What is Global Workflow Orchestration Platform Market?

The Global Workflow Orchestration Platform Market is a rapidly evolving sector that focuses on streamlining and automating complex business processes across various industries. These platforms are designed to coordinate and manage the flow of tasks, data, and resources within an organization, ensuring that operations run smoothly and efficiently. By integrating various applications and systems, workflow orchestration platforms help businesses reduce manual intervention, minimize errors, and improve overall productivity. They provide a centralized framework that allows organizations to automate repetitive tasks, manage workloads, and optimize resource allocation. As businesses continue to embrace digital transformation, the demand for workflow orchestration platforms is expected to grow, driven by the need for enhanced operational efficiency and agility. These platforms are particularly valuable in industries such as IT, healthcare, finance, and manufacturing, where complex processes and large volumes of data require seamless coordination. By leveraging advanced technologies like artificial intelligence and machine learning, workflow orchestration platforms can adapt to changing business needs and provide real-time insights, enabling organizations to make informed decisions and stay competitive in a rapidly changing market landscape.

Business Orchestration Platform, Data Orchestration Platform, Others in the Global Workflow Orchestration Platform Market:

The Global Workflow Orchestration Platform Market is composed of several key components, each serving a distinct purpose in the orchestration of business processes. The Business Orchestration Platform is a crucial element, focusing on aligning and automating business processes to achieve strategic objectives. It integrates various business applications and systems, enabling seamless communication and collaboration across departments. This platform is essential for organizations looking to streamline operations, reduce costs, and enhance productivity. By automating routine tasks and providing real-time insights, the Business Orchestration Platform helps businesses make informed decisions and respond quickly to market changes. On the other hand, the Data Orchestration Platform is designed to manage and optimize the flow of data across an organization. It ensures that data is collected, processed, and delivered efficiently, enabling businesses to derive valuable insights and make data-driven decisions. This platform is particularly important in industries where data plays a critical role, such as finance, healthcare, and retail. By automating data workflows and integrating disparate data sources, the Data Orchestration Platform helps organizations improve data quality, reduce latency, and enhance decision-making capabilities. In addition to these core components, the Global Workflow Orchestration Platform Market also includes other specialized platforms that cater to specific industry needs. These platforms may focus on areas such as IT process automation, customer service management, or supply chain optimization. By providing tailored solutions, these platforms help organizations address unique challenges and achieve their business goals. Overall, the Global Workflow Orchestration Platform Market is characterized by its ability to enhance operational efficiency, improve collaboration, and drive innovation across various industries.

Large Enterprises, SMEs in the Global Workflow Orchestration Platform Market:

The usage of Global Workflow Orchestration Platform Market varies significantly between large enterprises and small to medium-sized enterprises (SMEs), each leveraging the technology to meet their unique operational needs. Large enterprises, with their complex and expansive operations, benefit immensely from workflow orchestration platforms by achieving greater efficiency and scalability. These platforms enable large organizations to automate and streamline a multitude of processes across different departments, from IT and finance to human resources and customer service. By integrating disparate systems and applications, large enterprises can ensure seamless communication and data flow, reducing the risk of errors and enhancing productivity. Moreover, workflow orchestration platforms provide large enterprises with the ability to manage and optimize resources effectively, ensuring that tasks are completed on time and within budget. This is particularly important for large organizations that operate in multiple locations and need to coordinate activities across various time zones. On the other hand, SMEs utilize workflow orchestration platforms to enhance their agility and competitiveness in the market. For SMEs, these platforms offer a cost-effective solution to automate routine tasks and improve operational efficiency without the need for significant investment in IT infrastructure. By leveraging workflow orchestration platforms, SMEs can focus on their core business activities and respond quickly to market changes. These platforms also provide SMEs with valuable insights into their operations, enabling them to make data-driven decisions and optimize their processes. Additionally, workflow orchestration platforms help SMEs improve customer service by ensuring timely and accurate delivery of products and services. Overall, the Global Workflow Orchestration Platform Market plays a crucial role in helping both large enterprises and SMEs achieve their business objectives by enhancing efficiency, reducing costs, and driving innovation.

Global Workflow Orchestration Platform Market Outlook:

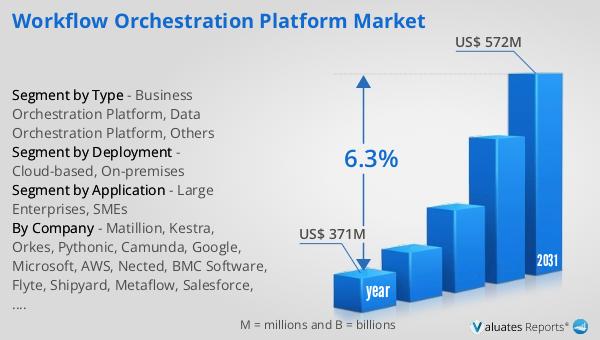

In 2024, the global market for Workflow Orchestration Platforms was valued at approximately $371 million. Looking ahead, this market is anticipated to expand significantly, reaching an estimated value of $572 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 6.3% over the forecast period. The increasing demand for workflow orchestration platforms is driven by the need for businesses to enhance operational efficiency, reduce costs, and improve productivity. As organizations continue to embrace digital transformation, the adoption of workflow orchestration platforms is expected to rise, enabling businesses to automate complex processes and optimize resource allocation. These platforms provide a centralized framework for managing and coordinating tasks, data, and resources, ensuring seamless communication and collaboration across departments. By integrating various applications and systems, workflow orchestration platforms help organizations reduce manual intervention, minimize errors, and improve overall performance. As a result, businesses can respond quickly to market changes, make informed decisions, and stay competitive in a rapidly evolving market landscape. The projected growth of the Global Workflow Orchestration Platform Market underscores the increasing importance of these platforms in driving innovation and achieving strategic business objectives.

| Report Metric | Details |

| Report Name | Workflow Orchestration Platform Market |

| Accounted market size in year | US$ 371 million |

| Forecasted market size in 2031 | US$ 572 million |

| CAGR | 6.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Deployment |

|

| Segment by Application |

|

| By Region |

|

| By Company | Matillion, Kestra, Orkes, Pythonic, Camunda, Google, Microsoft, AWS, Nected, BMC Software, Flyte, Shipyard, Metaflow, Salesforce, Cflow, Prefect, Cloudbees, Synergetics, Process Street, Kyndryl, Rivery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |