What is Global Viral Conjunctivitis Pipeline Drugs Market?

The Global Viral Conjunctivitis Pipeline Drugs Market refers to the development and potential commercialization of pharmaceutical treatments specifically targeting viral conjunctivitis, an eye condition commonly known as "pink eye." This market encompasses a range of drugs that are in various stages of research and development, aiming to provide effective solutions for this widespread and often uncomfortable condition. Viral conjunctivitis is caused by a viral infection of the eye, leading to symptoms such as redness, itching, and discharge. The pipeline drugs in this market are designed to address these symptoms and potentially reduce the duration and severity of the infection. The market is driven by the increasing prevalence of viral conjunctivitis worldwide, coupled with the demand for more effective and faster-acting treatments. As pharmaceutical companies invest in research and development, the Global Viral Conjunctivitis Pipeline Drugs Market is poised to offer innovative solutions that could significantly improve patient outcomes and quality of life. The market's growth is also fueled by advancements in drug delivery technologies and a better understanding of the viral mechanisms involved in conjunctivitis.

Acute Follicular Conjunctivitis Pipeline Drugs, Subacute Or Chronic Conjunctivitis Pipeline Drugs in the Global Viral Conjunctivitis Pipeline Drugs Market:

Acute Follicular Conjunctivitis Pipeline Drugs are a crucial segment within the Global Viral Conjunctivitis Pipeline Drugs Market. Acute follicular conjunctivitis is characterized by the sudden onset of symptoms such as redness, tearing, and the formation of small follicles on the conjunctiva. These symptoms are often caused by viral infections, making the development of targeted drugs essential. The pipeline drugs for this condition are focused on alleviating symptoms quickly and effectively, reducing the discomfort experienced by patients. Research in this area is exploring various antiviral agents that can inhibit the replication of viruses responsible for the condition. Additionally, there is a focus on developing drugs that can modulate the immune response to prevent excessive inflammation, which can exacerbate symptoms. The development of these drugs involves rigorous clinical trials to ensure their safety and efficacy, with the ultimate goal of providing a reliable treatment option for patients suffering from acute follicular conjunctivitis. Subacute or Chronic Conjunctivitis Pipeline Drugs represent another important area of focus within the Global Viral Conjunctivitis Pipeline Drugs Market. Unlike acute conjunctivitis, subacute or chronic conjunctivitis persists for a longer duration, often leading to prolonged discomfort and potential complications if left untreated. The pipeline drugs for this condition aim to provide long-term relief and prevent recurrence. Researchers are investigating a variety of therapeutic approaches, including antiviral medications that target specific viral strains known to cause chronic conjunctivitis. Additionally, there is interest in developing drugs that can enhance the body's natural defense mechanisms, promoting faster recovery and reducing the likelihood of chronic symptoms. The development of these drugs requires a comprehensive understanding of the underlying viral and immunological factors contributing to chronic conjunctivitis. Clinical trials are essential to determine the optimal dosing regimens and to assess the long-term safety and effectiveness of these treatments. As the Global Viral Conjunctivitis Pipeline Drugs Market continues to evolve, the development of drugs for subacute or chronic conjunctivitis holds promise for improving patient outcomes and reducing the burden of this persistent condition.

Hospitals, Clinics, Others in the Global Viral Conjunctivitis Pipeline Drugs Market:

The usage of Global Viral Conjunctivitis Pipeline Drugs Market in hospitals, clinics, and other healthcare settings is pivotal in managing and treating viral conjunctivitis effectively. In hospitals, these drugs are often used in emergency departments and ophthalmology units to provide immediate relief to patients presenting with severe symptoms. The availability of effective pipeline drugs can significantly reduce the duration of hospital stays and prevent the spread of infection within the hospital environment. In clinics, these drugs are essential for outpatient management of viral conjunctivitis. They allow healthcare providers to offer targeted treatments that address the specific viral cause of the condition, improving patient outcomes and satisfaction. Clinics often serve as the first point of contact for patients experiencing conjunctivitis symptoms, making the availability of effective pipeline drugs crucial for timely intervention. In addition to hospitals and clinics, the Global Viral Conjunctivitis Pipeline Drugs Market also finds application in other healthcare settings, such as community health centers and telemedicine platforms. Community health centers play a vital role in providing accessible healthcare services to underserved populations, and the availability of pipeline drugs for viral conjunctivitis can enhance the quality of care offered. Telemedicine platforms have gained prominence in recent years, allowing patients to consult with healthcare providers remotely. The integration of pipeline drugs into telemedicine services enables healthcare professionals to prescribe effective treatments without the need for in-person visits, increasing convenience for patients and reducing the risk of spreading infection. Overall, the usage of Global Viral Conjunctivitis Pipeline Drugs Market in various healthcare settings underscores the importance of developing effective treatments for viral conjunctivitis. These drugs not only improve patient outcomes but also contribute to the efficient functioning of healthcare systems by reducing the burden of conjunctivitis-related complications and hospitalizations. As the market continues to evolve, the integration of pipeline drugs into diverse healthcare settings will play a crucial role in enhancing the management and treatment of viral conjunctivitis.

Global Viral Conjunctivitis Pipeline Drugs Market Outlook:

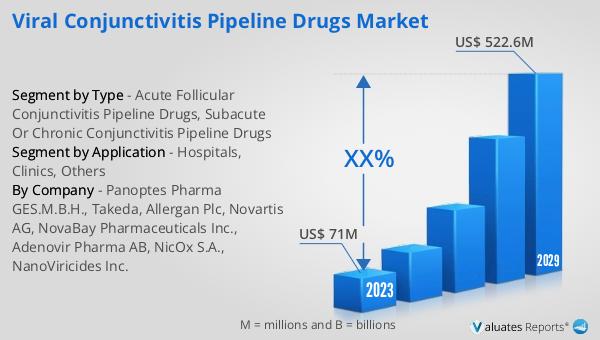

The outlook for the Global Viral Conjunctivitis Pipeline Drugs Market indicates a significant growth trajectory. In 2024, the market was valued at approximately $96 million, and it is anticipated to expand to a revised size of $960 million by 2031. This growth represents a compound annual growth rate (CAGR) of 39.5% over the forecast period. This rapid expansion is indicative of the increasing demand for effective treatments for viral conjunctivitis and the ongoing advancements in pharmaceutical research and development. In comparison, the global pharmaceutical market was valued at $1,475 billion in 2022, with a projected CAGR of 5% over the next six years. This highlights the relatively faster growth rate of the Viral Conjunctivitis Pipeline Drugs Market, driven by the urgent need for innovative solutions to address this common eye condition. Additionally, the chemical drug market is estimated to grow from $1,005 billion in 2018 to $1,094 billion in 2022, further emphasizing the dynamic nature of the pharmaceutical industry. The substantial growth of the Global Viral Conjunctivitis Pipeline Drugs Market underscores the importance of continued investment in research and development to meet the evolving needs of patients and healthcare providers.

| Report Metric | Details |

| Report Name | Viral Conjunctivitis Pipeline Drugs Market |

| Accounted market size in year | US$ 96 million |

| Forecasted market size in 2031 | US$ 960 million |

| CAGR | 39.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Panoptes Pharma GES.M.B.H., Takeda, Allergan Plc, Novartis AG, NovaBay Pharmaceuticals Inc., Adenovir Pharma AB, NicOx S.A., NanoViricides Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |