What is Global Photonic Sensors and Detectors Market?

The Global Photonic Sensors and Detectors Market is a rapidly evolving sector that plays a crucial role in various industries by utilizing light-based technologies to detect and measure physical properties. Photonic sensors and detectors are devices that convert light into an electrical signal, enabling the measurement of various parameters such as temperature, pressure, and chemical composition. These devices are integral to numerous applications, ranging from telecommunications to healthcare, due to their high sensitivity, accuracy, and ability to operate in harsh environments. The market encompasses a wide range of products, including fiber optic sensors, biophotonic sensors, and image sensors, each serving distinct purposes. The growth of this market is driven by advancements in technology, increasing demand for automation, and the need for precise and reliable sensing solutions across different sectors. As industries continue to seek innovative ways to enhance efficiency and performance, the Global Photonic Sensors and Detectors Market is poised to expand, offering new opportunities for development and application. The market's evolution is marked by continuous research and development efforts aimed at improving the capabilities and applications of photonic technologies, making it a dynamic and promising field.

Fibre Optic Sensors, Biophotonic Sensors, Image Sensors, Others in the Global Photonic Sensors and Detectors Market:

Fibre optic sensors are a pivotal component of the Global Photonic Sensors and Detectors Market, known for their ability to transmit data over long distances with minimal loss. These sensors utilize optical fibers to detect changes in light properties, such as intensity, phase, and wavelength, which can be translated into measurements of temperature, pressure, and strain. Their high sensitivity and immunity to electromagnetic interference make them ideal for applications in telecommunications, structural health monitoring, and industrial automation. Biophotonic sensors, on the other hand, leverage the interaction of light with biological materials to detect and analyze biological processes. These sensors are crucial in medical diagnostics, enabling non-invasive monitoring of physiological parameters and early detection of diseases. They are also used in environmental monitoring to assess the presence of biological contaminants. Image sensors, another significant category, are used to capture visual information and convert it into electronic signals. These sensors are integral to digital cameras, smartphones, and various imaging devices, providing high-resolution images for applications in consumer electronics, security, and automotive industries. Other types of photonic sensors include infrared sensors, which detect infrared radiation and are used in applications such as night vision and thermal imaging, and laser sensors, which provide precise distance and speed measurements for industrial and automotive applications. The diversity of photonic sensors and detectors highlights their versatility and the wide range of applications they support, making them indispensable in modern technology. As the demand for advanced sensing solutions continues to grow, the development of new and improved photonic sensors is expected to drive further innovation and expansion in the market.

Defence & Security, Medical & Healthcare, Chemicals & Petrochemicals, Consumer Electronics, Others in the Global Photonic Sensors and Detectors Market:

The usage of Global Photonic Sensors and Detectors Market spans across various sectors, each benefiting from the unique capabilities of photonic technologies. In the defense and security sector, photonic sensors are employed for surveillance, target detection, and communication systems. Their ability to operate in challenging environments and provide real-time data makes them invaluable for military applications, enhancing situational awareness and operational efficiency. In the medical and healthcare industry, photonic sensors are used for diagnostic imaging, patient monitoring, and therapeutic applications. They enable non-invasive procedures, reducing the risk of infection and improving patient outcomes. Biophotonic sensors, in particular, are used for early disease detection and monitoring of vital signs, contributing to personalized medicine and improved healthcare delivery. The chemicals and petrochemicals industry utilizes photonic sensors for process monitoring and control, ensuring safety and efficiency in production processes. These sensors provide real-time data on chemical composition and concentration, enabling precise control of chemical reactions and reducing the risk of hazardous incidents. In consumer electronics, photonic sensors are integral to the functionality of devices such as smartphones, cameras, and televisions. They enable features such as facial recognition, augmented reality, and high-resolution imaging, enhancing user experience and device performance. Other sectors, such as automotive and environmental monitoring, also benefit from photonic sensors, which provide critical data for applications such as autonomous driving and pollution detection. The versatility and precision of photonic sensors make them essential tools in modern technology, driving innovation and efficiency across various industries. As the demand for advanced sensing solutions continues to grow, the Global Photonic Sensors and Detectors Market is expected to expand, offering new opportunities for development and application.

Global Photonic Sensors and Detectors Market Outlook:

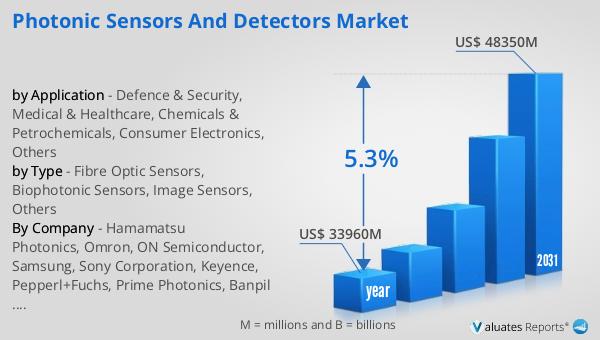

The worldwide market for Photonic Sensors and Detectors was estimated to be worth $33,960 million in 2024. It is anticipated to grow to a revised size of $48,350 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.3% over the forecast period. This growth trajectory underscores the increasing demand for photonic technologies across various industries, driven by the need for precise and reliable sensing solutions. The market's expansion is fueled by advancements in technology, which have enhanced the capabilities and applications of photonic sensors and detectors. As industries continue to seek innovative ways to improve efficiency and performance, the demand for photonic sensors is expected to rise, driving further growth in the market. The increasing adoption of automation and the need for real-time data in sectors such as healthcare, defense, and consumer electronics are also contributing to the market's expansion. As a result, the Global Photonic Sensors and Detectors Market is poised for significant growth, offering new opportunities for development and application. The market's evolution is marked by continuous research and development efforts aimed at improving the capabilities and applications of photonic technologies, making it a dynamic and promising field.

| Report Metric | Details |

| Report Name | Photonic Sensors and Detectors Market |

| Accounted market size in year | US$ 33960 million |

| Forecasted market size in 2031 | US$ 48350 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Hamamatsu Photonics, Omron, ON Semiconductor, Samsung, Sony Corporation, Keyence, Pepperl+Fuchs, Prime Photonics, Banpil Photonics, NP Photonics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |