What is Global Anti-Corrosion Coating for Building Steel Structure Market?

The Global Anti-Corrosion Coating for Building Steel Structure Market is a specialized segment within the broader coatings industry, focusing on products designed to protect steel structures from corrosion. Corrosion is a natural process that deteriorates metals, and when it comes to steel structures, this can lead to significant safety and financial concerns. Anti-corrosion coatings are applied to steel to create a barrier that prevents moisture, salt, and other corrosive elements from reaching the metal surface. These coatings are essential in extending the lifespan of steel structures, reducing maintenance costs, and ensuring safety. The market for these coatings is driven by the need for durable infrastructure, especially in regions with harsh environmental conditions. As urbanization and industrialization continue to rise globally, the demand for anti-corrosion coatings is expected to grow, making it a vital component in the construction and maintenance of buildings, bridges, and other steel structures. The market encompasses various types of coatings, including epoxy, polyurethane, and acrylic, each offering different levels of protection and application methods. The choice of coating often depends on the specific environmental challenges and the desired longevity of the structure.

Metal Anti-corrosion Coating, Anti-corrosion Coatings Resistant to Seawater Intrusion in the Global Anti-Corrosion Coating for Building Steel Structure Market:

Metal anti-corrosion coatings are crucial in protecting steel structures from the damaging effects of corrosion, which can compromise structural integrity and lead to costly repairs. These coatings are formulated to provide a protective layer that prevents corrosive elements such as water, salt, and chemicals from reaching the metal surface. In the context of the Global Anti-Corrosion Coating for Building Steel Structure Market, these coatings are indispensable for ensuring the longevity and safety of steel structures. There are several types of metal anti-corrosion coatings, each with unique properties and applications. Epoxy coatings are widely used due to their excellent adhesion, chemical resistance, and durability. They are particularly effective in environments where chemical exposure is a concern. Polyurethane coatings offer superior UV resistance and flexibility, making them ideal for structures exposed to sunlight and temperature fluctuations. Acrylic coatings, on the other hand, are valued for their quick-drying properties and ease of application, although they may not provide the same level of protection as epoxy or polyurethane coatings. Anti-corrosion coatings resistant to seawater intrusion are specifically designed to protect structures in marine environments. These coatings must withstand the harsh conditions of saltwater, which can accelerate the corrosion process. Marine-grade coatings often incorporate advanced technologies such as zinc-rich primers, which provide sacrificial protection by corroding in place of the steel. Additionally, these coatings may include additives that enhance their resistance to biofouling, a common issue in seawater environments where organisms such as barnacles and algae attach to surfaces. The Global Anti-Corrosion Coating for Building Steel Structure Market is driven by the increasing demand for durable infrastructure in coastal and industrial areas. As urbanization and industrial activities continue to expand, the need for effective corrosion protection becomes more critical. In addition to traditional applications, there is a growing interest in environmentally friendly coatings that minimize the use of volatile organic compounds (VOCs) and other harmful substances. These eco-friendly coatings are gaining traction as regulatory bodies impose stricter environmental standards. The market is also witnessing advancements in coating technologies, such as the development of nanocoatings and smart coatings. Nanocoatings utilize nanoparticles to enhance the protective properties of the coating, offering improved resistance to corrosion and wear. Smart coatings, on the other hand, are designed to respond to environmental changes, such as temperature or pH fluctuations, by altering their properties to provide optimal protection. These innovations are expected to drive the growth of the Global Anti-Corrosion Coating for Building Steel Structure Market in the coming years. In conclusion, metal anti-corrosion coatings play a vital role in safeguarding steel structures from the detrimental effects of corrosion. The market for these coatings is expanding as the demand for durable and sustainable infrastructure increases. With advancements in coating technologies and a focus on environmentally friendly solutions, the Global Anti-Corrosion Coating for Building Steel Structure Market is poised for significant growth.

Houses, Bridge, Others in the Global Anti-Corrosion Coating for Building Steel Structure Market:

The usage of Global Anti-Corrosion Coating for Building Steel Structure Market is extensive and varied, particularly in areas such as houses, bridges, and other infrastructure. In residential construction, anti-corrosion coatings are applied to steel components to ensure the longevity and safety of the structure. Steel is often used in the framework of houses, especially in regions prone to natural disasters like earthquakes, due to its strength and flexibility. However, without proper protection, steel can corrode over time, compromising the structural integrity of the building. Anti-corrosion coatings provide a protective barrier that prevents moisture and other corrosive elements from reaching the steel, thereby extending the lifespan of the structure and reducing maintenance costs. In the construction of bridges, anti-corrosion coatings are even more critical. Bridges are exposed to a variety of environmental factors, including moisture, salt from de-icing agents, and pollutants, all of which can accelerate the corrosion process. The failure of a bridge due to corrosion can have catastrophic consequences, making the application of anti-corrosion coatings essential. These coatings not only protect the steel components of the bridge but also enhance its aesthetic appeal by providing a smooth, uniform finish. In addition to traditional coatings, advanced technologies such as zinc-rich primers and epoxy coatings are often used in bridge construction to provide superior protection against corrosion. Beyond houses and bridges, anti-corrosion coatings are used in a wide range of other applications, including industrial facilities, pipelines, and offshore structures. In industrial settings, steel structures are often exposed to harsh chemicals and extreme temperatures, making corrosion protection a top priority. Anti-corrosion coatings help to prevent the degradation of steel components, ensuring the safety and efficiency of industrial operations. In the oil and gas industry, pipelines and offshore platforms are subjected to some of the most corrosive environments on the planet. Anti-corrosion coatings are essential in protecting these structures from the damaging effects of seawater, chemicals, and temperature fluctuations. The Global Anti-Corrosion Coating for Building Steel Structure Market is driven by the need for durable and sustainable infrastructure across various sectors. As urbanization and industrialization continue to expand, the demand for effective corrosion protection solutions is expected to grow. In addition to traditional applications, there is a growing interest in environmentally friendly coatings that minimize the use of harmful substances. These eco-friendly coatings are gaining traction as regulatory bodies impose stricter environmental standards. The market is also witnessing advancements in coating technologies, such as the development of nanocoatings and smart coatings. These innovations are expected to drive the growth of the Global Anti-Corrosion Coating for Building Steel Structure Market in the coming years.

Global Anti-Corrosion Coating for Building Steel Structure Market Outlook:

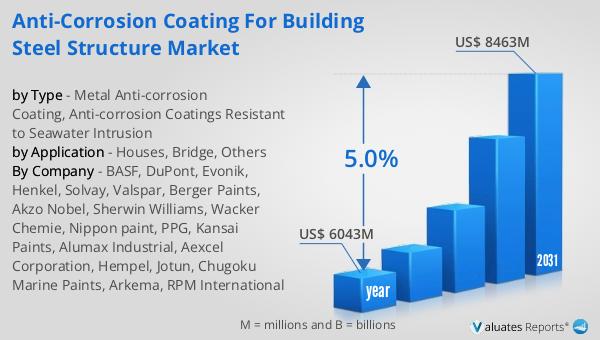

The global market for Anti-Corrosion Coating for Building Steel Structure was valued at $6,043 million in 2024 and is anticipated to expand to a revised size of $8,463 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.0% over the forecast period. This growth trajectory underscores the increasing demand for protective coatings that safeguard steel structures from the detrimental effects of corrosion. As infrastructure development continues to accelerate worldwide, particularly in emerging economies, the need for durable and long-lasting construction materials becomes more pronounced. Anti-corrosion coatings play a pivotal role in extending the lifespan of steel structures, reducing maintenance costs, and ensuring safety. The market's expansion is also driven by advancements in coating technologies, which offer enhanced protection and application efficiency. Furthermore, the growing emphasis on environmentally friendly coatings that minimize the use of volatile organic compounds (VOCs) and other harmful substances is expected to contribute to market growth. As regulatory bodies impose stricter environmental standards, the demand for eco-friendly coatings is likely to increase. In conclusion, the Global Anti-Corrosion Coating for Building Steel Structure Market is poised for significant growth, driven by the need for durable infrastructure and advancements in coating technologies.

| Report Metric | Details |

| Report Name | Anti-Corrosion Coating for Building Steel Structure Market |

| Accounted market size in year | US$ 6043 million |

| Forecasted market size in 2031 | US$ 8463 million |

| CAGR | 5.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BASF, DuPont, Evonik, Henkel, Solvay, Valspar, Berger Paints, Akzo Nobel, Sherwin Williams, Wacker Chemie, Nippon paint, PPG, Kansai Paints, Alumax Industrial, Aexcel Corporation, Hempel, Jotun, Chugoku Marine Paints, Arkema, RPM International |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |