What is Global Avocados Market?

The global avocados market is a dynamic and rapidly expanding sector within the agricultural industry. Avocados, often referred to as "green gold," have gained immense popularity worldwide due to their rich nutritional profile and versatility in culinary applications. The market encompasses the production, distribution, and consumption of avocados across various regions, with key players including countries like Mexico, the United States, Peru, and Chile. These countries are major producers and exporters, contributing significantly to the global supply chain. The demand for avocados is driven by increasing consumer awareness of health and wellness, as avocados are rich in healthy fats, vitamins, and minerals. Additionally, the rise of plant-based diets and the popularity of avocados in dishes like guacamole and avocado toast have further fueled their demand. The market is characterized by seasonal fluctuations, with peak production periods varying by region. Despite challenges such as climate change and trade regulations, the global avocados market continues to thrive, supported by innovations in farming techniques and supply chain logistics. As consumer preferences evolve, the market is expected to adapt and grow, offering opportunities for stakeholders across the value chain.

Hass Avocado, Others in the Global Avocados Market:

Hass avocados are the most popular variety in the global avocados market, known for their creamy texture and rich flavor. Originating from California, the Hass avocado has become the standard for quality and taste, dominating the market with its year-round availability and consistent quality. This variety is favored by consumers and food service providers alike due to its versatility in culinary applications, from salads and sandwiches to smoothies and desserts. The thick, pebbly skin of the Hass avocado makes it easy to handle and transport, reducing spoilage and waste. In contrast, other avocado varieties, such as Fuerte, Bacon, and Zutano, offer different flavors and textures but are less prevalent in the market. These varieties are often grown in specific regions and have shorter seasons, making them less accessible to global consumers. The global avocados market is heavily influenced by the production and export capabilities of key countries. Mexico is the largest producer and exporter of avocados, with its favorable climate and established infrastructure supporting large-scale production. The United States, particularly California and Florida, also plays a significant role in the market, both as a producer and a major consumer. Peru and Chile are emerging as important players, with increasing exports to Europe and Asia. The demand for avocados is not limited to fresh consumption; processed avocado products such as guacamole, avocado oil, and avocado-based spreads are gaining popularity. These products cater to the growing demand for convenient and healthy food options, appealing to health-conscious consumers. The rise of e-commerce and online grocery shopping has also impacted the global avocados market, making it easier for consumers to access a wide range of avocado products. Retailers and suppliers are leveraging digital platforms to reach a broader audience and enhance customer engagement. Sustainability is a key consideration in the global avocados market, with producers and consumers becoming more aware of the environmental impact of avocado farming. Efforts to promote sustainable practices, such as water conservation and organic farming, are gaining traction. Certifications and labels indicating sustainable sourcing are becoming important factors for consumers when purchasing avocados. The global avocados market is also influenced by geopolitical factors, such as trade agreements and tariffs, which can impact the flow of avocados between countries. Despite these challenges, the market remains resilient, driven by strong consumer demand and the adaptability of producers and suppliers. As the market continues to evolve, stakeholders are exploring new opportunities for growth, such as expanding into emerging markets and developing innovative avocado-based products. The global avocados market is a testament to the growing importance of avocados in the global food landscape, reflecting changing consumer preferences and the increasing emphasis on health and sustainability.

Personal Consumer, Food Service, Food Processing Manufacturer, Others in the Global Avocados Market:

The global avocados market serves a diverse range of applications, catering to personal consumers, food service providers, food processing manufacturers, and other sectors. For personal consumers, avocados have become a staple in many households due to their health benefits and versatility. They are commonly used in home-cooked meals, from breakfast dishes like avocado toast to salads, sandwiches, and smoothies. The rise of social media and food blogs has further popularized avocados, with consumers sharing creative recipes and meal ideas. In the food service industry, avocados are a popular ingredient in restaurants, cafes, and catering services. Chefs and culinary professionals appreciate the unique flavor and texture of avocados, incorporating them into a wide range of dishes, from appetizers and entrees to desserts. The demand for avocados in the food service sector is driven by the growing trend of healthy eating and the desire for fresh, high-quality ingredients. Food processing manufacturers are also capitalizing on the popularity of avocados, developing a variety of processed products to meet consumer demand. Avocado-based products such as guacamole, avocado oil, and avocado spreads are widely available in supermarkets and grocery stores. These products offer convenience and cater to health-conscious consumers looking for nutritious and easy-to-use options. The versatility of avocados allows manufacturers to experiment with different formulations and packaging, appealing to a broad audience. Beyond these primary sectors, the global avocados market also finds applications in other areas, such as cosmetics and personal care. Avocado oil is a popular ingredient in skincare and haircare products due to its moisturizing and nourishing properties. The demand for natural and organic beauty products has led to increased interest in avocado-based formulations. Additionally, the global avocados market is influenced by cultural and regional preferences, with different countries and regions incorporating avocados into their traditional cuisines. This cultural diversity contributes to the global appeal of avocados, as consumers seek out new and exciting ways to enjoy this versatile fruit. The global avocados market is characterized by its adaptability and resilience, with stakeholders continuously exploring new opportunities for growth and innovation. As consumer preferences evolve and new trends emerge, the market is poised to expand further, offering a wide range of products and applications to meet the diverse needs of consumers worldwide.

Global Avocados Market Outlook:

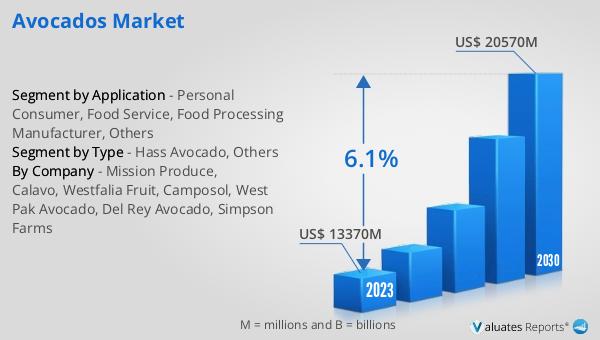

In 2024, the global market for avocados was valued at approximately $15.82 billion. This figure highlights the significant economic impact of avocados on the global agricultural sector. Over the years, the market has witnessed substantial growth, driven by increasing consumer demand for healthy and nutritious food options. Avocados, known for their rich content of healthy fats, vitamins, and minerals, have become a popular choice among health-conscious consumers. The market is projected to continue its upward trajectory, with expectations to reach a revised size of $24.22 billion by 2031. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 6.1% during the forecast period. The steady increase in market size reflects the expanding consumer base and the growing popularity of avocados in various culinary applications. The global avocados market is characterized by its dynamic nature, with key players continuously adapting to changing consumer preferences and market trends. The rise of plant-based diets and the increasing emphasis on sustainability are expected to further drive the demand for avocados. As the market evolves, stakeholders are exploring new opportunities for growth, such as expanding into emerging markets and developing innovative avocado-based products. The global avocados market outlook underscores the importance of avocados in the global food landscape, highlighting their economic significance and potential for future growth.

| Report Metric |

Details |

| Report Name |

Avocados Market |

| Accounted market size in year |

US$ 15820 million |

| Forecasted market size in 2031 |

US$ 24220 million |

| CAGR |

6.1% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

- Personal Consumer

- Food Service

- Food Processing Manufacturer

- Others

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Mission Produce, Calavo, Westfalia Fruit, Camposol, West Pak Avocado, Del Rey Avocado, Simpson Farms |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |