What is Global Well Casing & Cementing Market?

The Global Well Casing & Cementing Market is a crucial segment of the oil and gas industry, focusing on the processes and equipment used to ensure the structural integrity of oil and gas wells. Well casing involves the installation of steel pipes into a drilled well to stabilize the wellbore, prevent contamination of water zones, and control well pressures. Cementing, on the other hand, involves pumping cement between the casing and the wellbore to secure the casing in place and prevent fluid migration between subsurface formations. This market is driven by the need for efficient and safe extraction of oil and gas resources, as well as the increasing exploration activities in both onshore and offshore environments. Technological advancements and the growing demand for energy are also significant factors contributing to the market's expansion. The market encompasses a wide range of products and services, including casing pipes, cementing equipment, and various services that ensure the proper installation and maintenance of well casings and cementing. As the energy sector continues to evolve, the Global Well Casing & Cementing Market plays a vital role in supporting the industry's infrastructure and operational efficiency.

Casing Pipe, Cementing Equipment, Casing Equipment, Services in the Global Well Casing & Cementing Market:

Casing pipes are fundamental components in the well casing process, serving as the primary structural element that lines the wellbore. These pipes are typically made of steel and come in various sizes and grades to accommodate different well conditions and depths. The selection of casing pipes is critical, as they must withstand the pressures and temperatures encountered during drilling and production. Cementing equipment, on the other hand, includes a range of tools and machinery used to mix, pump, and place cement in the annular space between the casing and the wellbore. This equipment ensures that the cement is properly distributed and bonded to both the casing and the formation, providing a seal that prevents fluid migration and enhances well integrity. Casing equipment encompasses various tools and accessories used to install and secure the casing pipes within the wellbore. This includes centralizers, which help position the casing in the center of the wellbore, and float equipment, which aids in the placement of the casing and cement. Services in the Global Well Casing & Cementing Market include a wide range of activities, from well planning and design to the execution of casing and cementing operations. These services are provided by specialized companies that have the expertise and technology to ensure that wells are constructed safely and efficiently. The integration of advanced technologies, such as real-time monitoring and automated systems, has enhanced the precision and reliability of these services, contributing to the overall success of well construction projects. As the demand for energy continues to rise, the Global Well Casing & Cementing Market is poised to play a critical role in supporting the exploration and production activities of the oil and gas industry.

Onshore, Offshore in the Global Well Casing & Cementing Market:

The usage of the Global Well Casing & Cementing Market in onshore and offshore environments is essential for the successful extraction of oil and gas resources. Onshore drilling involves the exploration and production of oil and gas from land-based wells. In this context, well casing and cementing are crucial for maintaining the structural integrity of the well and preventing environmental contamination. The onshore segment of the market is characterized by a wide range of geological conditions, requiring a diverse array of casing and cementing solutions to address the specific challenges of each well. Offshore drilling, on the other hand, involves the extraction of oil and gas from beneath the ocean floor. This environment presents unique challenges, such as high pressures, corrosive conditions, and the need for specialized equipment to operate in deepwater and ultra-deepwater settings. In offshore drilling, well casing and cementing are vital for ensuring the safety and stability of the well, as well as preventing blowouts and other catastrophic events. The Global Well Casing & Cementing Market provides the necessary tools, equipment, and services to address these challenges, enabling the safe and efficient extraction of resources from both onshore and offshore locations. As the industry continues to expand into more complex and challenging environments, the role of well casing and cementing becomes increasingly important in ensuring the success and sustainability of oil and gas operations.

Global Well Casing & Cementing Market Outlook:

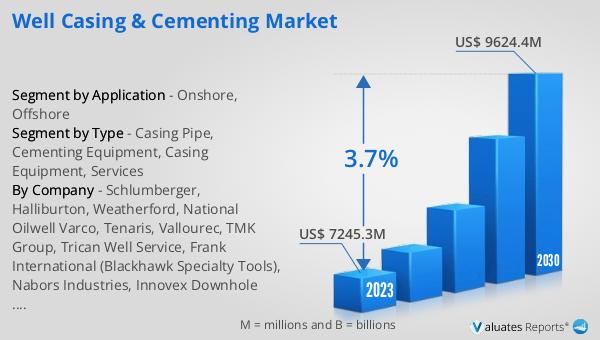

The outlook for the Global Well Casing & Cementing Market indicates a steady growth trajectory over the coming years. The market is anticipated to expand from a valuation of approximately $7,739.3 million in 2024 to around $9,624.4 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.7% during the forecast period. This upward trend is driven by several factors, including the increasing demand for energy, the expansion of exploration and production activities, and the ongoing advancements in drilling and well construction technologies. As the global energy landscape evolves, the need for efficient and reliable well casing and cementing solutions becomes more pronounced, supporting the market's growth. The market's expansion is also supported by the rising investments in oil and gas infrastructure, as well as the growing focus on enhancing the safety and environmental sustainability of drilling operations. As a result, the Global Well Casing & Cementing Market is poised to play a pivotal role in the future of the oil and gas industry, providing the essential tools and services needed to meet the world's energy demands.

| Report Metric | Details |

| Report Name | Well Casing & Cementing Market |

| Accounted market size in 2024 | US$ 7739.3 million |

| Forecasted market size in 2030 | US$ 9624.4 million |

| CAGR | 3.7 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Schlumberger, Halliburton, Weatherford, National Oilwell Varco, Tenaris, Vallourec, TMK Group, Trican Well Service, Frank International (Blackhawk Specialty Tools), Nabors Industries, Innovex Downhole Solutions, Centek Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |