What is Global Lithium-ion Battery Materials Market?

The Global Lithium-ion Battery Materials Market is a rapidly evolving sector that plays a crucial role in the development and advancement of energy storage solutions worldwide. Lithium-ion batteries are essential components in a wide range of applications, from consumer electronics to electric vehicles and renewable energy storage systems. The market for these materials is driven by the increasing demand for efficient, high-capacity, and long-lasting energy storage solutions. As the world shifts towards more sustainable energy sources, the need for advanced battery technologies has become more pronounced. Lithium-ion batteries are favored for their high energy density, lightweight nature, and ability to retain charge over extended periods. The market encompasses various materials, including cathodes, anodes, separators, and electrolytes, each playing a vital role in the battery's performance and efficiency. With technological advancements and increased research and development efforts, the Global Lithium-ion Battery Materials Market is poised for significant growth, catering to the ever-expanding needs of industries and consumers alike. This growth is further fueled by government initiatives and policies promoting clean energy and the reduction of carbon emissions, making lithium-ion batteries a cornerstone of the future energy landscape.

Cathode Material, Anode Materials, Lithium-Ion Battery Separator, Electrolyte in the Global Lithium-ion Battery Materials Market:

Cathode materials are a critical component of lithium-ion batteries, serving as the positive electrode where the lithium ions are stored during the discharge cycle. These materials significantly influence the battery's capacity, voltage, and overall performance. Common cathode materials include lithium cobalt oxide (LCO), lithium iron phosphate (LFP), and lithium nickel manganese cobalt oxide (NMC). Each of these materials offers distinct advantages and trade-offs in terms of energy density, safety, and cost. For instance, LCO is known for its high energy density, making it ideal for portable electronics, while LFP is favored for its thermal stability and safety, often used in electric vehicles and grid storage. Anode materials, on the other hand, are the negative electrodes in lithium-ion batteries, typically made from graphite. The anode's primary function is to store lithium ions during the charging cycle, releasing them during discharge. Graphite is widely used due to its excellent conductivity and ability to form a stable structure with lithium ions. However, research is ongoing to develop alternative anode materials, such as silicon-based compounds, which promise higher energy densities and faster charging times. The lithium-ion battery separator is another crucial component, acting as a barrier between the cathode and anode to prevent short circuits while allowing the flow of ions. Separators are typically made from microporous polymer films, designed to withstand the battery's operating conditions. The choice of separator material can impact the battery's safety, lifespan, and performance. Lastly, the electrolyte in a lithium-ion battery facilitates the movement of lithium ions between the cathode and anode. It is usually composed of a lithium salt dissolved in an organic solvent. The electrolyte's composition is vital for the battery's conductivity, stability, and overall efficiency. Innovations in electrolyte formulations aim to enhance battery performance, safety, and environmental sustainability. As the Global Lithium-ion Battery Materials Market continues to grow, advancements in these materials will be key to meeting the increasing demands for high-performance, reliable, and sustainable energy storage solutions.

Automotive, Grid Energy Storage, Consumer Electronics, Others in the Global Lithium-ion Battery Materials Market:

The Global Lithium-ion Battery Materials Market finds extensive usage across various sectors, each with unique requirements and challenges. In the automotive industry, lithium-ion batteries are pivotal in the transition to electric vehicles (EVs). These batteries provide the necessary energy density and power output to support the performance and range of modern EVs. As automakers strive to meet stringent emissions regulations and consumer demand for greener transportation options, the reliance on advanced lithium-ion battery materials becomes increasingly critical. The development of high-capacity, fast-charging batteries is essential to enhance the appeal and practicality of EVs, driving further innovation in cathode, anode, and electrolyte materials. In grid energy storage, lithium-ion batteries play a vital role in stabilizing and optimizing the use of renewable energy sources like solar and wind. These batteries store excess energy generated during peak production times, releasing it when demand is high or production is low. This capability is crucial for maintaining a reliable and efficient power grid, especially as the share of renewable energy in the global energy mix continues to rise. The demand for durable, high-capacity batteries in this sector drives ongoing research into improving the longevity and efficiency of lithium-ion battery materials. Consumer electronics, another significant market for lithium-ion batteries, benefit from the compact size and high energy density of these batteries. From smartphones and laptops to wearable devices, lithium-ion batteries power a wide array of gadgets that are integral to modern life. The continuous push for longer battery life and faster charging times in consumer electronics spurs innovation in battery materials, focusing on enhancing energy density and reducing charging times. Beyond these primary sectors, lithium-ion battery materials are also used in various other applications, including aerospace, marine, and industrial equipment. Each of these areas presents unique challenges and opportunities for the development of specialized battery materials that meet specific performance and safety requirements. As the Global Lithium-ion Battery Materials Market expands, the diverse applications and demands across these sectors will continue to drive advancements in battery technology, shaping the future of energy storage solutions.

Global Lithium-ion Battery Materials Market Outlook:

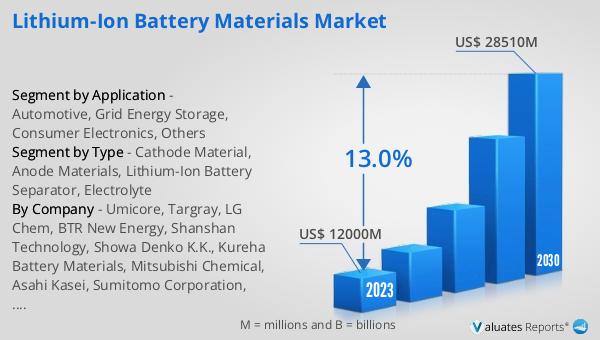

In 2024, the global market for Lithium-ion Battery Materials was estimated to be worth approximately $17.29 billion. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an adjusted value of around $36.22 billion by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 11.3% throughout the forecast period. The robust expansion of this market can be attributed to several factors, including the increasing demand for electric vehicles, the rising adoption of renewable energy sources, and the continuous advancements in battery technology. As industries and consumers alike seek more efficient and sustainable energy solutions, the demand for high-performance lithium-ion battery materials is expected to rise. This growth is further supported by government initiatives and policies aimed at reducing carbon emissions and promoting clean energy. The market's expansion is not only a reflection of the growing need for energy storage solutions but also an indication of the ongoing innovation and development within the lithium-ion battery sector. As the market continues to evolve, it will play a crucial role in shaping the future of energy storage and contributing to a more sustainable and energy-efficient world.

| Report Metric | Details |

| Report Name | Lithium-ion Battery Materials Market |

| Accounted market size in year | US$ 17290 million |

| Forecasted market size in 2031 | US$ 36220 million |

| CAGR | 11.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Umicore, Targray, LG Chem, BTR New Energy, Shanshan Technology, Showa Denko K.K., Kureha Battery Materials, Mitsubishi Chemical, Asahi Kasei, Sumitomo Corporation, Toray |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |