What is Global Essential Fatty Acids for Fitness Market?

The Global Essential Fatty Acids for Fitness Market is a dynamic and rapidly evolving sector that focuses on the production and distribution of essential fatty acids (EFAs) specifically tailored for fitness enthusiasts and athletes. Essential fatty acids, such as omega-3 and omega-6, are crucial for maintaining optimal health and enhancing physical performance. These nutrients are not synthesized by the body and must be obtained through diet or supplementation. The market is driven by the increasing awareness of the health benefits associated with EFAs, including improved cardiovascular health, enhanced muscle recovery, and reduced inflammation. As more individuals adopt fitness-oriented lifestyles, the demand for high-quality EFA supplements has surged. This market encompasses a wide range of products, including capsules, powders, and fortified foods, catering to diverse consumer preferences. Additionally, the rise of e-commerce platforms has made these products more accessible to a global audience, further fueling market growth. Companies operating in this space are continually innovating to develop new formulations and delivery methods to meet the evolving needs of consumers. Overall, the Global Essential Fatty Acids for Fitness Market is poised for significant expansion as health-conscious individuals seek to optimize their fitness routines through targeted nutrition.

Linolenic Acid, Linoleic Acid in the Global Essential Fatty Acids for Fitness Market:

Linolenic acid and linoleic acid are two pivotal components within the Global Essential Fatty Acids for Fitness Market, each playing a unique role in supporting fitness and overall health. Linolenic acid, commonly known as alpha-linolenic acid (ALA), is a type of omega-3 fatty acid found in plant sources such as flaxseeds, chia seeds, and walnuts. ALA is renowned for its anti-inflammatory properties, which are particularly beneficial for athletes and fitness enthusiasts who experience muscle soreness and joint pain due to intense physical activity. By incorporating ALA into their diets, individuals can potentially reduce inflammation and enhance recovery times, allowing for more consistent and effective training sessions. Furthermore, ALA is a precursor to other omega-3 fatty acids like EPA and DHA, which are essential for brain health and cognitive function, making it a valuable addition to any fitness regimen.

On the other hand, linoleic acid is an omega-6 fatty acid predominantly found in vegetable oils, nuts, and seeds. It is an essential component of cell membranes and plays a crucial role in maintaining skin health and promoting wound healing. For fitness enthusiasts, linoleic acid is vital for energy production and muscle growth. It aids in the synthesis of arachidonic acid, which is involved in the regulation of muscle protein synthesis and the repair of damaged tissues. This makes linoleic acid an important nutrient for those looking to build muscle mass and improve overall physical performance. However, it is important to maintain a balanced intake of omega-6 and omega-3 fatty acids to prevent potential health issues associated with excessive omega-6 consumption, such as increased inflammation.

The Global Essential Fatty Acids for Fitness Market recognizes the significance of both linolenic and linoleic acids in supporting fitness goals. Manufacturers are increasingly incorporating these fatty acids into various products, including supplements, protein bars, and meal replacement shakes, to cater to the growing demand from health-conscious consumers. Additionally, there is a rising trend towards plant-based and vegan-friendly EFA supplements, driven by the increasing number of individuals adopting plant-based diets for health and ethical reasons. This shift has prompted companies to explore innovative sources of linolenic and linoleic acids, such as algae and hemp seeds, to provide sustainable and environmentally friendly options for consumers.

Moreover, the market is witnessing a surge in research and development activities aimed at enhancing the bioavailability and efficacy of linolenic and linoleic acid supplements. Advanced technologies, such as microencapsulation and nanotechnology, are being employed to improve the stability and absorption of these fatty acids, ensuring that consumers receive maximum benefits from their supplementation. As the understanding of the health benefits of linolenic and linoleic acids continues to grow, the Global Essential Fatty Acids for Fitness Market is expected to expand further, offering a wide array of products that cater to the diverse needs of fitness enthusiasts worldwide.

Gym, Supermarket, Other in the Global Essential Fatty Acids for Fitness Market:

The usage of Global Essential Fatty Acids for Fitness Market products spans various areas, including gyms, supermarkets, and other retail environments, each offering unique opportunities for consumers to access these essential nutrients. In gyms, essential fatty acid supplements are often marketed as part of a comprehensive fitness and wellness program. Fitness centers and personal trainers frequently recommend these supplements to clients as a means to enhance performance, support muscle recovery, and reduce inflammation. Many gyms have on-site retail sections where members can conveniently purchase EFA supplements, protein powders, and other nutritional products that complement their workout routines. Additionally, some fitness centers offer educational workshops and seminars to inform members about the benefits of essential fatty acids and how they can be integrated into a balanced diet to support fitness goals.

Supermarkets also play a crucial role in the distribution of essential fatty acid products, making them accessible to a broader consumer base. With the growing trend towards health and wellness, many supermarkets have expanded their offerings to include a wide range of EFA supplements, fortified foods, and beverages. These products are often strategically placed in health and wellness aisles, alongside other nutritional supplements and organic foods, to attract health-conscious shoppers. Supermarkets provide a convenient shopping experience for consumers looking to incorporate essential fatty acids into their daily diets, offering a variety of options to suit different preferences and dietary needs. Furthermore, supermarkets often collaborate with nutritionists and dietitians to provide in-store consultations and advice, helping customers make informed decisions about their nutritional choices.

Beyond gyms and supermarkets, essential fatty acid products are also available through various other channels, including online retailers, health food stores, and specialty nutrition shops. The rise of e-commerce has significantly expanded the reach of EFA products, allowing consumers to purchase them from the comfort of their homes. Online platforms offer a vast selection of products, often accompanied by detailed descriptions, customer reviews, and expert recommendations, enabling consumers to make well-informed purchasing decisions. Health food stores and specialty nutrition shops cater to niche markets, offering premium and specialized EFA products that may not be available in mainstream retail outlets. These stores often focus on organic, non-GMO, and sustainably sourced products, appealing to environmentally conscious consumers and those with specific dietary preferences.

In conclusion, the Global Essential Fatty Acids for Fitness Market is characterized by its diverse distribution channels, each catering to the unique needs and preferences of consumers. Whether through gyms, supermarkets, or other retail environments, essential fatty acid products are readily accessible to individuals seeking to enhance their fitness and overall health. As awareness of the benefits of EFAs continues to grow, the market is likely to see further expansion and innovation, offering consumers an ever-increasing array of options to support their fitness journeys.

Global Essential Fatty Acids for Fitness Market Outlook:

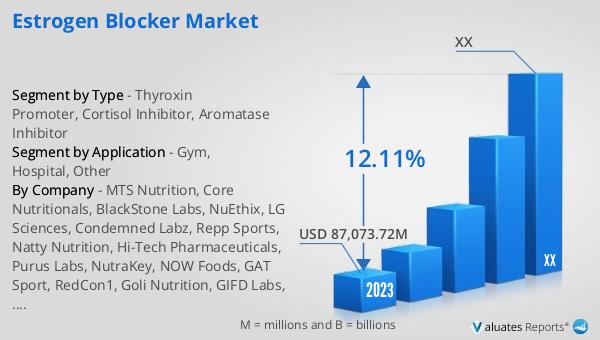

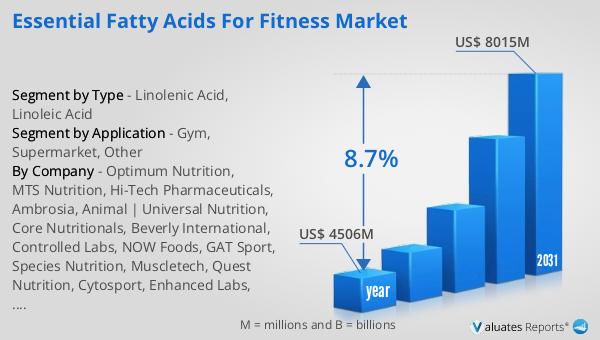

The global market for Essential Fatty Acids for Fitness was valued at $4,506 million in 2024 and is anticipated to grow significantly, reaching an estimated size of $8,015 million by 2031. This growth is projected to occur at a compound annual growth rate (CAGR) of 8.7% over the forecast period. This upward trend reflects the increasing demand for essential fatty acids as more individuals prioritize health and fitness in their lifestyles. In parallel, the health and fitness clubs market is also experiencing substantial growth. It is expected to expand from $87,073.72 million in 2023 to $154,208.70 million by 2028, with a CAGR of 12.11% during the forecast period from 2023 to 2028. This growth in the health and fitness sector underscores the rising interest in wellness and the adoption of fitness-oriented lifestyles. As consumers become more health-conscious, the demand for products that support fitness, such as essential fatty acids, is likely to continue its upward trajectory. This market outlook highlights the potential for significant opportunities and innovations within the Global Essential Fatty Acids for Fitness Market, driven by the growing emphasis on health and wellness across the globe.

| Report Metric |

Details |

| Report Name |

Essential Fatty Acids for Fitness Market |

| Accounted market size in year |

US$ 4506 million |

| Forecasted market size in 2031 |

US$ 8015 million |

| CAGR |

8.7% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

- Linolenic Acid

- Linoleic Acid

|

| Segment by Application |

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Optimum Nutrition, MTS Nutrition, Hi-Tech Pharmaceuticals, Ambrosia, Animal | Universal Nutrition, Core Nutritionals, Beverly International, Controlled Labs, NOW Foods, GAT Sport, Species Nutrition, Muscletech, Quest Nutrition, Cytosport, Enhanced Labs, Black Magic, NutraKey |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |