What is Smart Roads- Global Market?

Smart roads represent a transformative leap in infrastructure, integrating advanced technologies to enhance the efficiency, safety, and sustainability of transportation networks worldwide. These roads are equipped with sensors, IoT devices, and communication technologies that enable real-time data collection and analysis. This data is used to monitor traffic flow, detect accidents, and manage road maintenance proactively. Smart roads can communicate with connected vehicles, providing drivers with real-time information about traffic conditions, road hazards, and optimal routes. This not only improves the driving experience but also reduces congestion and emissions. The global market for smart roads is expanding rapidly as governments and private sectors invest in upgrading existing infrastructure to meet the demands of modern transportation. The integration of renewable energy sources, such as solar panels embedded in road surfaces, further enhances the sustainability aspect of smart roads. As urbanization continues to rise, the need for efficient and intelligent transportation systems becomes increasingly critical, positioning smart roads as a key component in the future of global infrastructure development.

Software, Hardware in the Smart Roads- Global Market:

The smart roads market is characterized by the integration of both software and hardware components, each playing a crucial role in the functionality and effectiveness of these advanced transportation systems. On the hardware side, smart roads are equipped with a variety of sensors, cameras, and communication devices that collect and transmit data. These include inductive loops embedded in the road surface to detect vehicle presence and speed, as well as cameras and radar systems for monitoring traffic flow and identifying incidents. Additionally, smart roads may incorporate LED lighting systems that adjust brightness based on traffic conditions and weather, enhancing safety and energy efficiency. The hardware infrastructure also includes digital signage that provides real-time information to drivers, such as traffic updates and road conditions. On the software side, smart roads rely on sophisticated data analytics platforms that process the vast amounts of data collected by the hardware components. These platforms use machine learning algorithms and artificial intelligence to analyze traffic patterns, predict congestion, and optimize traffic signal timings. Software solutions also enable communication between vehicles and infrastructure, facilitating the exchange of information that can improve traffic flow and reduce accidents. Furthermore, software applications are used for asset management, allowing authorities to monitor the condition of road infrastructure and schedule maintenance activities proactively. The integration of software and hardware in smart roads not only enhances the efficiency of transportation systems but also contributes to environmental sustainability by reducing emissions and energy consumption. As the global market for smart roads continues to grow, the demand for innovative software and hardware solutions is expected to increase, driving further advancements in this field.

Urban Traffic, Highway, Bridges and Tunnels, Others in the Smart Roads- Global Market:

Smart roads have a wide range of applications across different areas, including urban traffic management, highways, bridges, tunnels, and more. In urban areas, smart roads play a critical role in managing traffic congestion and improving mobility. By utilizing real-time data from sensors and cameras, traffic management systems can optimize traffic signal timings, reduce bottlenecks, and enhance the overall flow of vehicles. This not only reduces travel time for commuters but also lowers emissions by minimizing idling and stop-and-go traffic. On highways, smart roads enhance safety and efficiency by providing drivers with real-time information about road conditions, weather, and potential hazards. This information can be communicated through digital signage or directly to connected vehicles, allowing drivers to make informed decisions and avoid accidents. Smart roads also facilitate the implementation of dynamic tolling systems, where toll rates are adjusted based on traffic conditions, encouraging more efficient use of highway infrastructure. In the context of bridges and tunnels, smart roads incorporate structural health monitoring systems that detect signs of wear and tear, enabling timely maintenance and reducing the risk of structural failures. These systems use sensors to monitor parameters such as vibration, temperature, and stress, providing valuable data for infrastructure management. Beyond these specific applications, smart roads contribute to the broader goal of creating intelligent transportation systems that enhance connectivity, safety, and sustainability. As the global market for smart roads continues to expand, their usage in various areas is expected to grow, driving improvements in transportation infrastructure worldwide.

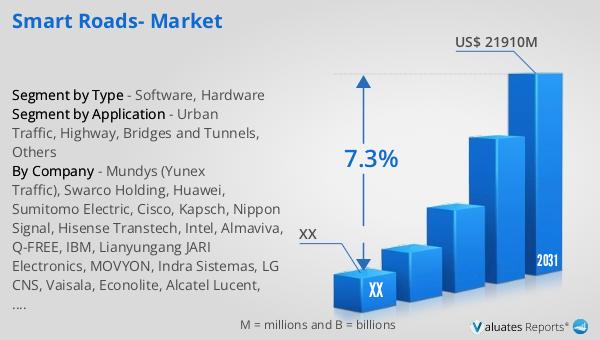

Smart Roads- Global Market Outlook:

The global smart roads market is poised for significant growth, with its value projected to increase from an estimated $13,450 million in 2024 to a revised size of $21,910 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.3% during the forecast period from 2025 to 2031. The market is dominated by the top five players, who collectively hold a share exceeding 32%. China emerges as the largest market, accounting for approximately 34% of the global share, followed by Europe and the Americas, which hold shares of 31% and 18%, respectively. In terms of product type, hardware is the largest segment, occupying a substantial share of 63%. This dominance is attributed to the extensive deployment of sensors, cameras, and communication devices that form the backbone of smart road infrastructure. On the application front, urban traffic management stands out as the most significant segment, with a share of about 52%. This highlights the critical role of smart roads in addressing the challenges of urbanization and traffic congestion. As the market continues to evolve, the integration of advanced technologies and the expansion of smart road applications are expected to drive further growth and innovation in this dynamic sector.

| Report Metric | Details |

| Report Name | Smart Roads- Market |

| Forecasted market size in 2031 | US$ 21910 million |

| CAGR | 7.3% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Mundys (Yunex Traffic), Swarco Holding, Huawei, Sumitomo Electric, Cisco, Kapsch, Nippon Signal, Hisense Transtech, Intel, Almaviva, Q-FREE, IBM, Lianyungang JARI Electronics, MOVYON, Indra Sistemas, LG CNS, Vaisala, Econolite, Alcatel Lucent, Valerann |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |