What is Global Commercial Vehicle Air Suspension System Market?

The Global Commercial Vehicle Air Suspension System Market is a specialized segment within the automotive industry that focuses on the development and distribution of air suspension systems for commercial vehicles. These systems are designed to enhance the ride quality, handling, and overall performance of vehicles such as trucks, buses, and other heavy-duty vehicles. Unlike traditional suspension systems that rely on metal springs, air suspension systems use air-filled bags or bellows, which can be adjusted to provide a smoother ride and better load handling. This market is driven by the increasing demand for commercial vehicles that offer improved comfort and safety, as well as the need for vehicles that can efficiently handle varying loads and road conditions. The market is also influenced by technological advancements and regulatory requirements aimed at reducing vehicle emissions and improving fuel efficiency. As a result, manufacturers are investing in research and development to create more advanced and efficient air suspension systems that meet these demands. The market is expected to grow significantly in the coming years, driven by the expansion of the commercial vehicle industry and the increasing adoption of air suspension systems in various regions around the world.

Manual Air Suspension, Electronic Air Suspension in the Global Commercial Vehicle Air Suspension System Market:

Manual Air Suspension and Electronic Air Suspension are two primary types of air suspension systems used in the Global Commercial Vehicle Air Suspension System Market. Manual Air Suspension systems are relatively straightforward and rely on manual adjustments to control the air pressure within the suspension system. This type of system typically involves a manual valve or switch that allows the driver or operator to adjust the air pressure, thereby altering the ride height and stiffness of the suspension. Manual systems are often favored for their simplicity and cost-effectiveness, making them a popular choice for smaller commercial vehicles or applications where advanced features are not necessary. However, they require more effort and attention from the operator to maintain optimal performance, as adjustments must be made manually based on the load and road conditions. On the other hand, Electronic Air Suspension systems offer a more sophisticated and automated approach to managing vehicle suspension. These systems use electronic sensors and control units to continuously monitor and adjust the air pressure in the suspension system. This allows for real-time adjustments to the ride height and stiffness, providing a smoother and more comfortable ride regardless of the load or road conditions. Electronic systems can automatically adapt to changes in vehicle weight, speed, and terrain, ensuring optimal performance and safety. They often include features such as automatic leveling, which maintains a consistent ride height even when the vehicle is heavily loaded or traveling on uneven surfaces. This not only enhances comfort but also improves vehicle stability and handling. The adoption of Electronic Air Suspension systems is growing in the commercial vehicle market due to their advanced capabilities and the increasing demand for vehicles that offer superior comfort and performance. These systems are particularly beneficial for long-haul trucks and buses, where driver and passenger comfort is a priority. Additionally, electronic systems can contribute to improved fuel efficiency by optimizing the vehicle's aerodynamics and reducing drag. Despite their higher cost compared to manual systems, the benefits of electronic air suspension systems in terms of performance, safety, and efficiency make them an attractive option for many commercial vehicle operators. In summary, both Manual and Electronic Air Suspension systems play a crucial role in the Global Commercial Vehicle Air Suspension System Market. While manual systems offer simplicity and cost-effectiveness, electronic systems provide advanced features and automation that enhance vehicle performance and comfort. As the market continues to evolve, the demand for more sophisticated and efficient air suspension systems is expected to grow, driven by the need for commercial vehicles that can meet the challenges of modern transportation.

Light Commercial Vehicles, Heavy Trucks, Buses and Coaches in the Global Commercial Vehicle Air Suspension System Market:

The Global Commercial Vehicle Air Suspension System Market finds its application across various types of vehicles, including Light Commercial Vehicles (LCVs), Heavy Trucks, Buses, and Coaches. Each of these vehicle categories benefits from air suspension systems in unique ways, enhancing their performance, comfort, and efficiency. In Light Commercial Vehicles, air suspension systems are primarily used to improve ride quality and handling. These vehicles, which include vans and small trucks, often operate in urban environments where road conditions can vary significantly. Air suspension systems help to absorb shocks and vibrations, providing a smoother ride for both the driver and any cargo being transported. This is particularly important for vehicles that carry fragile goods, as it reduces the risk of damage during transit. Additionally, air suspension systems can improve the vehicle's load-carrying capacity by maintaining a consistent ride height, even when fully loaded. Heavy Trucks, which are used for long-haul transportation and heavy-duty applications, benefit greatly from air suspension systems. These systems enhance the truck's stability and handling, especially when carrying heavy or uneven loads. By automatically adjusting the suspension based on the load and road conditions, air suspension systems help to maintain optimal tire contact with the road, reducing wear and improving safety. This is crucial for heavy trucks that travel long distances, as it minimizes driver fatigue and enhances overall vehicle performance. Furthermore, air suspension systems can contribute to fuel efficiency by optimizing the truck's aerodynamics and reducing rolling resistance. Buses and Coaches, which prioritize passenger comfort, are another key area where air suspension systems are widely used. These vehicles often travel long distances and need to provide a comfortable ride for passengers. Air suspension systems help to achieve this by absorbing road shocks and vibrations, ensuring a smooth and comfortable journey. The ability to automatically adjust the suspension based on the number of passengers and road conditions also enhances safety and stability. Additionally, air suspension systems can lower the vehicle's ride height when stationary, making it easier for passengers to board and alight, which is particularly beneficial for elderly or disabled passengers. In conclusion, the Global Commercial Vehicle Air Suspension System Market plays a vital role in enhancing the performance and comfort of various types of commercial vehicles. Whether it's improving ride quality in Light Commercial Vehicles, enhancing stability and efficiency in Heavy Trucks, or ensuring passenger comfort in Buses and Coaches, air suspension systems offer significant benefits across the board. As the demand for more efficient and comfortable commercial vehicles continues to grow, the adoption of air suspension systems is expected to increase, driving further advancements in this market.

Global Commercial Vehicle Air Suspension System Market Outlook:

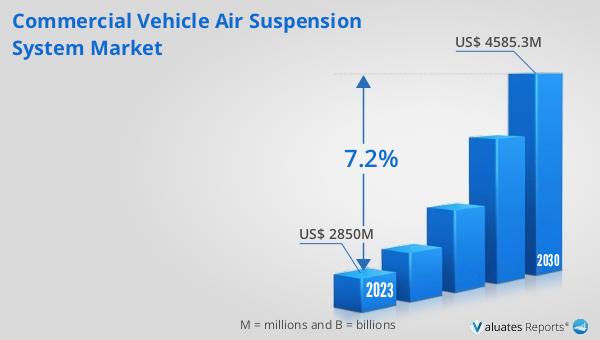

The outlook for the Global Commercial Vehicle Air Suspension System Market indicates a promising growth trajectory. The market is anticipated to expand from a valuation of US$ 3023 million in 2024 to reach approximately US$ 4585.3 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 7.2% over the forecast period. This upward trend is driven by several factors, including the increasing demand for commercial vehicles that offer enhanced comfort, safety, and performance. As the transportation and logistics industries continue to expand globally, there is a growing need for vehicles that can efficiently handle varying loads and road conditions. Air suspension systems, with their ability to provide a smoother ride and better load management, are becoming an essential component in modern commercial vehicles. Moreover, technological advancements in air suspension systems, such as the development of electronic control units and sensors, are further propelling market growth. These innovations enable more precise and automated adjustments to the suspension system, enhancing vehicle performance and fuel efficiency. Additionally, regulatory requirements aimed at reducing vehicle emissions and improving fuel economy are encouraging manufacturers to adopt more advanced suspension technologies. As a result, the market is witnessing increased investment in research and development to create more efficient and environmentally friendly air suspension systems. Overall, the Global Commercial Vehicle Air Suspension System Market is poised for significant growth, driven by the increasing demand for advanced suspension solutions in the commercial vehicle sector.

| Report Metric | Details |

| Report Name | Commercial Vehicle Air Suspension System Market |

| Accounted market size in 2024 | US$ 3023 million |

| Forecasted market size in 2030 | US$ 4585.3 million |

| CAGR | 7.2 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

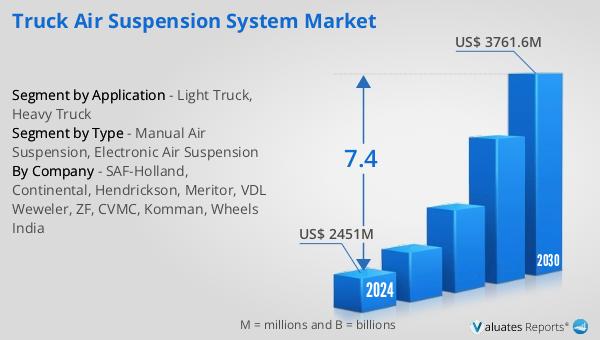

| By Company | SAF-Holland, Continental, Hendrickson, Meritor, VDL Weweler, ZF, CVMC, Komman, Wheels India |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |