What is Global Static RAM (Static Random-Access Memory,Sram) Market?

Global Static RAM (Static Random-Access Memory, SRAM) is a type of semiconductor memory that uses bistable latching circuitry to store each bit. Unlike Dynamic RAM (DRAM), which needs to be periodically refreshed, SRAM retains data bits in its memory as long as power is being supplied. This makes it faster and more reliable for certain applications. SRAM is commonly used in devices where speed is critical, such as in cache memory for processors, routers, and switches. It is also used in various consumer electronics, automotive applications, and communication devices. The global market for SRAM is driven by the increasing demand for high-speed and low-power memory solutions. As technology advances, the need for efficient memory solutions in various sectors continues to grow, making SRAM an essential component in modern electronic devices. The market is characterized by a few key players who dominate the industry, focusing on innovation and development to meet the evolving needs of different applications.

Quad Data Rate (Qdr), Double Data Rate (Ddr), Asynchronous Sram, Psram, Vsram in the Global Static RAM (Static Random-Access Memory,Sram) Market:

Quad Data Rate (QDR) SRAM is a type of SRAM that offers four data transfers per clock cycle, effectively doubling the data rate compared to Double Data Rate (DDR) SRAM, which provides two data transfers per clock cycle. QDR SRAM is particularly useful in high-performance applications such as networking and telecommunications, where rapid data access and transfer are crucial. It allows for simultaneous read and write operations, enhancing the efficiency of data handling. On the other hand, DDR SRAM is widely used in applications where moderate speed and power efficiency are required. It is commonly found in computer systems and consumer electronics, providing a balance between performance and power consumption. Asynchronous SRAM operates independently of a clock signal, making it suitable for applications where timing is not critical. It is often used in simpler devices where cost and power consumption are more important than speed. Pseudo SRAM (PSRAM) combines the features of DRAM and SRAM, offering a cost-effective solution with the speed of SRAM and the density of DRAM. It is used in mobile devices and other applications where space and cost are constraints. Volatile SRAM (VSRAM) retains data only while power is supplied, making it suitable for temporary data storage in various electronic devices. Each type of SRAM has its unique advantages and is chosen based on the specific requirements of the application, such as speed, power consumption, and cost. The global SRAM market continues to evolve with advancements in technology, offering a range of solutions to meet the diverse needs of different industries.

Computers/It, Communication, Automotive, Consumer Electronics, Modern Appliances, Electronic Toys, Synthesizers, Mobile Phones, Cameras in the Global Static RAM (Static Random-Access Memory,Sram) Market:

SRAM is extensively used in various sectors due to its speed and reliability. In the Computers/IT sector, SRAM is primarily used as cache memory in processors. It provides fast access to frequently used data, enhancing the overall performance of computer systems. In the communication sector, SRAM is used in routers and switches to manage data traffic efficiently. Its ability to handle high-speed data transfers makes it ideal for networking applications. In the automotive industry, SRAM is used in advanced driver-assistance systems (ADAS) and infotainment systems, where quick data access is crucial for real-time processing. Consumer electronics, such as gaming consoles and smart TVs, also rely on SRAM for fast data processing and smooth performance. Modern appliances, including smart refrigerators and washing machines, use SRAM to manage complex functions and improve energy efficiency. Electronic toys and synthesizers benefit from SRAM's speed and low power consumption, allowing for responsive and interactive experiences. Mobile phones and cameras use SRAM in their processors and image sensors to enhance performance and image quality. The versatility of SRAM makes it a valuable component in a wide range of applications, driving its demand in the global market.

Global Static RAM (Static Random-Access Memory,Sram) Market Outlook:

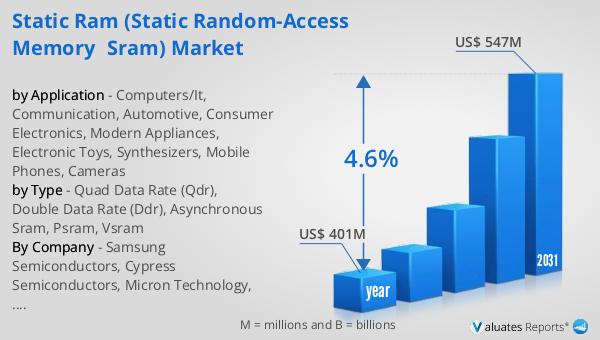

The global market for Static RAM (Static Random-Access Memory, SRAM) was valued at $401 million in 2024 and is anticipated to grow to a revised size of $547 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.6% during the forecast period. This growth is driven by the increasing demand for high-speed and low-power memory solutions across various industries. The market is dominated by a few key players, with the top three companies accounting for approximately 81% of the market share. These leading companies focus on innovation and development to maintain their competitive edge and meet the evolving needs of different applications. The SRAM market's growth is supported by advancements in technology and the increasing need for efficient memory solutions in sectors such as computing, communication, automotive, and consumer electronics. As the demand for faster and more reliable memory continues to rise, the SRAM market is expected to expand further, offering a range of solutions to meet the diverse needs of different industries.

| Report Metric | Details |

| Report Name | Static RAM (Static Random-Access Memory,Sram) Market |

| Accounted market size in year | US$ 401 million |

| Forecasted market size in 2031 | US$ 547 million |

| CAGR | 4.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Samsung Semiconductors, Cypress Semiconductors, Micron Technology, Integrated Silicon Solutions, Gsi Technology, Renesas Electronics Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |