What is Global Graphene Powered Batteries Market?

The Global Graphene Powered Batteries Market represents a burgeoning sector within the energy storage industry, driven by the unique properties of graphene. Graphene, a single layer of carbon atoms arranged in a two-dimensional honeycomb lattice, is renowned for its exceptional electrical conductivity, mechanical strength, and thermal properties. These characteristics make it an ideal material for enhancing battery performance. In the context of batteries, graphene is used to improve energy density, charge and discharge rates, and overall battery lifespan. The market for graphene-powered batteries is gaining traction as industries seek more efficient and sustainable energy storage solutions. This market encompasses various types of batteries, including lithium-ion, lead-acid, and others, which are enhanced with graphene to deliver superior performance. The demand for these advanced batteries is fueled by the growing need for efficient energy storage in applications such as electric vehicles, consumer electronics, and renewable energy systems. As the world moves towards cleaner and more sustainable energy solutions, the Global Graphene Powered Batteries Market is poised for significant growth, offering innovative solutions to meet the evolving energy demands of various industries.

Graphene Cylindrical Battery, Graphene Prismatic Battery in the Global Graphene Powered Batteries Market:

Graphene cylindrical and prismatic batteries are two prominent types of batteries within the Global Graphene Powered Batteries Market, each offering distinct advantages and applications. Graphene cylindrical batteries are characterized by their cylindrical shape, which is similar to traditional AA or AAA batteries. These batteries leverage graphene's exceptional conductivity and thermal properties to enhance performance. The cylindrical design allows for efficient packing of cells, making them suitable for applications where space is a constraint. They are commonly used in portable electronic devices, power tools, and electric vehicles. The incorporation of graphene in these batteries results in faster charging times, higher energy density, and improved thermal management, which are critical for devices that require quick bursts of power or operate in high-temperature environments. On the other hand, graphene prismatic batteries are designed with a flat, rectangular shape, which allows for a more compact and lightweight design compared to cylindrical batteries. This form factor is particularly advantageous in applications where space and weight are critical considerations, such as in electric vehicles and drones. The use of graphene in prismatic batteries enhances their energy density and cycle life, making them ideal for applications that demand long-lasting and reliable power sources. The prismatic design also facilitates better heat dissipation, which is crucial for maintaining battery performance and safety. Both graphene cylindrical and prismatic batteries are integral to the advancement of the Global Graphene Powered Batteries Market, offering tailored solutions to meet the diverse energy storage needs of various industries. As the demand for efficient and sustainable energy storage solutions continues to rise, these graphene-enhanced batteries are expected to play a pivotal role in shaping the future of energy storage technology.

Electric Vehicle (EV), Electric E-Motorcycle & Scooter, Others in the Global Graphene Powered Batteries Market:

The Global Graphene Powered Batteries Market finds significant applications in various sectors, including electric vehicles (EVs), electric e-motorcycles and scooters, and other industries. In the realm of electric vehicles, graphene-powered batteries are revolutionizing the industry by offering enhanced performance and efficiency. The superior energy density and fast charging capabilities of graphene batteries make them ideal for EVs, addressing one of the major challenges of electric mobility: range anxiety. With graphene-enhanced batteries, EVs can achieve longer driving ranges and shorter charging times, making them more appealing to consumers and accelerating the adoption of electric mobility. Additionally, the improved thermal management of graphene batteries ensures safety and reliability, which are critical factors for the widespread acceptance of electric vehicles. In the electric e-motorcycle and scooter segment, graphene-powered batteries offer similar advantages. The lightweight and compact design of graphene batteries make them suitable for two-wheeled electric vehicles, where space and weight are crucial considerations. The fast charging and high energy density of graphene batteries enable e-motorcycles and scooters to deliver impressive performance and range, making them a viable alternative to traditional gasoline-powered vehicles. This is particularly important in urban areas, where electric two-wheelers are gaining popularity as a convenient and eco-friendly mode of transportation. Beyond the automotive sector, the Global Graphene Powered Batteries Market is also making inroads into other industries. In consumer electronics, graphene batteries are being used to power devices such as smartphones, laptops, and wearable technology, offering longer battery life and faster charging times. In the renewable energy sector, graphene batteries are being integrated into energy storage systems to enhance the efficiency and reliability of solar and wind power installations. The ability of graphene batteries to store and deliver energy efficiently makes them a valuable asset in the transition towards a more sustainable energy future. As the demand for efficient and sustainable energy storage solutions continues to grow, the Global Graphene Powered Batteries Market is poised to play a crucial role in shaping the future of various industries.

Global Graphene Powered Batteries Market Outlook:

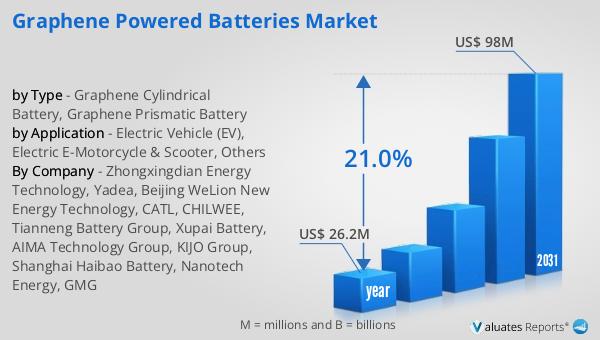

The global market for graphene-powered batteries is experiencing significant growth, with its valuation reaching $26.2 million in 2024. This market is projected to expand substantially, reaching an estimated size of $98 million by 2031. This growth trajectory is driven by a compound annual growth rate (CAGR) of 21.0% during the forecast period. The impressive growth rate underscores the increasing demand for advanced energy storage solutions that graphene-powered batteries offer. The unique properties of graphene, such as high electrical conductivity, mechanical strength, and thermal stability, make it an ideal material for enhancing battery performance. As industries across the globe seek more efficient and sustainable energy storage solutions, the adoption of graphene-powered batteries is expected to rise. This market growth is further fueled by the increasing demand for electric vehicles, consumer electronics, and renewable energy systems, all of which require efficient and reliable energy storage solutions. The projected growth of the Global Graphene Powered Batteries Market highlights the potential of graphene technology to revolutionize the energy storage industry, offering innovative solutions to meet the evolving energy demands of various sectors. As the market continues to expand, it presents significant opportunities for companies and investors looking to capitalize on the growing demand for advanced energy storage solutions.

| Report Metric | Details |

| Report Name | Graphene Powered Batteries Market |

| Accounted market size in year | US$ 26.2 million |

| Forecasted market size in 2031 | US$ 98 million |

| CAGR | 21.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Zhongxingdian Energy Technology, Yadea, Beijing WeLion New Energy Technology, CATL, CHILWEE, Tianneng Battery Group, Xupai Battery, AIMA Technology Group, KIJO Group, Shanghai Haibao Battery, Nanotech Energy, GMG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |