What is Global Chambered Doctor Blade Systems Market?

The Global Chambered Doctor Blade Systems Market is a specialized segment within the printing industry, focusing on the technology used to ensure precise ink application in various printing processes. These systems are crucial in maintaining the quality and consistency of printed materials by controlling the amount of ink transferred onto the printing substrate. The chambered doctor blade system consists of a chamber that holds the ink and a blade that scrapes excess ink off the printing cylinder, ensuring a clean and even application. This technology is widely used in high-speed printing applications, where precision and efficiency are paramount. The market for these systems is driven by the increasing demand for high-quality printed materials across various industries, including packaging, labeling, and publishing. As businesses continue to seek ways to enhance their printing capabilities, the demand for advanced chambered doctor blade systems is expected to grow, offering opportunities for innovation and development within the market. The systems are designed to be adaptable to different printing machines and processes, making them a versatile solution for printers looking to improve their operational efficiency and product quality.

Single-Blade System, Dual-Blade System in the Global Chambered Doctor Blade Systems Market:

The Global Chambered Doctor Blade Systems Market includes various types of systems, with the Single-Blade System and Dual-Blade System being the most prominent. The Single-Blade System is designed with a single blade that scrapes excess ink from the printing cylinder. This system is typically used in applications where precision is critical, and the printing process requires a high degree of control over ink application. The single-blade design allows for easy maintenance and replacement, making it a cost-effective solution for many printing operations. It is particularly popular in industries where the quality of the printed material is of utmost importance, such as in packaging and labeling. On the other hand, the Dual-Blade System features two blades that work in tandem to remove excess ink. This system is often used in high-speed printing applications where the volume of ink and the speed of the printing process require more robust ink management. The dual-blade design provides an additional layer of control, ensuring that the ink is applied evenly and consistently across the printing surface. This system is ideal for large-scale printing operations where efficiency and precision are critical. Both systems offer unique advantages and are chosen based on the specific needs of the printing operation. The choice between a Single-Blade System and a Dual-Blade System often depends on factors such as the type of printing machine, the speed of the printing process, and the desired quality of the printed material. As the demand for high-quality printed materials continues to grow, the market for both Single-Blade and Dual-Blade Systems is expected to expand, offering opportunities for innovation and development within the industry.

Flexographic Printing Machine, Corrugated Box Printing Slotting Machine, Others in the Global Chambered Doctor Blade Systems Market:

The Global Chambered Doctor Blade Systems Market finds extensive usage in various printing applications, including Flexographic Printing Machines, Corrugated Box Printing Slotting Machines, and others. In Flexographic Printing Machines, chambered doctor blade systems play a crucial role in ensuring precise ink application. Flexographic printing is widely used for packaging materials, labels, and other products that require high-quality printing. The chambered doctor blade system helps maintain the consistency and quality of the printed material by controlling the amount of ink applied to the printing substrate. This is particularly important in flexographic printing, where the speed and efficiency of the printing process are critical. In Corrugated Box Printing Slotting Machines, chambered doctor blade systems are used to ensure that the ink is applied evenly and consistently across the surface of the corrugated material. This is essential for producing high-quality printed boxes that meet the standards of the packaging industry. The chambered doctor blade system helps prevent issues such as ink smudging and uneven application, which can affect the appearance and quality of the final product. In addition to these applications, chambered doctor blade systems are also used in other printing processes where precision and quality are important. These systems are designed to be adaptable to different types of printing machines and processes, making them a versatile solution for printers looking to improve their operational efficiency and product quality. As the demand for high-quality printed materials continues to grow, the usage of chambered doctor blade systems in various printing applications is expected to increase, offering opportunities for innovation and development within the market.

Global Chambered Doctor Blade Systems Market Outlook:

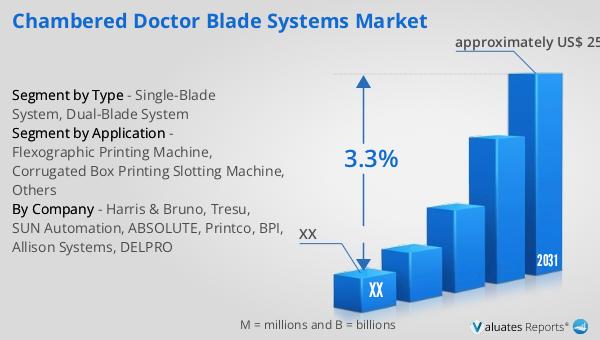

In 2024, the global market size for Chambered Doctor Blade Systems was valued at approximately US$ 20.3 million. It is projected to grow to around US$ 25.4 million by 2031, with a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2025 to 2031. North America holds the largest share of the Chambered Doctor Blade Systems market, accounting for about 36% of the market. Europe follows closely, with a market share of approximately 32%. The top three companies in this market dominate with a combined market share of about 76%. This market outlook highlights the significant role that Chambered Doctor Blade Systems play in the printing industry, driven by the increasing demand for high-quality printed materials. The growth in this market is attributed to the rising need for precision and efficiency in printing processes, as well as the continuous advancements in printing technology. As businesses strive to enhance their printing capabilities, the demand for advanced chambered doctor blade systems is expected to rise, providing opportunities for innovation and development within the market. The market's expansion is also supported by the growing adoption of these systems in various printing applications, including packaging, labeling, and publishing.

| Report Metric | Details |

| Report Name | Chambered Doctor Blade Systems Market |

| Forecasted market size in 2031 | approximately US$ 25.4 million |

| CAGR | 3.3% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Harris & Bruno, Tresu, SUN Automation, ABSOLUTE, Printco, BPI, Allison Systems, DELPRO |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |