What is Global Fluid Heating Chamber Market?

The Global Fluid Heating Chamber Market is a specialized segment within the broader industrial equipment sector, focusing on devices designed to heat fluids to specific temperatures for various applications. These chambers are essential in processes where precise temperature control is crucial, such as in chemical reactions, industrial manufacturing, and medical applications. The market for these chambers is driven by the increasing demand for efficient and reliable heating solutions across different industries. Technological advancements have led to the development of more sophisticated and energy-efficient fluid heating chambers, which are capable of maintaining consistent temperatures and improving process efficiency. The market is characterized by a diverse range of products, including both standard and customized solutions, catering to the specific needs of different industries. As industries continue to seek ways to optimize their processes and reduce energy consumption, the demand for advanced fluid heating chambers is expected to grow. This market is also influenced by regulatory standards and environmental considerations, which drive the need for more sustainable and compliant heating solutions. Overall, the Global Fluid Heating Chamber Market plays a critical role in supporting industrial and technological advancements by providing essential heating solutions.

Glass Door, Solid Door in the Global Fluid Heating Chamber Market:

In the Global Fluid Heating Chamber Market, the choice between glass door and solid door designs is a significant consideration for users, as each type offers distinct advantages and is suited to different applications. Glass door fluid heating chambers are particularly valued for their visibility and accessibility. These chambers allow operators to monitor the contents without opening the door, which is crucial in maintaining a stable internal environment and preventing heat loss. This feature is especially beneficial in laboratory settings or in processes where constant observation is necessary. The transparency of glass doors also aids in ensuring safety and compliance, as operators can quickly identify any issues or irregularities within the chamber. However, glass doors may not provide the same level of insulation as solid doors, which can be a drawback in applications requiring stringent temperature control. On the other hand, solid door fluid heating chambers are known for their superior insulation properties. These doors are typically constructed from robust materials that offer excellent thermal retention, making them ideal for applications where maintaining a consistent temperature is critical. Solid doors are often preferred in industrial settings where the contents of the chamber do not require frequent monitoring, or where the risk of contamination must be minimized. The enhanced insulation of solid doors helps in reducing energy consumption, as less heat is lost to the surrounding environment. This can lead to cost savings over time, particularly in large-scale operations where energy efficiency is a priority. Additionally, solid doors provide a more secure barrier against external factors, such as dust or moisture, which can affect the performance of the heating chamber. The decision between glass and solid doors in fluid heating chambers often depends on the specific requirements of the application. For instance, in medical or pharmaceutical environments where sterility and precision are paramount, solid doors may be preferred to ensure that the internal conditions remain uncontaminated and stable. Conversely, in research and development settings where observation is key, glass doors might be more suitable. Manufacturers in the Global Fluid Heating Chamber Market offer a variety of options to cater to these diverse needs, often providing customizable solutions that allow users to select the door type that best fits their operational requirements. This flexibility is crucial in a market where the demands of different industries can vary significantly. Moreover, advancements in materials and design have led to improvements in both glass and solid door fluid heating chambers. For glass doors, innovations such as double-glazing and the use of specialized coatings have enhanced their insulation capabilities, reducing the trade-off between visibility and thermal efficiency. Similarly, solid doors have benefited from the development of lighter, more durable materials that improve their performance without adding excessive weight or bulk. These advancements have expanded the range of applications for fluid heating chambers, making them more versatile and adaptable to the changing needs of industries. In conclusion, the choice between glass door and solid door fluid heating chambers in the Global Fluid Heating Chamber Market is influenced by a variety of factors, including the specific requirements of the application, the need for visibility or insulation, and the operational environment. Both types of doors offer unique benefits and challenges, and the decision ultimately depends on the priorities of the user. As technology continues to evolve, the capabilities of both glass and solid door fluid heating chambers are likely to improve, offering even greater efficiency and functionality to meet the demands of modern industries.

Industrial, Medical, Chemical, Others in the Global Fluid Heating Chamber Market:

The Global Fluid Heating Chamber Market finds extensive usage across various sectors, including industrial, medical, chemical, and others, each with unique requirements and applications. In the industrial sector, fluid heating chambers are integral to processes that require precise temperature control, such as in the manufacturing of plastics, textiles, and food products. These chambers ensure that the fluids used in production are heated to the exact temperatures needed to achieve the desired chemical reactions or physical properties. This precision is crucial in maintaining product quality and consistency, as even slight variations in temperature can lead to defects or inefficiencies. Additionally, fluid heating chambers in industrial settings often need to handle large volumes of fluid, necessitating robust and reliable equipment that can operate continuously under demanding conditions. In the medical field, fluid heating chambers are used in a variety of applications, from sterilizing equipment to preparing solutions for patient care. These chambers must adhere to strict regulatory standards to ensure safety and efficacy, as they often deal with sensitive materials that can impact patient health. For example, in hospitals and laboratories, fluid heating chambers are used to warm intravenous fluids or blood products to body temperature before administration, preventing shock or discomfort in patients. The ability to maintain precise and consistent temperatures is critical in these applications, as deviations can compromise the safety and effectiveness of medical treatments. As such, fluid heating chambers used in the medical sector are designed with advanced controls and monitoring systems to ensure optimal performance. The chemical industry also relies heavily on fluid heating chambers for various processes, including synthesis, distillation, and extraction. In these applications, the chambers are used to heat solvents, reactants, or other fluids to specific temperatures to facilitate chemical reactions or separations. The ability to control temperature accurately is essential in the chemical industry, as it can affect reaction rates, yields, and product purity. Fluid heating chambers used in this sector are often equipped with features such as programmable temperature settings, rapid heating capabilities, and safety mechanisms to prevent overheating or accidents. These features help ensure that chemical processes are conducted efficiently and safely, minimizing the risk of errors or hazards. Beyond industrial, medical, and chemical applications, fluid heating chambers are also used in other areas such as research and development, environmental testing, and food processing. In research and development, these chambers provide the controlled conditions needed to conduct experiments and test new products or materials. Environmental testing often involves simulating specific temperature conditions to study the effects on materials or biological samples, making fluid heating chambers an essential tool in this field. In food processing, fluid heating chambers are used to pasteurize or sterilize products, ensuring they are safe for consumption and have a longer shelf life. Overall, the Global Fluid Heating Chamber Market serves a wide range of industries, each with its own set of requirements and challenges. The versatility and precision offered by these chambers make them indispensable tools in applications where temperature control is critical. As industries continue to evolve and demand more efficient and reliable heating solutions, the role of fluid heating chambers is likely to expand, driving further innovation and development in this market.

Global Fluid Heating Chamber Market Outlook:

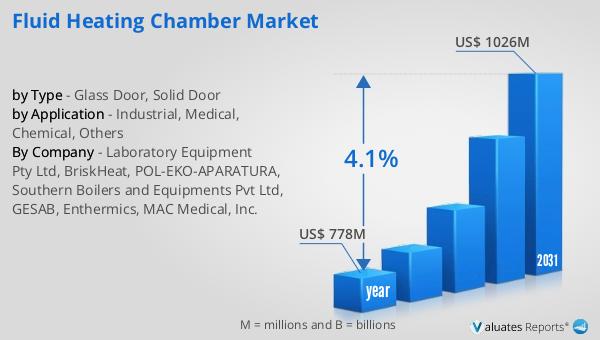

The outlook for the Global Fluid Heating Chamber Market indicates a promising growth trajectory. In 2024, the market was valued at approximately $778 million, and projections suggest it will reach around $1,026 million by 2031. This growth represents a compound annual growth rate (CAGR) of 4.1% over the forecast period. This steady increase in market size reflects the rising demand for fluid heating chambers across various industries, driven by the need for precise temperature control and energy-efficient solutions. As industries continue to seek ways to optimize their processes and reduce operational costs, the adoption of advanced fluid heating chambers is expected to rise. The market's growth is also supported by technological advancements that have led to the development of more sophisticated and reliable heating solutions. These innovations have expanded the range of applications for fluid heating chambers, making them more versatile and adaptable to the changing needs of industries. Additionally, regulatory standards and environmental considerations are influencing the market, as companies strive to comply with regulations and adopt more sustainable practices. Overall, the Global Fluid Heating Chamber Market is poised for continued growth, driven by the increasing demand for efficient and reliable heating solutions across various sectors.

| Report Metric | Details |

| Report Name | Fluid Heating Chamber Market |

| Accounted market size in year | US$ 778 million |

| Forecasted market size in 2031 | US$ 1026 million |

| CAGR | 4.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Laboratory Equipment Pty Ltd, BriskHeat, POL-EKO-APARATURA, Southern Boilers and Equipments Pvt Ltd, GESAB, Enthermics, MAC Medical, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |