What is Global Lightweight Bogie Market?

The Global Lightweight Bogie Market refers to the industry focused on the production and distribution of lightweight bogies, which are essential components of railway vehicles. Bogies are the wheel assemblies that support the train's body, allowing it to move smoothly along the tracks. Lightweight bogies are specifically designed to reduce the overall weight of the train, which can lead to increased energy efficiency, reduced wear and tear on the tracks, and improved speed and performance. These bogies are typically made from advanced materials such as aluminum alloys, composites, and high-strength steels, which offer a balance of strength and weight reduction. The demand for lightweight bogies is driven by the growing need for efficient and sustainable transportation solutions, as well as the expansion of railway networks worldwide. As urbanization continues to rise, there is an increasing emphasis on developing rail systems that are not only cost-effective but also environmentally friendly. This market is characterized by continuous innovation and technological advancements, as manufacturers strive to meet the evolving needs of the rail industry. The Global Lightweight Bogie Market plays a crucial role in shaping the future of rail transportation by providing solutions that enhance the efficiency and sustainability of train operations.

2-axle Bogies, 3-axle Bogies, Others in the Global Lightweight Bogie Market:

In the Global Lightweight Bogie Market, different types of bogies are utilized to meet various operational requirements, including 2-axle bogies, 3-axle bogies, and others. Each type of bogie offers distinct advantages and is chosen based on the specific needs of the railway system. 2-axle bogies are the most common type and are widely used in passenger and freight trains. They consist of two axles, each with a pair of wheels, and are known for their simplicity and cost-effectiveness. These bogies are suitable for a wide range of applications, including commuter trains, regional trains, and light rail vehicles. Their lightweight design helps reduce energy consumption and track wear, making them an ideal choice for urban and suburban rail networks. On the other hand, 3-axle bogies are typically used in heavy-duty applications, such as freight trains and high-speed trains. They provide additional stability and load-bearing capacity, which is essential for transporting heavy goods or operating at high speeds. The extra axle allows for better weight distribution, reducing the stress on individual wheels and improving the overall performance of the train. 3-axle bogies are often equipped with advanced suspension systems to enhance ride comfort and minimize vibrations. In addition to 2-axle and 3-axle bogies, there are other specialized bogies designed for specific applications. For example, articulated bogies are used in articulated trains, where multiple train cars are connected with a shared bogie. This design allows for smoother transitions between cars and improved maneuverability on curves. Another example is the tilting bogie, which is used in trains that operate on routes with sharp curves. These bogies can tilt the train body to counteract the centrifugal force, allowing for higher speeds and improved passenger comfort. The choice of bogie type depends on various factors, including the type of train, the track conditions, and the operational requirements. Manufacturers in the Global Lightweight Bogie Market are continuously innovating to develop bogies that offer improved performance, reduced maintenance costs, and enhanced safety features. As the demand for efficient and sustainable rail transportation continues to grow, the market for lightweight bogies is expected to expand, with a focus on developing solutions that meet the diverse needs of the rail industry.

Underground Subway, Elevated Subway in the Global Lightweight Bogie Market:

The Global Lightweight Bogie Market plays a significant role in the development and operation of underground and elevated subway systems. These systems are crucial for urban transportation, providing efficient and reliable transit solutions for millions of commuters worldwide. In underground subways, lightweight bogies are essential for ensuring smooth and efficient train operations. The reduced weight of these bogies helps minimize energy consumption, which is particularly important in underground environments where ventilation and energy efficiency are critical concerns. Lightweight bogies also contribute to reduced track wear, which is essential for maintaining the infrastructure of underground subway systems. The use of advanced materials and innovative designs in lightweight bogies enhances their durability and performance, ensuring reliable service in the demanding conditions of underground transit. Elevated subways, on the other hand, benefit from lightweight bogies in terms of structural efficiency and operational performance. The reduced weight of the bogies allows for lighter train cars, which in turn reduces the load on the elevated structures. This is particularly important in urban areas where space is limited, and the construction of heavy infrastructure can be challenging. Lightweight bogies also contribute to improved acceleration and braking performance, which is essential for maintaining efficient service on elevated subway lines. The use of lightweight bogies in both underground and elevated subway systems is driven by the need for sustainable and efficient transportation solutions. As cities continue to grow and urbanize, the demand for reliable and efficient public transit systems is increasing. The Global Lightweight Bogie Market is at the forefront of this development, providing innovative solutions that enhance the performance and sustainability of subway systems. Manufacturers are continuously working to improve the design and materials used in lightweight bogies, ensuring they meet the evolving needs of urban transit systems. The focus is on developing bogies that offer a balance of strength, weight reduction, and durability, ensuring they can withstand the demanding conditions of subway operations. As the market for lightweight bogies continues to grow, it is expected to play a crucial role in shaping the future of urban transportation, providing solutions that enhance the efficiency and sustainability of subway systems worldwide.

Global Lightweight Bogie Market Outlook:

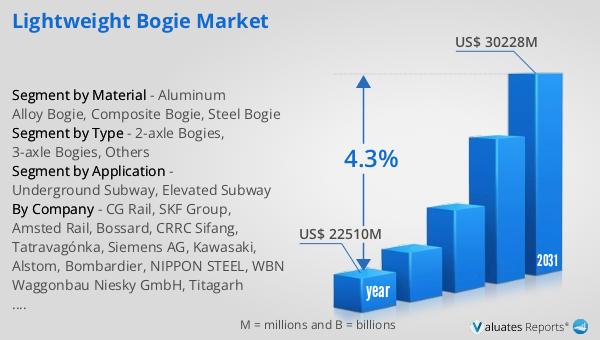

The global market for lightweight bogies was valued at approximately $22,510 million in 2024. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an estimated size of $30,228 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.3% during the forecast period. The increasing demand for lightweight bogies is driven by the need for more efficient and sustainable rail transportation solutions. As urbanization continues to rise, there is a growing emphasis on developing rail systems that are not only cost-effective but also environmentally friendly. Lightweight bogies play a crucial role in achieving these goals by reducing the overall weight of trains, which in turn leads to improved energy efficiency and reduced wear and tear on the tracks. The market is characterized by continuous innovation and technological advancements, as manufacturers strive to meet the evolving needs of the rail industry. The focus is on developing bogies that offer a balance of strength, weight reduction, and durability, ensuring they can withstand the demanding conditions of rail operations. As the market for lightweight bogies continues to expand, it is expected to play a crucial role in shaping the future of rail transportation, providing solutions that enhance the efficiency and sustainability of train operations.

| Report Metric | Details |

| Report Name | Lightweight Bogie Market |

| Accounted market size in year | US$ 22510 million |

| Forecasted market size in 2031 | US$ 30228 million |

| CAGR | 4.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Material |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | CG Rail, SKF Group, Amsted Rail, Bossard, CRRC Sifang, Tatravagónka, Siemens AG, Kawasaki, Alstom, Bombardier, NIPPON STEEL, WBN Waggonbau Niesky GmbH, Titagarh Wagons, Jiangsu Railteco Equipment, Ganz Motor, PROMEC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |