What is Global Special Containers Market?

The Global Special Containers Market refers to the industry focused on the production, distribution, and utilization of specialized containers designed to meet specific requirements across various sectors. These containers are not your typical shipping boxes; they are engineered to handle unique challenges such as temperature control, hazardous material containment, and oversized cargo. The market encompasses a wide range of container types, including refrigerated containers, tank containers, and flat-rack containers, each serving distinct purposes. The demand for special containers is driven by the need for efficient and safe transportation of goods that require specific handling conditions. Industries such as pharmaceuticals, chemicals, and food rely heavily on these containers to maintain product integrity during transit. As global trade continues to expand, the need for specialized containers is expected to grow, driven by technological advancements and the increasing complexity of supply chains. The market is characterized by innovation, with manufacturers constantly developing new solutions to meet the evolving needs of their clients. This dynamic environment makes the Global Special Containers Market a critical component of the global logistics and transportation industry, ensuring that goods reach their destinations safely and efficiently.

≤ 10 FT, 10-20 FT, 21-30 FT, 31-40 FT, > 40 FT in the Global Special Containers Market:

In the Global Special Containers Market, containers are categorized based on their size, which plays a crucial role in determining their application and suitability for different types of cargo. Containers that are ≤ 10 FT are typically used for smaller shipments or when space is limited. These compact containers are ideal for transporting goods that require special handling but do not occupy much space. They are often used in urban areas where space constraints are a significant consideration. Moving up in size, the 10-20 FT containers offer a bit more room and are commonly used for medium-sized shipments. These containers strike a balance between capacity and maneuverability, making them suitable for a wide range of applications, including the transportation of industrial equipment and smaller batches of chemicals. The 21-30 FT containers are a step up in size and are often employed for larger shipments that require more space but still need to be transported efficiently. These containers are versatile and can be used for various types of cargo, including bulk goods and larger industrial components. The 31-40 FT containers are among the most commonly used sizes in the industry, offering ample space for a wide range of goods. They are particularly popular in the transportation of consumer goods, machinery, and other large items that require significant space. Finally, containers that are > 40 FT are used for the largest shipments, often involving oversized or heavy cargo. These containers are essential for industries that deal with large-scale logistics, such as construction and heavy machinery. Each size category in the Global Special Containers Market serves a specific purpose, catering to the diverse needs of industries worldwide. The choice of container size depends on various factors, including the nature of the cargo, the distance of transportation, and the specific requirements of the shipment. As the market continues to evolve, the demand for different container sizes is expected to fluctuate, driven by changes in global trade patterns and the specific needs of industries. The ability to choose the right container size is crucial for businesses looking to optimize their logistics operations and ensure the safe and efficient transportation of their goods.

Oil, Natural gas, Industrial gas, Chemical industry, Pharmaceuticals, Food, Other in the Global Special Containers Market:

The Global Special Containers Market plays a vital role in various industries, providing tailored solutions for the transportation and storage of goods that require specific handling conditions. In the oil industry, special containers are used to transport crude oil and refined products safely. These containers are designed to withstand the harsh conditions of oil transportation, ensuring that the cargo remains secure and intact. Similarly, in the natural gas sector, special containers are used to transport liquefied natural gas (LNG) and other gas products. These containers are equipped with advanced insulation and pressure control systems to maintain the integrity of the gas during transit. In the industrial gas sector, special containers are essential for transporting gases such as oxygen, nitrogen, and argon. These containers are designed to handle the unique challenges associated with gas transportation, including pressure regulation and temperature control. The chemical industry also relies heavily on special containers to transport hazardous and non-hazardous chemicals safely. These containers are engineered to prevent leaks and spills, ensuring that the chemicals reach their destination without incident. In the pharmaceutical industry, special containers are used to transport temperature-sensitive medications and vaccines. These containers are equipped with advanced temperature control systems to maintain the required conditions throughout the journey. The food industry also benefits from the Global Special Containers Market, using refrigerated containers to transport perishable goods such as fruits, vegetables, and dairy products. These containers ensure that the food remains fresh and safe for consumption upon arrival. Other industries, such as electronics and automotive, also utilize special containers to transport sensitive and high-value goods. The versatility and adaptability of special containers make them an indispensable part of the global supply chain, providing solutions for a wide range of transportation challenges. As industries continue to evolve and expand, the demand for specialized containers is expected to grow, driven by the need for efficient and reliable logistics solutions.

Global Special Containers Market Outlook:

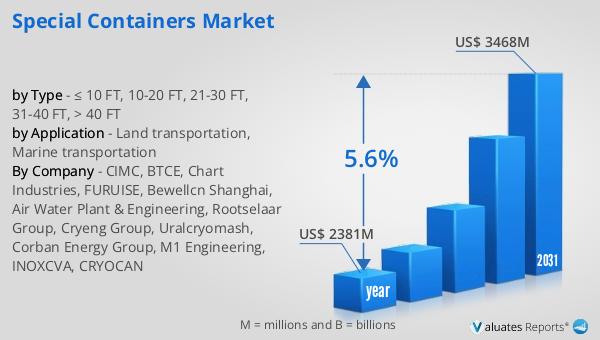

The global market for Special Containers was valued at $2,501 million in 2024, and it is anticipated to grow significantly, reaching an estimated size of $3,643 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.6% over the forecast period. The increasing demand for specialized containers is driven by the expanding global trade and the need for efficient logistics solutions across various industries. As businesses continue to seek ways to optimize their supply chains and ensure the safe transportation of goods, the market for special containers is expected to witness substantial growth. The versatility and adaptability of these containers make them an attractive option for industries looking to enhance their logistics operations. The projected growth in the market reflects the increasing importance of specialized containers in the global logistics and transportation industry. As the market continues to evolve, manufacturers are expected to focus on innovation and the development of new solutions to meet the changing needs of their clients. The growth of the Global Special Containers Market is a testament to the critical role these containers play in facilitating global trade and ensuring the safe and efficient transportation of goods.

| Report Metric | Details |

| Report Name | Special Containers Market |

| Accounted market size in year | US$ 2501 million |

| Forecasted market size in 2031 | US$ 3643 million |

| CAGR | 5.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | CIMC, BTCE, Chart Industries, Singamas Container, China Eastern Containers (CEC), CXIC Group, Daikin Industries, W&K Containers Inc., Bewellcn Shanghai, Hoover Ferguson Group, Inc., AIR WATER INC., Rootselaar Group, Uralcryomash, Corban Energy Group, CRYOCAN, TLS Offshore Containers International, Klinge Corporation, Maersk Container Industry, FURUISE |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |