What is Global Dual Channel IP Encoder Market?

The Global Dual Channel IP Encoder Market is a specialized segment within the broader field of digital communication technology. This market focuses on devices known as dual channel IP encoders, which are essential for converting analog video signals into digital IP streams. These encoders are pivotal in various applications, including broadcasting, surveillance, and multimedia streaming, as they enable the efficient transmission of high-quality video over IP networks. The dual channel feature allows these encoders to handle two separate video inputs simultaneously, making them highly versatile and efficient for users who need to manage multiple video feeds. This capability is particularly valuable in environments where space and resources are limited, yet there is a need for robust video processing and transmission. The market for these devices is driven by the increasing demand for high-definition video content and the growing adoption of IP-based communication systems across various industries. As technology continues to evolve, the Global Dual Channel IP Encoder Market is expected to expand, offering more advanced features and improved performance to meet the diverse needs of its users.

in the Global Dual Channel IP Encoder Market:

In the Global Dual Channel IP Encoder Market, various types of encoders are utilized by customers based on their specific needs and applications. One of the primary types is the hardware-based encoder, which is known for its reliability and performance. These encoders are typically used in professional broadcasting environments where high-quality video transmission is crucial. They are designed to handle large volumes of data and provide consistent performance, making them ideal for live broadcasts and other real-time applications. Another type is the software-based encoder, which offers flexibility and scalability. These encoders are often used in environments where cost-effectiveness and adaptability are important. They can be easily updated and configured to meet changing requirements, making them suitable for a wide range of applications, from small-scale video streaming to large-scale broadcasting. Additionally, there are hybrid encoders that combine the features of both hardware and software encoders. These devices offer the best of both worlds, providing high performance and flexibility. They are often used in complex environments where multiple video feeds need to be managed efficiently. Customers also have the option to choose between different compression standards, such as H.264 and H.265, depending on their specific needs. H.264 is widely used due to its balance between quality and compression efficiency, while H.265 offers improved compression, making it suitable for high-definition and ultra-high-definition video. The choice of encoder type and compression standard depends on various factors, including the intended application, budget, and technical requirements. For instance, a broadcasting company may prioritize high-quality video and opt for a hardware-based encoder with H.265 compression, while a small business may choose a software-based encoder with H.264 compression for cost-effectiveness. The Global Dual Channel IP Encoder Market offers a wide range of options to cater to the diverse needs of its customers, ensuring that they can find the right solution for their specific requirements.

Broadcasting and Television Projects, Multimedia Conference Halls, Combination of Large-Screen Display Engineering, TV Teaching, Others in the Global Dual Channel IP Encoder Market:

The Global Dual Channel IP Encoder Market finds extensive usage in various areas, including broadcasting and television projects, multimedia conference halls, large-screen display engineering, TV teaching, and other applications. In broadcasting and television projects, dual channel IP encoders are essential for transmitting high-quality video content over IP networks. They enable broadcasters to deliver live and on-demand video content to a wide audience, ensuring that viewers receive a seamless and high-definition viewing experience. These encoders are also used in television studios to manage multiple video feeds, allowing for efficient production and distribution of content. In multimedia conference halls, dual channel IP encoders play a crucial role in facilitating communication and collaboration. They enable the transmission of video and audio signals over IP networks, allowing participants to engage in real-time discussions and presentations. This is particularly important in large conference settings where participants may be located in different parts of the world. The ability to handle multiple video feeds simultaneously makes these encoders ideal for complex conference setups. In the field of large-screen display engineering, dual channel IP encoders are used to manage and transmit video content to large displays, such as those used in stadiums, concert halls, and public events. They ensure that high-quality video is delivered to the audience, enhancing the overall viewing experience. In TV teaching, these encoders are used to transmit educational content to students in remote locations. They enable educators to deliver lectures and presentations in real-time, ensuring that students receive high-quality video and audio. This is particularly important in distance learning environments where students rely on digital communication tools to access educational content. Overall, the Global Dual Channel IP Encoder Market provides essential solutions for a wide range of applications, ensuring that users can transmit high-quality video content efficiently and effectively.

Global Dual Channel IP Encoder Market Outlook:

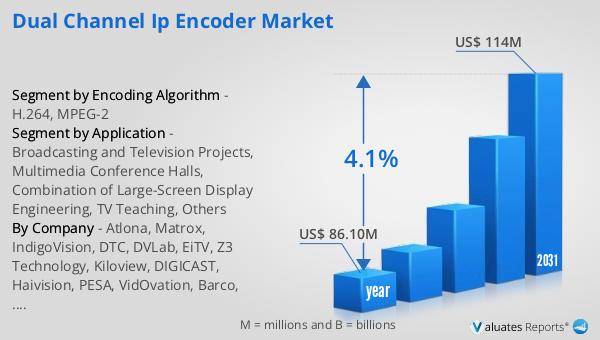

The global market for Dual Channel IP Encoder was valued at $86.10 million in 2024 and is anticipated to grow to a revised size of $114 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.1% during the forecast period. This growth trajectory underscores the increasing demand for dual channel IP encoders across various industries. The market's expansion is driven by the rising need for high-quality video transmission solutions that can handle multiple video feeds simultaneously. As more industries adopt IP-based communication systems, the demand for efficient and reliable video encoding solutions continues to grow. The dual channel feature of these encoders makes them particularly attractive to users who require the ability to manage multiple video inputs without compromising on quality or performance. This is especially important in industries such as broadcasting, where the ability to deliver high-definition video content to a wide audience is crucial. Additionally, the growing popularity of remote work and virtual collaboration has further fueled the demand for dual channel IP encoders, as they enable seamless communication and collaboration across different locations. As the market continues to evolve, it is expected to offer more advanced features and improved performance, catering to the diverse needs of its users.

| Report Metric | Details |

| Report Name | Dual Channel IP Encoder Market |

| Accounted market size in year | US$ 86.10 million |

| Forecasted market size in 2031 | US$ 114 million |

| CAGR | 4.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Encoding Algorithm |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Atlona, Matrox, IndigoVision, DTC, DVLab, EiTV, Z3 Technology, Kiloview, DIGICAST, Haivision, PESA, VidOvation, Barco, Advanced Micro Peripherals, Kramer, SOUKA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |