What is Global Programmable Stage Illumination Market?

The Global Programmable Stage Illumination Market refers to the industry focused on the development, production, and distribution of advanced lighting systems that can be programmed to create dynamic and visually captivating lighting effects for various stage performances. These systems are integral to enhancing the visual experience of live events, including concerts, theater productions, and other entertainment venues. Programmable stage illumination involves the use of sophisticated lighting fixtures and control systems that allow for precise manipulation of light intensity, color, and movement. This market has seen significant growth due to the increasing demand for high-quality visual effects in live performances, driven by advancements in technology and the growing popularity of live events worldwide. The market encompasses a wide range of products, including LED lights, halogen lamps, and discharge lamps, each offering unique benefits and applications. As the entertainment industry continues to evolve, the Global Programmable Stage Illumination Market is expected to expand further, driven by innovations in lighting technology and the increasing emphasis on creating immersive and engaging experiences for audiences.

LED, Halogen, Discharge in the Global Programmable Stage Illumination Market:

In the realm of the Global Programmable Stage Illumination Market, three primary types of lighting technologies are prevalent: LED, halogen, and discharge lamps. Each of these lighting technologies offers distinct advantages and is chosen based on specific requirements of stage performances. LED (Light Emitting Diode) lights are renowned for their energy efficiency, long lifespan, and versatility. They are capable of producing a wide spectrum of colors without the need for additional color filters, making them a popular choice for dynamic stage lighting. LEDs are also known for their low heat emission, which is beneficial in maintaining a comfortable environment on stage and reducing the risk of overheating. This technology has revolutionized stage lighting by providing designers with the flexibility to create intricate lighting designs that can be easily programmed and controlled. Halogen lamps, on the other hand, are known for their bright, white light and excellent color rendering capabilities. They are often used in situations where a natural and warm light is desired. Halogen lights are relatively inexpensive and provide a consistent light output, making them a reliable choice for many stage lighting applications. However, they tend to consume more energy compared to LEDs and have a shorter lifespan, which can lead to higher maintenance costs over time. Despite these drawbacks, halogen lamps remain a staple in the industry due to their ability to produce high-quality light that enhances the visual appeal of performances. Discharge lamps, including metal halide and high-pressure sodium lamps, are another key component of the Global Programmable Stage Illumination Market. These lamps are known for their high-intensity light output and are often used in large venues where powerful lighting is required. Discharge lamps are capable of producing a bright and focused beam of light, making them ideal for spotlighting and creating dramatic effects on stage. However, they require a warm-up period to reach full brightness and can generate significant heat, which needs to be managed to ensure safety and comfort during performances. Despite these challenges, discharge lamps are valued for their ability to deliver intense and vibrant lighting that can enhance the overall impact of a stage production. In summary, the Global Programmable Stage Illumination Market is characterized by a diverse range of lighting technologies, each offering unique benefits and applications. LED lights are favored for their energy efficiency and versatility, halogen lamps for their natural light quality, and discharge lamps for their powerful output. As technology continues to advance, the market is likely to see further innovations that will enhance the capabilities and applications of these lighting systems, ultimately contributing to more immersive and engaging stage performances.

Architectural, Entertainment, Concert/Touring, Others in the Global Programmable Stage Illumination Market:

The Global Programmable Stage Illumination Market finds its applications across various sectors, including architectural, entertainment, concert/touring, and other areas. In the architectural domain, programmable stage illumination is used to enhance the aesthetic appeal of buildings and structures. By using dynamic lighting systems, architects and designers can create visually stunning effects that highlight the architectural features of a building. This is particularly popular in urban environments where buildings are often used as canvases for light shows and projections. Programmable lighting allows for the creation of intricate patterns and color schemes that can transform the appearance of a structure, making it a focal point in the cityscape. In the entertainment industry, programmable stage illumination plays a crucial role in creating captivating visual experiences for audiences. Whether it's a theater production, a dance performance, or a live concert, lighting is an essential element that enhances the storytelling and emotional impact of a performance. Programmable lighting systems allow designers to synchronize lights with music and other elements of a show, creating a seamless and immersive experience for the audience. The ability to control light intensity, color, and movement in real-time enables designers to adapt to the dynamic nature of live performances, ensuring that the lighting complements the mood and theme of the show. Concert and touring productions are another significant area where programmable stage illumination is extensively used. In these settings, lighting is not just a tool for visibility but an integral part of the performance itself. Concert lighting designers use programmable systems to create elaborate light shows that are synchronized with the music, enhancing the overall experience for concert-goers. The use of programmable lighting allows for the creation of unique and memorable visual effects that can be tailored to the specific style and genre of the music being performed. This level of customization is essential for creating a distinctive brand and identity for artists and performers. Beyond these primary areas, programmable stage illumination is also used in various other applications, such as corporate events, exhibitions, and theme parks. In corporate settings, dynamic lighting can be used to create an engaging atmosphere for product launches, conferences, and other events. Exhibitions and trade shows often use programmable lighting to highlight products and create an inviting environment for attendees. In theme parks, lighting is used to enhance attractions and create immersive experiences for visitors. The versatility and adaptability of programmable stage illumination make it a valuable tool in a wide range of applications, contributing to its growing demand in the global market.

Global Programmable Stage Illumination Market Outlook:

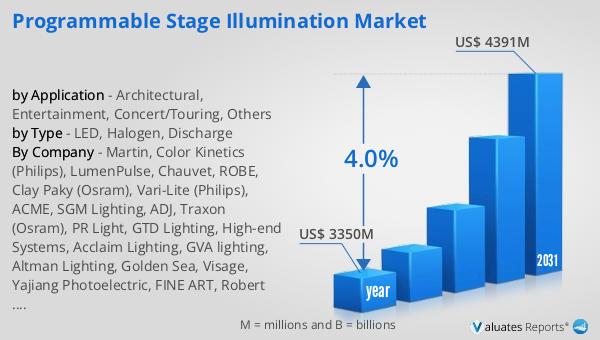

In 2024, the global market for Programmable Stage Illumination was valued at approximately 3,350 million US dollars. Looking ahead, this market is anticipated to expand, reaching an estimated size of 4,391 million US dollars by the year 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.0% over the forecast period. This steady growth can be attributed to the increasing demand for advanced lighting solutions in various sectors, including entertainment, architecture, and live events. As technology continues to evolve, the capabilities of programmable stage illumination systems are expected to enhance, offering more sophisticated and customizable lighting options for users. The market's expansion is also driven by the rising popularity of live performances and events, which require high-quality lighting to create engaging and memorable experiences for audiences. With the ongoing advancements in lighting technology and the growing emphasis on creating immersive environments, the Global Programmable Stage Illumination Market is poised for continued growth and innovation in the coming years.

| Report Metric | Details |

| Report Name | Programmable Stage Illumination Market |

| Accounted market size in year | US$ 3350 million |

| Forecasted market size in 2031 | US$ 4391 million |

| CAGR | 4.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Martin, Color Kinetics (Philips), LumenPulse, Chauvet, ROBE, Clay Paky (Osram), Vari-Lite (Philips), ACME, SGM Lighting, ADJ, Traxon (Osram), PR Light, GTD Lighting, High-end Systems, Acclaim Lighting, GVA lighting, Altman Lighting, Golden Sea, Visage, Yajiang Photoelectric, FINE ART, Robert juliat, Elation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |