What is Global Industrial Plugs and Sockets Market?

The Global Industrial Plugs and Sockets Market is a crucial component of the electrical industry, providing essential connectivity solutions for various industrial applications. These devices are designed to ensure safe and reliable electrical connections in environments where standard household plugs and sockets would not suffice. Industrial plugs and sockets are built to withstand harsh conditions, such as exposure to dust, water, and extreme temperatures, making them suitable for use in factories, construction sites, and other demanding settings. The market for these products is driven by the increasing demand for energy-efficient and safe electrical systems across different industries. As industries continue to expand and modernize, the need for robust and reliable electrical connections grows, fueling the demand for industrial plugs and sockets. These products are available in various configurations and specifications to meet the diverse needs of different sectors, ensuring that they can handle the specific power requirements and environmental conditions of each application. The market is characterized by a wide range of products, including plugs, sockets, and mechanical interlocks, each designed to provide secure and efficient electrical connections. As the global economy continues to develop, the industrial plugs and sockets market is expected to grow, driven by technological advancements and the increasing focus on safety and efficiency in industrial operations.

Plugs, Socket, Mechanical Interlock in the Global Industrial Plugs and Sockets Market:

Plugs, sockets, and mechanical interlocks are integral components of the Global Industrial Plugs and Sockets Market, each serving a specific purpose in ensuring safe and efficient electrical connections. Plugs are devices that connect electrical equipment to a power source, designed to fit into corresponding sockets. They come in various types and sizes, tailored to meet the specific power requirements and environmental conditions of different industrial applications. Industrial plugs are built to withstand harsh conditions, such as exposure to dust, water, and extreme temperatures, ensuring reliable performance in demanding environments. Sockets, on the other hand, are the receptacles into which plugs are inserted to establish an electrical connection. Like plugs, industrial sockets are designed to endure challenging conditions and provide secure connections. They are available in various configurations to accommodate different plug types and power requirements. Mechanical interlocks are safety devices that prevent the accidental disconnection of plugs from sockets, ensuring that electrical connections remain secure during operation. These interlocks are particularly important in environments where accidental disconnections could lead to equipment damage or safety hazards. They work by mechanically locking the plug into the socket, preventing it from being removed while the power is on. This feature is crucial in industrial settings where equipment is often subjected to vibrations and movements that could otherwise cause plugs to become dislodged. The combination of plugs, sockets, and mechanical interlocks provides a comprehensive solution for establishing and maintaining safe and reliable electrical connections in industrial environments. These components are designed to work together seamlessly, ensuring that electrical systems operate efficiently and safely. The market for these products is driven by the increasing demand for robust and reliable electrical connections in various industries, as well as the growing focus on safety and efficiency in industrial operations. As industries continue to expand and modernize, the need for high-quality plugs, sockets, and mechanical interlocks is expected to grow, driving the development of new and innovative products to meet the evolving needs of the market.

Agriculture, Industry, Construction, Sports & Entertainment, Other in the Global Industrial Plugs and Sockets Market:

The Global Industrial Plugs and Sockets Market finds extensive usage across various sectors, including agriculture, industry, construction, sports and entertainment, and others. In agriculture, industrial plugs and sockets are essential for powering equipment such as irrigation systems, tractors, and other machinery used in farming operations. These devices ensure that electrical connections are secure and reliable, even in outdoor environments where exposure to dust, water, and extreme temperatures is common. In the industrial sector, plugs and sockets are used to power a wide range of equipment, from heavy machinery to smaller tools and appliances. The need for robust and reliable electrical connections is critical in this sector, as any disruption in power supply can lead to costly downtime and safety hazards. Industrial plugs and sockets are designed to withstand the harsh conditions often found in factories and manufacturing plants, ensuring that equipment operates efficiently and safely. In the construction industry, these devices are used to power tools and equipment on job sites, where reliable electrical connections are crucial for maintaining productivity and safety. Construction sites often present challenging conditions, such as exposure to dust, water, and extreme temperatures, making industrial plugs and sockets an essential component of the electrical infrastructure. In the sports and entertainment sector, industrial plugs and sockets are used to power lighting, sound systems, and other equipment used in events and venues. These devices ensure that electrical connections are secure and reliable, even in environments where equipment is frequently moved and reconfigured. Other sectors that rely on industrial plugs and sockets include transportation, mining, and oil and gas, where the need for robust and reliable electrical connections is critical. As these industries continue to grow and evolve, the demand for high-quality industrial plugs and sockets is expected to increase, driving the development of new and innovative products to meet the diverse needs of the market.

Global Industrial Plugs and Sockets Market Outlook:

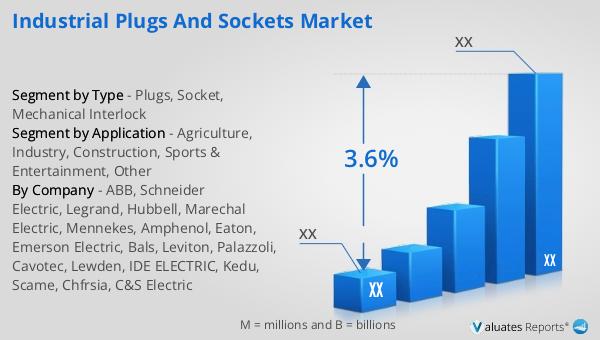

In 2024, the global market size for Industrial Plugs and Sockets was valued at approximately US$ 2,195 million. It is projected to grow to around US$ 2,802 million by 2031, with a compound annual growth rate (CAGR) of 3.6% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 35% of the market share. Among the various product segments, plugs represent the largest share, accounting for approximately 75% of the market. This significant share highlights the critical role that plugs play in the industrial plugs and sockets market, as they are essential for establishing and maintaining electrical connections in various industrial applications. The growth of the market is driven by the increasing demand for energy-efficient and safe electrical systems across different industries, as well as the ongoing expansion and modernization of industrial operations worldwide. As industries continue to evolve and adapt to new technologies and environmental standards, the need for high-quality industrial plugs and sockets is expected to grow, driving further innovation and development in the market.

| Report Metric | Details |

| Report Name | Industrial Plugs and Sockets Market |

| CAGR | 3.6% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | ABB, Schneider Electric, Legrand, Hubbell, Marechal Electric, Mennekes, Amphenol, Eaton, Emerson Electric, Bals, Leviton, Palazzoli, Cavotec, Lewden, IDE ELECTRIC, Kedu, Scame, Chfrsia, C&S Electric |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |