What is Global Surgical Stapling Devices Sales Market?

The Global Surgical Stapling Devices Sales Market refers to the worldwide industry focused on the production and distribution of surgical stapling devices. These devices are essential tools in modern surgical procedures, used to close wounds or connect tissues during operations. Unlike traditional sutures, surgical staplers offer a quicker and often more reliable method of closure, reducing surgery time and improving patient outcomes. The market for these devices is driven by the increasing number of surgeries performed globally, advancements in surgical technology, and the growing preference for minimally invasive procedures. As healthcare systems worldwide strive to improve efficiency and patient care, the demand for surgical stapling devices continues to rise. This market encompasses a wide range of products, including manual and powered staplers, each designed for specific surgical applications. The market's growth is also fueled by the rising prevalence of chronic diseases, which often require surgical intervention, and the expanding healthcare infrastructure in emerging economies. As a result, the Global Surgical Stapling Devices Sales Market is a dynamic and rapidly evolving sector, playing a crucial role in the advancement of surgical practices worldwide.

in the Global Surgical Stapling Devices Sales Market:

In the Global Surgical Stapling Devices Sales Market, various types of stapling devices are utilized by healthcare professionals, each catering to specific surgical needs and preferences. The primary types of surgical staplers include manual staplers, powered staplers, and reusable staplers, each offering distinct advantages and applications. Manual staplers are the traditional choice, operated by hand and favored for their simplicity and cost-effectiveness. They are widely used in various surgical procedures, from general surgery to specialized operations, due to their reliability and ease of use. Powered staplers, on the other hand, are gaining popularity for their precision and efficiency. These devices are battery-operated or electrically powered, allowing for consistent staple formation and reducing the physical effort required by surgeons. Powered staplers are particularly beneficial in complex surgeries where precision is paramount, such as in thoracic or bariatric procedures. Reusable staplers are designed for multiple uses, offering a cost-effective solution for healthcare facilities. These devices are typically made from durable materials and can be sterilized between uses, making them an environmentally friendly option. In addition to these primary types, there are specialized staplers designed for specific surgical applications. For instance, skin staplers are used for closing external wounds, while endoscopic staplers are designed for minimally invasive procedures. Circular staplers are used in gastrointestinal surgeries to create anastomoses, while linear staplers are used for tissue resection and transection. The choice of stapler type often depends on the surgical procedure, the surgeon's preference, and the patient's specific needs. As the demand for surgical stapling devices continues to grow, manufacturers are investing in research and development to create innovative products that enhance surgical outcomes and improve patient safety. This includes the development of staplers with advanced features, such as adjustable staple heights, ergonomic designs, and integrated cutting mechanisms. Additionally, the market is witnessing a trend towards the use of biocompatible materials in stapler construction, reducing the risk of adverse reactions and improving patient recovery times. The Global Surgical Stapling Devices Sales Market is characterized by a diverse range of products, each designed to meet the evolving needs of the healthcare industry. As surgical techniques continue to advance, the demand for specialized and high-performance stapling devices is expected to increase, driving further innovation and growth in this dynamic market.

in the Global Surgical Stapling Devices Sales Market:

The Global Surgical Stapling Devices Sales Market finds applications across a wide range of surgical procedures, reflecting the versatility and indispensability of these devices in modern medicine. One of the primary applications is in general surgery, where surgical staplers are used for tasks such as wound closure, tissue resection, and anastomosis. These devices are favored for their ability to provide consistent and secure closures, reducing the risk of complications and improving patient outcomes. In addition to general surgery, surgical staplers are extensively used in minimally invasive procedures, such as laparoscopic and endoscopic surgeries. These techniques require precise and efficient tools, and surgical staplers are ideal for creating internal connections and closures with minimal tissue trauma. The use of staplers in minimally invasive procedures is driven by the growing preference for surgeries that offer faster recovery times and reduced postoperative pain. Another significant application of surgical stapling devices is in bariatric surgery, a field that has seen substantial growth due to the rising prevalence of obesity worldwide. In bariatric procedures, staplers are used to create gastric pouches or bypasses, essential for achieving the desired weight loss outcomes. The precision and reliability of surgical staplers make them a critical component in these complex surgeries, ensuring patient safety and surgical success. Surgical staplers are also widely used in thoracic surgery, particularly in procedures involving the lungs and esophagus. In these surgeries, staplers are used to resect diseased tissue and create anastomoses, facilitating the restoration of normal function. The use of staplers in thoracic surgery is driven by the need for precise and secure closures, which are crucial in preventing complications such as leaks or infections. Furthermore, surgical staplers are employed in colorectal surgery, where they are used to create anastomoses and resections in the treatment of conditions such as colorectal cancer or inflammatory bowel disease. The ability of staplers to provide consistent and reliable closures is particularly important in these procedures, where the integrity of the gastrointestinal tract is paramount. As the Global Surgical Stapling Devices Sales Market continues to evolve, the applications of these devices are expanding, driven by advancements in surgical techniques and the growing demand for efficient and effective surgical solutions. The versatility and reliability of surgical staplers make them an essential tool in a wide range of surgical procedures, contributing to improved patient outcomes and the advancement of modern medicine.

Global Surgical Stapling Devices Sales Market Outlook:

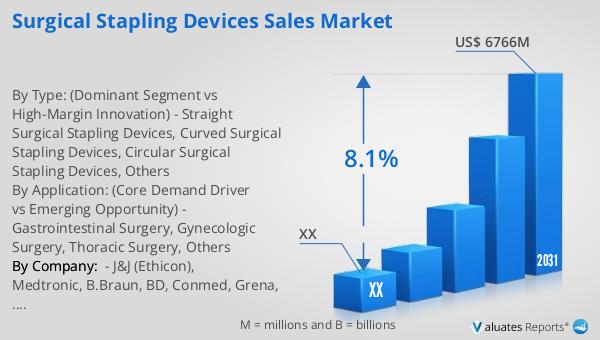

In 2024, the global market for Surgical Stapling Devices was valued at approximately $3,952 million. Looking ahead, projections indicate that by 2031, this market is expected to grow to an adjusted size of around $6,766 million, reflecting a compound annual growth rate (CAGR) of 8.1% during the forecast period from 2025 to 2031. This significant growth underscores the increasing demand for surgical stapling devices across various medical fields. The market's expansion is driven by several factors, including the rising number of surgical procedures worldwide, advancements in surgical technology, and the growing preference for minimally invasive surgeries. These factors contribute to the heightened adoption of surgical staplers, which offer efficiency and reliability in surgical closures. Notably, the global market is dominated by the top four manufacturers, who collectively hold a market share exceeding 70%. This concentration of market power highlights the competitive landscape and the importance of innovation and quality in maintaining a leading position. As the market continues to grow, these manufacturers are likely to focus on research and development to introduce advanced products that meet the evolving needs of healthcare professionals and patients. The outlook for the Global Surgical Stapling Devices Sales Market is promising, with substantial growth anticipated in the coming years, driven by technological advancements and the increasing demand for efficient surgical solutions.

| Report Metric | Details |

| Report Name | Surgical Stapling Devices Sales Market |

| Forecasted market size in 2031 | US$ 6766 million |

| CAGR | 8.1% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | J&J (Ethicon), Medtronic, B.Braun, BD, Conmed, Grena, Frankenman, Purple surgical, Kangdi, Reach, Dextera Surgical, Medizintechnik |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |