What is Global Bioelectronics and Biosensors Market?

The Global Bioelectronics and Biosensors Market is a rapidly evolving sector that merges biology with electronics to create devices capable of detecting biological information. These devices, known as biosensors, are designed to convert a biological response into an electrical signal. The market encompasses a wide range of applications, from healthcare diagnostics to environmental monitoring. Bioelectronics and biosensors are pivotal in advancing personalized medicine, enabling real-time monitoring of health conditions, and improving the accuracy of diagnostic tests. The integration of these technologies into various sectors is driven by the need for more efficient, accurate, and cost-effective solutions. As the demand for point-of-care testing and home healthcare diagnostics increases, the market is expected to grow significantly. The development of innovative biosensor technologies, such as wearable devices and implantable sensors, is further propelling the market forward. These advancements are not only enhancing patient care but also contributing to the broader field of medical research by providing new tools for data collection and analysis. The Global Bioelectronics and Biosensors Market is thus a crucial component of the modern healthcare landscape, offering promising solutions to some of the most pressing challenges in medical diagnostics and treatment.

Electrochemical Biosensors, Thermal Biosensors, Piezoelectric Biosensors, Optical Biosensors in the Global Bioelectronics and Biosensors Market:

Electrochemical biosensors are a cornerstone of the Global Bioelectronics and Biosensors Market, known for their sensitivity and specificity in detecting various biological analytes. These sensors operate by converting a biochemical reaction into an electrical signal, which can then be measured and analyzed. They are widely used in glucose monitoring devices for diabetes management, where they provide rapid and accurate readings of blood sugar levels. The simplicity and cost-effectiveness of electrochemical biosensors make them ideal for point-of-care testing, allowing for immediate decision-making in clinical settings. Thermal biosensors, on the other hand, measure changes in temperature resulting from biochemical reactions. These sensors are particularly useful in detecting enzymatic activities and are employed in various applications, including drug discovery and metabolic studies. Their ability to provide real-time data makes them invaluable in research laboratories where precise measurements are crucial. Piezoelectric biosensors utilize the piezoelectric effect, where mechanical stress generates an electrical charge, to detect biological interactions. These sensors are highly sensitive and can detect minute changes in mass, making them suitable for applications such as detecting pathogens or monitoring environmental pollutants. Their versatility and high sensitivity are driving their adoption in both healthcare and environmental monitoring sectors. Optical biosensors, which use light to detect biological interactions, are another significant segment of the market. These sensors are known for their high sensitivity and ability to provide real-time analysis. They are widely used in the detection of biomolecules, such as proteins and nucleic acids, and are integral to the development of diagnostic assays. The non-invasive nature of optical biosensors makes them particularly appealing for medical diagnostics, where patient comfort and safety are paramount. The integration of advanced technologies, such as nanotechnology and microfluidics, is further enhancing the capabilities of these biosensors, enabling the detection of multiple analytes simultaneously and improving the overall efficiency of diagnostic processes. As the demand for rapid, accurate, and non-invasive diagnostic tools continues to grow, the role of electrochemical, thermal, piezoelectric, and optical biosensors in the Global Bioelectronics and Biosensors Market is becoming increasingly important. These technologies are not only transforming the way diseases are diagnosed and monitored but are also paving the way for new innovations in personalized medicine and healthcare delivery.

Care Testing, Home Healthcare Diagnostics, Food Industry, Research Laboratories in the Global Bioelectronics and Biosensors Market:

The Global Bioelectronics and Biosensors Market plays a crucial role in various sectors, including care testing, home healthcare diagnostics, the food industry, and research laboratories. In care testing, biosensors are used to provide rapid and accurate diagnostic results, enabling healthcare professionals to make informed decisions quickly. This is particularly important in emergency settings where time is of the essence. Biosensors allow for the immediate detection of critical biomarkers, facilitating timely interventions and improving patient outcomes. In home healthcare diagnostics, biosensors are revolutionizing the way individuals monitor their health. Devices such as wearable sensors and portable diagnostic kits empower patients to track their health conditions from the comfort of their homes. This not only enhances patient engagement and adherence to treatment plans but also reduces the burden on healthcare facilities by minimizing the need for frequent hospital visits. In the food industry, biosensors are employed to ensure food safety and quality. They are used to detect contaminants, pathogens, and allergens in food products, ensuring that they meet safety standards and regulations. This is crucial for protecting public health and maintaining consumer trust. Biosensors provide a rapid and reliable method for monitoring food quality, enabling producers to address potential issues before products reach the market. In research laboratories, biosensors are invaluable tools for studying biological processes and developing new diagnostic methods. They provide precise and real-time data, allowing researchers to gain deeper insights into complex biological systems. The versatility of biosensors makes them suitable for a wide range of applications, from drug discovery to environmental monitoring. As the demand for efficient and accurate diagnostic tools continues to grow, the Global Bioelectronics and Biosensors Market is poised to play an increasingly important role in advancing healthcare, ensuring food safety, and driving scientific research.

Global Bioelectronics and Biosensors Market Outlook:

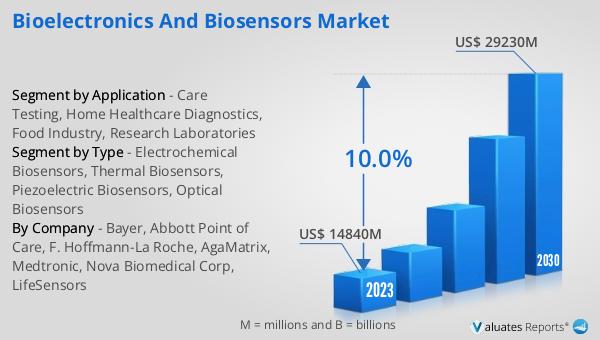

The global market for bioelectronics and biosensors is experiencing significant growth, with its value estimated at $17,990 million in 2024. This market is projected to expand to a revised size of $34,730 million by 2031, reflecting a compound annual growth rate (CAGR) of 10.0% over the forecast period. This robust growth is driven by several factors, including the increasing demand for point-of-care testing, advancements in biosensor technology, and the rising prevalence of chronic diseases that require continuous monitoring. The integration of bioelectronics and biosensors into various sectors, such as healthcare, food safety, and environmental monitoring, is further fueling market expansion. As these technologies become more sophisticated and accessible, they are transforming the way we approach diagnostics and treatment. The ability to provide real-time, accurate, and non-invasive monitoring is particularly appealing in the healthcare sector, where early detection and timely intervention can significantly improve patient outcomes. Additionally, the growing trend towards personalized medicine and the increasing focus on preventive healthcare are contributing to the market's growth. As the global population continues to age and the burden of chronic diseases rises, the demand for innovative diagnostic solutions is expected to increase, further driving the growth of the bioelectronics and biosensors market.

| Report Metric | Details |

| Report Name | Bioelectronics and Biosensors Market |

| Accounted market size in year | US$ 17990 million |

| Forecasted market size in 2031 | US$ 34730 million |

| CAGR | 10.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bayer, Abbott Point of Care, F. Hoffmann-La Roche, AgaMatrix, Medtronic, Nova Biomedical Corp, LifeSensors |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |