What is Global Vacuum Gauge Controllers Market?

The Global Vacuum Gauge Controllers Market is an essential segment within the broader instrumentation and control industry. These devices are crucial for measuring and controlling vacuum pressure in various industrial applications. Vacuum gauge controllers are used to ensure that processes requiring specific vacuum conditions are maintained accurately, which is vital for the quality and efficiency of production in industries such as semiconductor manufacturing, pharmaceuticals, and food processing. The market for these controllers is driven by the increasing demand for precision and reliability in vacuum measurement, as well as advancements in technology that allow for more accurate and user-friendly devices. As industries continue to automate and optimize their processes, the need for sophisticated vacuum gauge controllers is expected to grow. These controllers not only help in maintaining the desired vacuum levels but also provide data that can be used for process optimization and quality control. The global market is characterized by a mix of established players and new entrants, all striving to offer innovative solutions that meet the evolving needs of their customers. The market's growth is also supported by the increasing adoption of vacuum technology in emerging economies, where industrialization is on the rise.

Single Measurement Channel, Multi Measurement Channels in the Global Vacuum Gauge Controllers Market:

In the Global Vacuum Gauge Controllers Market, devices are categorized based on their measurement channels, primarily into single measurement channel and multi-measurement channels. Single measurement channel vacuum gauge controllers are designed to monitor and control vacuum pressure at a single point. These are typically used in applications where the vacuum environment is relatively simple and does not require monitoring at multiple points. Single channel controllers are often more cost-effective and easier to operate, making them suitable for small-scale operations or applications where budget constraints are a consideration. They provide precise measurements and control for processes that do not require complex monitoring, ensuring that the vacuum conditions are maintained within the desired range. On the other hand, multi-measurement channel vacuum gauge controllers are designed to handle more complex environments where multiple points of vacuum measurement are necessary. These controllers are capable of monitoring and controlling vacuum pressure at several points simultaneously, making them ideal for large-scale industrial applications where different parts of a process may require different vacuum conditions. Multi-channel controllers are often used in industries such as semiconductor manufacturing, where precise control of vacuum conditions at multiple stages of production is critical. They offer the advantage of centralized control and monitoring, which can lead to improved process efficiency and reduced downtime. The choice between single and multi-measurement channel controllers depends largely on the specific requirements of the application, including the complexity of the vacuum environment, the level of precision required, and budget considerations. As technology advances, both types of controllers are becoming more sophisticated, with features such as digital displays, remote monitoring capabilities, and integration with other control systems. This evolution is driven by the need for greater accuracy, ease of use, and the ability to integrate with modern industrial automation systems. The market for vacuum gauge controllers is expected to continue evolving as industries seek more efficient and reliable ways to manage their vacuum processes. Manufacturers are focusing on developing controllers that offer enhanced functionality, such as the ability to interface with other process control systems and provide real-time data for process optimization. This trend is likely to drive innovation in both single and multi-measurement channel controllers, as companies strive to meet the diverse needs of their customers.

Semiconductor, Optical, Aerospace, Others in the Global Vacuum Gauge Controllers Market:

The Global Vacuum Gauge Controllers Market finds extensive usage across various industries, including semiconductor, optical, aerospace, and others. In the semiconductor industry, vacuum gauge controllers are critical for maintaining the precise vacuum conditions required during the manufacturing of semiconductor devices. The production of semiconductors involves several processes that require different vacuum levels, such as deposition, etching, and lithography. Vacuum gauge controllers ensure that these processes are carried out under optimal conditions, which is essential for the quality and performance of the final product. In the optical industry, vacuum gauge controllers are used in the production of optical components such as lenses and mirrors. These components often require coatings that are applied in vacuum environments to ensure uniformity and adherence. Accurate vacuum measurement and control are crucial in these processes to achieve the desired optical properties and performance. In the aerospace industry, vacuum gauge controllers are used in various applications, including the testing and manufacturing of components that must withstand extreme conditions. For example, vacuum environments are used to simulate the conditions of outer space during the testing of spacecraft components. Vacuum gauge controllers ensure that these tests are conducted under precise conditions, providing valuable data for the development and validation of aerospace technologies. Beyond these industries, vacuum gauge controllers are also used in a variety of other applications, such as in the production of vacuum-packaged food products, pharmaceuticals, and in scientific research. In the food industry, vacuum packaging is used to extend the shelf life of products by removing air and preventing the growth of microorganisms. Vacuum gauge controllers ensure that the packaging process is carried out under the correct conditions, preserving the quality and safety of the food. In pharmaceuticals, vacuum environments are used in processes such as freeze-drying, where precise control of vacuum conditions is essential for the stability and efficacy of the final product. In scientific research, vacuum gauge controllers are used in experiments that require controlled vacuum environments, such as in the study of materials and chemical reactions. The versatility and importance of vacuum gauge controllers across these diverse applications highlight their critical role in modern industry. As technology continues to advance, the demand for more sophisticated and reliable vacuum gauge controllers is expected to grow, driving innovation and development in this market.

Global Vacuum Gauge Controllers Market Outlook:

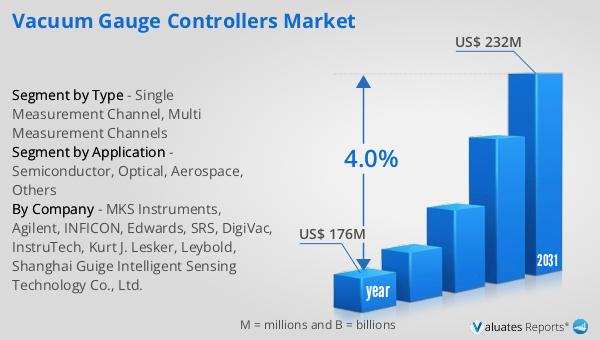

The global market for vacuum gauge controllers, which was valued at $176 million in 2024, is anticipated to expand to a revised size of $232 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.0% over the forecast period. This growth trajectory underscores the increasing demand for vacuum gauge controllers across various industries, driven by the need for precise vacuum measurement and control in complex industrial processes. The market's expansion is fueled by advancements in technology that enhance the accuracy, reliability, and user-friendliness of these devices. As industries continue to automate and optimize their processes, the role of vacuum gauge controllers becomes even more critical, ensuring that vacuum conditions are maintained accurately and efficiently. The growth in this market is also supported by the rising adoption of vacuum technology in emerging economies, where industrialization is rapidly progressing. This trend is expected to create new opportunities for manufacturers and suppliers of vacuum gauge controllers, as they strive to meet the evolving needs of their customers. The market's future looks promising, with continued innovation and development expected to drive further growth and expansion.

| Report Metric | Details |

| Report Name | Vacuum Gauge Controllers Market |

| Accounted market size in year | US$ 176 million |

| Forecasted market size in 2031 | US$ 232 million |

| CAGR | 4.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | MKS Instruments, Agilent, INFICON, Edwards, SRS, DigiVac, InstruTech, Kurt J. Lesker, Leybold, Shanghai Guige Intelligent Sensing Technology Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |