What is Global Antivenom Market?

The Global Antivenom Market is a critical segment of the pharmaceutical industry, focusing on the development and distribution of antivenoms, which are essential for treating venomous bites and stings from snakes, spiders, scorpions, and other venomous creatures. These life-saving treatments are crucial in regions where encounters with venomous animals are common, such as parts of Africa, Asia, and Latin America. The market is driven by the need to address the high incidence of venomous bites and the associated morbidity and mortality. Antivenoms are biological products that neutralize the effects of venom, and their production involves the immunization of animals, usually horses, with small, non-lethal doses of venom. The antibodies produced are then harvested and purified to create the antivenom. The market is characterized by a few key players who dominate the production and distribution, with a focus on improving the efficacy, safety, and accessibility of these treatments. The demand for antivenoms is also influenced by factors such as government initiatives, healthcare infrastructure, and awareness programs aimed at reducing the impact of venomous bites. As the global population grows and human activities encroach on wildlife habitats, the importance of the Global Antivenom Market continues to rise.

Polyvalent antivenom, Monovalent antivenom in the Global Antivenom Market:

Polyvalent antivenoms are designed to treat envenomations from multiple species of venomous animals, making them versatile and highly valuable in regions where various venomous species coexist. These antivenoms are particularly useful in areas where identifying the specific species responsible for a bite or sting is challenging, as they can neutralize the venom from several different species. The production of polyvalent antivenoms involves the collection of venom from multiple species, which is then used to immunize animals, typically horses, to produce a broad spectrum of antibodies. This process is complex and requires significant expertise and resources, but the resulting antivenoms are crucial in providing effective treatment in diverse ecological regions. On the other hand, monovalent antivenoms are tailored to neutralize the venom of a single species. These are used in situations where the offending species is known, allowing for a more targeted and potentially more effective treatment. Monovalent antivenoms are often preferred in areas where a particular species is responsible for the majority of envenomations, as they can offer a more specific immune response. The choice between polyvalent and monovalent antivenoms depends on various factors, including the local biodiversity of venomous species, the healthcare infrastructure, and the availability of diagnostic tools to identify the species involved in envenomations. In the Global Antivenom Market, both types of antivenoms play crucial roles, with manufacturers focusing on improving the safety, efficacy, and accessibility of these treatments. The development of antivenoms involves rigorous testing and quality control to ensure their safety and effectiveness, as well as compliance with regulatory standards. The market is also influenced by research and development efforts aimed at enhancing the production processes, reducing costs, and increasing the availability of antivenoms in underserved regions. Additionally, collaborations between governments, non-profit organizations, and pharmaceutical companies are essential in addressing the challenges associated with antivenom production and distribution. These partnerships help to ensure that antivenoms reach the populations most in need, particularly in low-income countries where the burden of venomous bites is highest. The Global Antivenom Market is also impacted by the need for education and training programs for healthcare providers, to ensure the proper administration of antivenoms and the management of envenomation cases. As the market continues to evolve, there is a growing emphasis on innovation and the development of new technologies to improve the production and delivery of antivenoms. This includes the exploration of alternative methods for producing antivenoms, such as recombinant DNA technology and synthetic biology, which have the potential to revolutionize the field. Overall, the Global Antivenom Market is a dynamic and vital component of the healthcare industry, with a focus on addressing the global challenge of venomous bites and stings.

Non-profit Institutions, Hospitals and Clinic in the Global Antivenom Market:

The usage of antivenoms in non-profit institutions, hospitals, and clinics is a critical aspect of the Global Antivenom Market, as these entities play a significant role in the distribution and administration of these life-saving treatments. Non-profit institutions, such as humanitarian organizations and international health agencies, are often at the forefront of efforts to provide antivenoms to underserved regions. These organizations work to ensure that antivenoms are available in areas with high incidences of venomous bites and limited access to healthcare. They often collaborate with governments and pharmaceutical companies to facilitate the distribution of antivenoms and to support training programs for healthcare providers. In hospitals and clinics, antivenoms are an essential component of emergency care for patients who have suffered venomous bites or stings. Healthcare professionals in these settings must be trained to recognize the symptoms of envenomation and to administer the appropriate antivenom promptly. The availability of antivenoms in hospitals and clinics is crucial for reducing the morbidity and mortality associated with venomous bites, as timely treatment can significantly improve patient outcomes. The Global Antivenom Market is also influenced by the need for hospitals and clinics to maintain adequate stocks of antivenoms, which requires careful planning and coordination with suppliers. In many regions, particularly in low-income countries, the availability of antivenoms in healthcare facilities is limited by factors such as cost, supply chain challenges, and regulatory barriers. Addressing these issues is a priority for stakeholders in the Global Antivenom Market, as ensuring access to antivenoms is essential for effective healthcare delivery. Additionally, hospitals and clinics play a role in the surveillance and reporting of envenomation cases, which is important for understanding the epidemiology of venomous bites and for guiding public health interventions. The data collected by these healthcare facilities can inform the development of targeted strategies for antivenom distribution and for raising awareness about the prevention and management of venomous bites. Overall, the usage of antivenoms in non-profit institutions, hospitals, and clinics is a vital component of the Global Antivenom Market, as these entities are key to ensuring that antivenoms reach the populations most in need and that patients receive timely and effective treatment.

Global Antivenom Market Outlook:

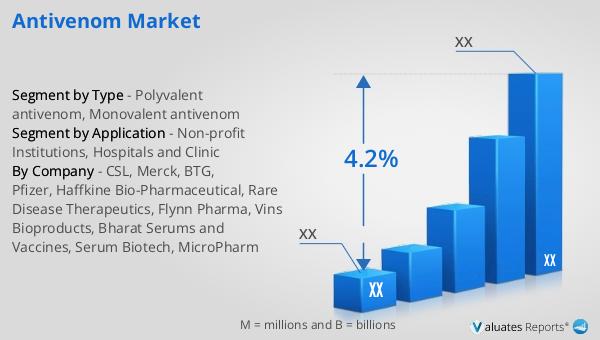

In 2024, the global market size for antivenoms was valued at approximately $1,041 million, with projections indicating it could grow to around $1,383 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2025 to 2031. CSL stands out as the leading manufacturer in the global antivenom market, commanding a 27% share in terms of revenue. Following CSL, other significant players include Merck, BTG, Pfizer, Haffkine BioPharmaceutical, Rare Disease Therapeutics, Flynn Pharma, Vins Bioproducts, Bharat Serums and Vaccines, Serum Biotech, and MicroPharm. The Asia-Pacific, Middle East, and Africa regions are the largest consumers of antivenoms, accounting for about 77% of the market share in terms of volume. This substantial consumption is driven by the high prevalence of venomous bites and stings in these regions, necessitating a robust supply of antivenoms to address the healthcare needs of affected populations. The market dynamics are shaped by factors such as the incidence of venomous bites, the availability of healthcare infrastructure, and the efforts of governments and non-profit organizations to improve access to antivenoms. As the market continues to evolve, there is a focus on enhancing the production, distribution, and accessibility of antivenoms to meet the growing demand and to ensure that these life-saving treatments reach the populations most in need.

| Report Metric | Details |

| Report Name | Antivenom Market |

| CAGR | 4.2% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | CSL, Merck, BTG, Pfizer, Haffkine Bio-Pharmaceutical, Rare Disease Therapeutics, Flynn Pharma, Vins Bioproducts, Bharat Serums and Vaccines, Serum Biotech, MicroPharm |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |