel slippage. Electromagnetic brakes are also quieter and produce less wear on the wheels, extending the lifespan of the rail vehicle components. However, they can be more expensive to install and maintain compared to pneumatic and hydraulic systems. Each of these braking technologies plays a vital role in the Global Rail Vehicle Braking System Market, catering to different needs and preferences within the rail industry. As rail networks continue to evolve, the demand for advanced braking solutions will drive innovation and growth in this market, ensuring that rail transportation remains safe, efficient, and reliable.

Train, Subway in the Global Rail Vehicle Braking System Market:

The Global Rail Vehicle Braking System Market plays a crucial role in the operation of trains and subways, providing essential safety and performance benefits. In the context of trains, braking systems are vital for ensuring the safe and efficient operation of both passenger and freight services. Trains often travel at high speeds and carry significant loads, making reliable braking systems essential for preventing accidents and ensuring passenger safety. Pneumatic braking systems are commonly used in trains due to their ability to provide consistent braking force across long distances. This is particularly important for freight trains, which can be several kilometers long and require uniform braking to prevent derailments. Hydraulic braking systems are also used in high-speed passenger trains, where precision and quick response times are critical. These systems allow for smooth and efficient deceleration, enhancing passenger comfort and safety. Electromagnetic braking systems are increasingly being adopted in modern trains, especially those operating at very high speeds. These systems offer rapid deceleration and reduced wear on the wheels, making them ideal for high-speed rail networks. In subways, braking systems are equally important, as they ensure the safe and efficient operation of urban transit systems. Subways often operate in densely populated areas, where safety and reliability are paramount. Pneumatic braking systems are commonly used in subways due to their reliability and ease of maintenance. These systems provide consistent braking performance, which is essential for maintaining tight schedules and ensuring passenger safety. Hydraulic braking systems are also used in some subway systems, offering precise control and quick response times. This is particularly important in urban environments, where trains must frequently stop and start at stations. Electromagnetic braking systems are also being explored for use in subways, offering the potential for quieter operation and reduced maintenance costs. Overall, the Global Rail Vehicle Braking System Market is essential for the safe and efficient operation of trains and subways, providing a range of technologies to meet the diverse needs of the rail industry. As urbanization continues to drive demand for efficient public transportation, the market for advanced braking systems is expected to grow, offering innovative solutions to enhance the safety and performance of rail networks worldwide.

Global Rail Vehicle Braking System Market Outlook:

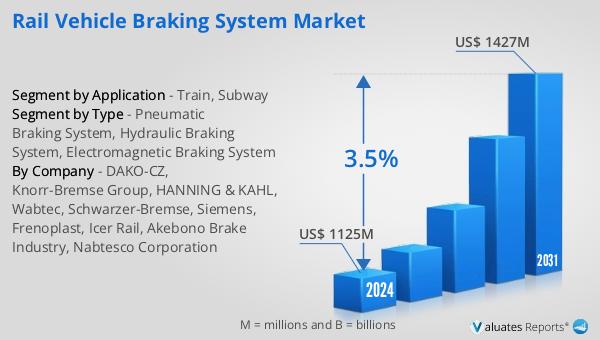

The outlook for the Global Rail Vehicle Braking System Market indicates a promising growth trajectory in the coming years. The market is anticipated to expand from a valuation of US$ 1,125 million in 2024 to approximately US$ 1,427 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.5% from 2025 to 2031. The expansion of this market is largely driven by the increasing demand for critical product segments and the diverse range of end-use applications. As rail networks continue to modernize and expand globally, the need for advanced braking systems becomes more pronounced. These systems are essential for ensuring the safety, efficiency, and reliability of rail transportation, which is becoming increasingly important in urbanized areas. The market's growth is also supported by technological advancements in braking systems, which offer improved performance, reduced maintenance costs, and enhanced safety features. As countries invest in upgrading their rail infrastructure to accommodate growing populations and reduce traffic congestion, the demand for innovative braking solutions is expected to rise. This positive market outlook reflects the ongoing evolution of the rail industry and the critical role that braking systems play in its development.

| Report Metric | Details |

| Report Name | Rail Vehicle Braking System Market |

| Accounted market size in 2024 | US$ 1125 in million |

| Forecasted market size in 2031 | US$ 1427 million |

| CAGR | 3.5% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Sales by Region |

|

| By Company | DAKO-CZ, Knorr-Bremse Group, HANNING & KAHL, Wabtec, Schwarzer-Bremse, Siemens, Frenoplast, Icer Rail, Akebono Brake Industry, Nabtesco Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |