What is Global District Heating And Cooling Systems Market?

The Global District Heating and Cooling Systems Market refers to the industry that provides centralized heating and cooling solutions to various sectors, including residential, commercial, and industrial areas. These systems are designed to distribute thermal energy in the form of hot water, steam, or chilled water from a central source to multiple buildings through a network of insulated pipes. This approach is more efficient and environmentally friendly compared to individual heating and cooling systems, as it allows for the use of renewable energy sources and waste heat recovery. The market for these systems is expanding due to increasing urbanization, the need for energy efficiency, and the growing awareness of environmental sustainability. As cities grow and the demand for energy-efficient solutions rises, district heating and cooling systems offer a viable solution to reduce carbon footprints and manage energy consumption more effectively. The market is also driven by technological advancements and government initiatives promoting clean energy solutions. Overall, the Global District Heating and Cooling Systems Market plays a crucial role in shaping the future of urban energy management by providing sustainable and efficient heating and cooling solutions.

District Heating, District Cooling in the Global District Heating And Cooling Systems Market:

District heating and cooling systems are integral components of modern urban infrastructure, providing efficient and sustainable thermal energy solutions. District heating involves the centralized production of heat, which is then distributed to residential, commercial, and industrial buildings through a network of insulated pipes. This system typically uses a variety of energy sources, including fossil fuels, biomass, geothermal energy, and waste heat from industrial processes or power plants. The centralized nature of district heating allows for greater efficiency and reduced emissions compared to individual heating systems. By utilizing waste heat and renewable energy sources, district heating systems contribute to reducing the carbon footprint of urban areas. On the other hand, district cooling systems work on a similar principle but focus on providing chilled water for air conditioning purposes. These systems are particularly beneficial in densely populated urban areas where individual air conditioning units can be inefficient and environmentally taxing. District cooling systems often use absorption chillers, which can be powered by waste heat or renewable energy, to produce chilled water that is then distributed to buildings. This approach not only reduces energy consumption but also minimizes the urban heat island effect, which is a common issue in large cities. The integration of district heating and cooling systems into urban planning is becoming increasingly important as cities strive to become more sustainable and resilient. These systems offer a reliable and cost-effective solution for managing energy demand and reducing greenhouse gas emissions. Moreover, they provide flexibility in terms of energy sources, allowing cities to adapt to changing energy landscapes and incorporate more renewable energy into their grids. The global market for district heating and cooling systems is witnessing significant growth, driven by factors such as increasing urbanization, the need for energy efficiency, and government initiatives promoting clean energy solutions. As cities continue to expand and the demand for sustainable energy solutions rises, district heating and cooling systems are poised to play a crucial role in shaping the future of urban energy management.

Residential, Commercial, Industrial in the Global District Heating And Cooling Systems Market:

The usage of Global District Heating and Cooling Systems Market in residential, commercial, and industrial areas highlights the versatility and efficiency of these systems in meeting diverse energy needs. In residential areas, district heating and cooling systems provide a reliable and efficient source of thermal energy for heating and cooling homes. By connecting multiple households to a centralized system, these solutions reduce the need for individual heating and cooling units, leading to lower energy consumption and reduced emissions. Residents benefit from consistent and comfortable indoor temperatures, while also contributing to environmental sustainability. In commercial areas, district heating and cooling systems offer significant advantages in terms of energy efficiency and cost savings. Large commercial buildings, such as office complexes, shopping malls, and hotels, require substantial amounts of energy for heating and cooling. By utilizing a centralized system, these buildings can achieve greater efficiency and reduce operational costs. Additionally, district systems allow for better load management, ensuring that energy is distributed according to demand and minimizing waste. In industrial areas, district heating and cooling systems play a crucial role in optimizing energy use and reducing emissions. Industrial processes often generate significant amounts of waste heat, which can be captured and utilized in district heating systems. This not only improves the overall efficiency of industrial operations but also reduces the reliance on fossil fuels. Furthermore, district cooling systems can provide efficient cooling solutions for industrial facilities, helping to maintain optimal operating conditions and improve productivity. Overall, the Global District Heating and Cooling Systems Market offers a comprehensive solution for managing energy needs across residential, commercial, and industrial sectors. By providing efficient and sustainable thermal energy solutions, these systems contribute to reducing carbon footprints, lowering energy costs, and enhancing the resilience of urban infrastructure. As the demand for energy-efficient solutions continues to grow, district heating and cooling systems are set to play an increasingly important role in shaping the future of energy management.

Global District Heating And Cooling Systems Market Outlook:

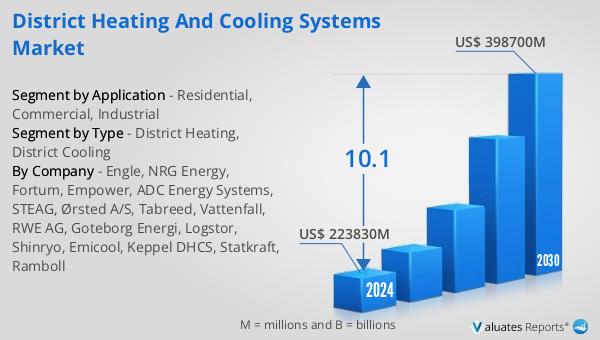

The outlook for the Global District Heating and Cooling Systems Market indicates a promising growth trajectory over the coming years. The market is anticipated to expand from a valuation of US$ 223,830 million in 2024 to an impressive US$ 398,700 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 10.1% during the forecast period. This robust growth can be attributed to several factors, including the increasing demand for energy-efficient solutions, the rising awareness of environmental sustainability, and the ongoing urbanization trends across the globe. As cities continue to expand and the need for sustainable energy solutions becomes more pressing, district heating and cooling systems offer a viable and effective means of managing energy consumption and reducing carbon emissions. The market is also benefiting from technological advancements and supportive government policies that promote the adoption of clean energy solutions. These factors are driving the expansion of district heating and cooling systems, making them an integral part of modern urban infrastructure. As the market continues to grow, it is expected to play a crucial role in shaping the future of energy management, providing efficient and sustainable solutions for heating and cooling needs across various sectors.

| Report Metric | Details |

| Report Name | District Heating And Cooling Systems Market |

| Accounted market size in 2024 | US$ 223830 million |

| Forecasted market size in 2030 | US$ 398700 million |

| CAGR | 10.1 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Engle, NRG Energy, Fortum, Empower, ADC Energy Systems, STEAG, Ørsted A/S, Tabreed, Vattenfall, RWE AG, Goteborg Energi, Logstor, Shinryo, Emicool, Keppel DHCS, Statkraft, Ramboll |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |