What is Global Rho Associated Protein Kinase 2 Market?

The Global Rho Associated Protein Kinase 2 (ROCK2) Market is a specialized segment within the broader pharmaceutical and biotechnology industry, focusing on the development and commercialization of inhibitors targeting the ROCK2 enzyme. This enzyme plays a crucial role in various cellular functions, including contraction, motility, proliferation, and apoptosis. The market is driven by the increasing interest in ROCK2 inhibitors due to their potential therapeutic applications in treating a range of diseases such as cardiovascular disorders, neurological conditions, and fibrotic diseases. The growing prevalence of these diseases, coupled with advancements in drug discovery technologies, has spurred research and development activities in this field. Additionally, collaborations between pharmaceutical companies and research institutions are fostering innovation and accelerating the development of new ROCK2 inhibitors. The market is characterized by a competitive landscape with several key players actively engaged in clinical trials and product development. As the understanding of ROCK2's role in disease mechanisms deepens, the market is expected to witness significant growth, offering promising opportunities for stakeholders involved in the development of ROCK2-targeted therapies.

AN-3485, KL-01045, AT-13148, TRX-101, Others in the Global Rho Associated Protein Kinase 2 Market:

AN-3485, KL-01045, AT-13148, TRX-101, and other compounds represent a diverse array of investigational drugs within the Global Rho Associated Protein Kinase 2 Market, each with unique properties and potential therapeutic applications. AN-3485 is a promising ROCK2 inhibitor that has shown efficacy in preclinical models of cardiovascular diseases. Its mechanism of action involves the selective inhibition of ROCK2, which leads to the relaxation of vascular smooth muscle cells, thereby reducing blood pressure and improving vascular function. This compound is currently undergoing clinical trials to evaluate its safety and efficacy in humans. KL-01045, another ROCK2 inhibitor, is being explored for its potential in treating fibrotic diseases. By targeting ROCK2, KL-01045 aims to modulate the fibrotic response, reducing tissue scarring and improving organ function. Preclinical studies have demonstrated its ability to attenuate fibrosis in animal models, paving the way for further clinical development. AT-13148 is a dual inhibitor that targets both ROCK2 and other kinases involved in cancer progression. This compound has shown promise in preclinical cancer models, where it effectively inhibits tumor growth and metastasis. Its dual-targeting approach offers a novel strategy for cancer therapy, potentially overcoming resistance mechanisms associated with single-target inhibitors. TRX-101 is an innovative ROCK2 inhibitor being investigated for its role in neurodegenerative diseases. By modulating ROCK2 activity, TRX-101 aims to protect neurons from degeneration and promote neuronal survival. Preclinical studies have shown its potential in models of Alzheimer's and Parkinson's diseases, highlighting its promise as a neuroprotective agent. Other compounds in the ROCK2 inhibitor pipeline are being developed for various indications, including immune disorders and metabolic diseases. These compounds are at different stages of development, with some in early preclinical testing and others advancing to clinical trials. The diversity of ROCK2 inhibitors reflects the broad therapeutic potential of targeting this enzyme, as well as the ongoing efforts to address unmet medical needs across multiple disease areas. As research progresses, these compounds hold the potential to transform the treatment landscape for several challenging conditions, offering hope to patients and healthcare providers alike.

Glaucoma, Fibrosis, Spinal Cord, Immune Therapy, Others in the Global Rho Associated Protein Kinase 2 Market:

The Global Rho Associated Protein Kinase 2 Market finds its application in several therapeutic areas, including glaucoma, fibrosis, spinal cord injuries, immune therapy, and others. In glaucoma, ROCK2 inhibitors are being explored for their ability to lower intraocular pressure, a key factor in the progression of this eye disease. By relaxing the trabecular meshwork and improving aqueous humor outflow, these inhibitors can effectively reduce eye pressure and prevent optic nerve damage. Clinical trials are underway to assess the long-term safety and efficacy of ROCK2 inhibitors in glaucoma patients, with promising preliminary results. In the field of fibrosis, ROCK2 inhibitors are being investigated for their potential to modulate the fibrotic response and reduce tissue scarring. By targeting the pathways involved in fibrosis, these inhibitors aim to improve organ function and prevent disease progression in conditions such as pulmonary fibrosis, liver cirrhosis, and systemic sclerosis. Preclinical studies have demonstrated the ability of ROCK2 inhibitors to attenuate fibrosis in animal models, and clinical trials are ongoing to evaluate their therapeutic potential in humans. Spinal cord injuries represent another area where ROCK2 inhibitors are being explored. By promoting axonal regeneration and reducing inflammation, these inhibitors hold promise for improving functional recovery in patients with spinal cord injuries. Preclinical studies have shown encouraging results, and clinical trials are being conducted to assess the safety and efficacy of ROCK2 inhibitors in this challenging condition. In the realm of immune therapy, ROCK2 inhibitors are being investigated for their ability to modulate immune responses and enhance the efficacy of existing treatments. By targeting ROCK2, these inhibitors aim to improve the therapeutic outcomes of immune-based therapies in conditions such as autoimmune diseases and cancer. Preclinical studies have shown the potential of ROCK2 inhibitors to enhance immune cell function and reduce inflammation, paving the way for further clinical development. Other potential applications of ROCK2 inhibitors include the treatment of metabolic diseases, cardiovascular disorders, and neurodegenerative conditions. The versatility of ROCK2 inhibitors in targeting multiple disease pathways highlights their potential as a valuable therapeutic tool in addressing a wide range of medical needs. As research continues to advance, the Global Rho Associated Protein Kinase 2 Market is poised to make significant contributions to the field of medicine, offering new hope for patients with challenging conditions.

Global Rho Associated Protein Kinase 2 Market Outlook:

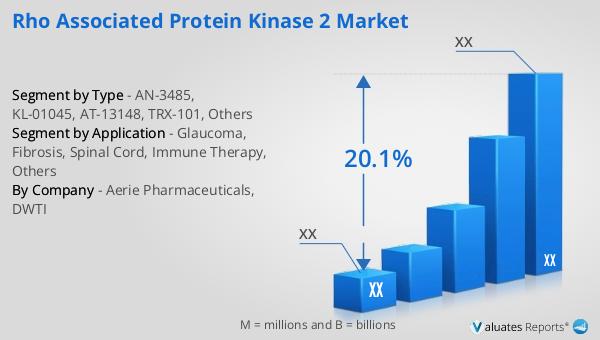

In 2024, the global market size of Rho Associated Protein Kinase 2 was estimated to be valued at approximately US$ 321 million, with projections indicating a substantial increase to around US$ 1,139 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 20.1% during the forecast period from 2025 to 2031. North America stands as the largest consumer of ROCK2 inhibitors, accounting for over 50% of the market share. This is followed by the Asia-Pacific region, which holds a 35% share of the market. Within this competitive landscape, Aerie Pharmaceuticals and DWTI are notable players, with Aerie Pharmaceuticals commanding a significant market share of approximately 60%. The robust growth of the ROCK2 market is driven by the increasing prevalence of diseases that can be targeted by ROCK2 inhibitors, coupled with advancements in drug discovery and development. The strategic positioning of key players in the market, along with their focus on innovation and clinical development, is expected to further propel the market's expansion. As the understanding of ROCK2's role in various disease mechanisms deepens, the market is anticipated to witness continued growth, offering promising opportunities for stakeholders involved in the development and commercialization of ROCK2-targeted therapies.

| Report Metric | Details |

| Report Name | Rho Associated Protein Kinase 2 Market |

| CAGR | 20.1% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Aerie Pharmaceuticals, DWTI |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |