What is DNA Synthesizer- Global Market?

The DNA synthesizer global market is a rapidly evolving sector that plays a crucial role in the field of biotechnology and genetic research. DNA synthesizers are sophisticated instruments used to create artificial DNA sequences, which are essential for various applications such as genetic engineering, molecular biology, and synthetic biology. These devices enable scientists to design and produce specific DNA sequences with high precision, facilitating advancements in medical research, drug development, and agricultural biotechnology. The global market for DNA synthesizers is driven by the increasing demand for personalized medicine, advancements in genomics, and the growing need for synthetic biology applications. As researchers continue to explore the potential of DNA synthesis in various fields, the market is expected to witness significant growth. The development of more efficient and cost-effective synthesizers is also contributing to the expansion of this market, making DNA synthesis more accessible to laboratories and research institutions worldwide. With ongoing technological advancements and increasing investments in genetic research, the DNA synthesizer global market is poised for continued growth and innovation.

Laboratory Type, Industrial Type in the DNA Synthesizer- Global Market:

The DNA synthesizer global market can be broadly categorized into two main types: laboratory type and industrial type. Laboratory-type DNA synthesizers are primarily used in research and academic settings. These synthesizers are designed to meet the needs of scientists and researchers who require precise and customizable DNA sequences for their experiments. Laboratory DNA synthesizers are typically smaller in size and offer a range of features that allow for flexibility in DNA sequence design. They are essential tools for genetic research, enabling scientists to explore new genetic pathways, study gene functions, and develop innovative solutions for various biological challenges. On the other hand, industrial-type DNA synthesizers are designed for large-scale production and commercial applications. These synthesizers are used by biotechnology companies, pharmaceutical manufacturers, and other industries that require high-throughput DNA synthesis. Industrial DNA synthesizers are capable of producing large quantities of DNA sequences with high accuracy and efficiency, making them ideal for applications such as drug development, diagnostics, and agricultural biotechnology. The industrial DNA synthesizer market is driven by the increasing demand for synthetic DNA in various industries, as well as the need for cost-effective and scalable DNA synthesis solutions. As the global market for DNA synthesizers continues to grow, both laboratory and industrial types are expected to see significant advancements in technology and capabilities. The development of more efficient and user-friendly synthesizers will further enhance the accessibility and utility of DNA synthesis in both research and commercial settings. With the ongoing advancements in genomics and synthetic biology, the DNA synthesizer global market is poised for continued growth and innovation, offering new opportunities for scientific discovery and technological advancement.

Laboratory, Biopharmaceutical, Others in the DNA Synthesizer- Global Market:

DNA synthesizers are versatile tools with a wide range of applications across various fields, including laboratory research, biopharmaceuticals, and other industries. In laboratory settings, DNA synthesizers are used to create custom DNA sequences for research purposes. Scientists and researchers rely on these instruments to design and produce specific DNA sequences that are essential for studying gene functions, genetic pathways, and molecular interactions. DNA synthesizers enable researchers to conduct experiments with high precision and accuracy, facilitating advancements in genetic research and biotechnology. In the biopharmaceutical industry, DNA synthesizers play a crucial role in drug development and production. Biopharmaceutical companies use these instruments to create synthetic DNA sequences that are used in the development of new drugs and therapies. DNA synthesizers enable the production of large quantities of DNA sequences with high accuracy and efficiency, making them essential tools for the biopharmaceutical industry. The ability to design and produce specific DNA sequences allows for the development of targeted therapies and personalized medicine, offering new opportunities for treating various diseases and medical conditions. In addition to laboratory and biopharmaceutical applications, DNA synthesizers are also used in other industries such as agriculture, diagnostics, and environmental science. In agriculture, DNA synthesizers are used to create genetically modified organisms (GMOs) that are resistant to pests and diseases, improving crop yields and food security. In diagnostics, DNA synthesizers are used to develop DNA-based tests and assays for detecting genetic disorders and infectious diseases. In environmental science, DNA synthesizers are used to study and monitor biodiversity, as well as to develop solutions for environmental challenges such as pollution and climate change. The versatility and utility of DNA synthesizers make them essential tools for scientific research and technological advancement across various fields. As the global market for DNA synthesizers continues to grow, the demand for these instruments is expected to increase, driving further innovation and development in the field of DNA synthesis.

DNA Synthesizer- Global Market Outlook:

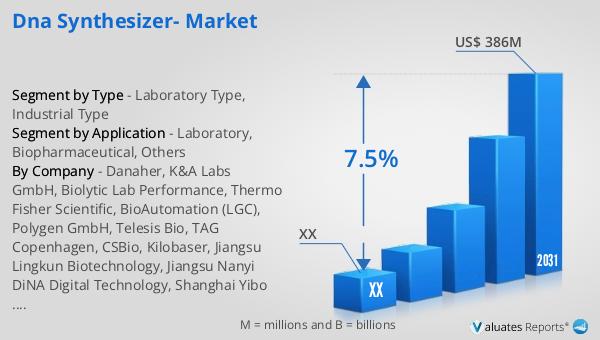

The global market for DNA synthesizers was valued at approximately $234 million in 2024 and is projected to reach an adjusted size of $386 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.5% during the forecast period from 2025 to 2031. The market is dominated by the top five players, who collectively hold about 62% of the market share. North America is the largest market for DNA synthesizers, accounting for approximately 36% of the global market share, followed by the Asia-Pacific and Europe regions, each holding around 28% of the market share. In terms of product type, the industrial type is the largest segment, representing about 73% of the market. The biopharmaceutical sector is the largest application field for DNA synthesizers, with a market share of approximately 54%. These figures highlight the significant role that DNA synthesizers play in the biopharmaceutical industry, as well as their growing importance in other sectors. As the demand for synthetic DNA continues to rise, the global market for DNA synthesizers is expected to experience substantial growth, driven by advancements in technology and increasing investments in genetic research and development.

| Report Metric | Details |

| Report Name | DNA Synthesizer- Market |

| Forecasted market size in 2031 | US$ 386 million |

| CAGR | 7.5% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Danaher, K&A Labs GmbH, Biolytic Lab Performance, Thermo Fisher Scientific, BioAutomation (LGC), Polygen GmbH, Telesis Bio, TAG Copenhagen, CSBio, Kilobaser, Jiangsu Lingkun Biotechnology, Jiangsu Nanyi DiNA Digital Technology, Shanghai Yibo Biotechnology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |