What is Global Centrifugal Air Compressor Market?

The Global Centrifugal Air Compressor Market refers to the worldwide industry focused on the production, distribution, and utilization of centrifugal air compressors. These compressors are mechanical devices that convert power into potential energy stored in pressurized air. They operate by using a rotating impeller to increase the velocity of air, which is then converted into pressure energy. Centrifugal air compressors are widely used across various industries due to their ability to deliver a continuous flow of compressed air, making them ideal for applications requiring large volumes of air at constant pressure. The market encompasses a range of products and services, including the manufacturing of compressors, sales, after-sales services, and maintenance. The demand for centrifugal air compressors is driven by their efficiency, reliability, and ability to handle high-capacity operations. Industries such as manufacturing, oil and gas, energy, and food and beverages are significant consumers of these compressors, utilizing them for various applications like powering pneumatic tools, conveying materials, and operating machinery. As industries continue to expand and modernize, the need for efficient and reliable air compression solutions is expected to grow, further propelling the market.

Portable, Stationary in the Global Centrifugal Air Compressor Market:

In the Global Centrifugal Air Compressor Market, products can be broadly categorized into portable and stationary compressors, each serving distinct purposes and catering to different industry needs. Portable centrifugal air compressors are designed for mobility and flexibility, making them ideal for applications where the compressor needs to be moved frequently or used in multiple locations. These compressors are commonly used in construction sites, road maintenance, and other outdoor projects where compressed air is needed on the go. Their compact design and ease of transportation allow for quick deployment and efficient operation in various environments. Portable compressors are typically smaller in size and capacity compared to their stationary counterparts, but they offer the advantage of being easily maneuverable and adaptable to changing work conditions. On the other hand, stationary centrifugal air compressors are designed for permanent installation in a fixed location, usually within industrial facilities or manufacturing plants. These compressors are built to handle high-capacity operations and provide a continuous supply of compressed air for extended periods. Stationary compressors are often larger and more powerful, capable of delivering higher pressure and volume outputs to meet the demands of large-scale industrial applications. They are commonly used in manufacturing processes, oil and gas refineries, power generation plants, and other industries where a reliable and consistent source of compressed air is essential. The choice between portable and stationary compressors depends on several factors, including the specific requirements of the application, the available space for installation, and the need for mobility. While portable compressors offer flexibility and convenience, stationary compressors provide the power and capacity needed for heavy-duty operations. Both types of compressors play a crucial role in the global market, catering to the diverse needs of industries worldwide. As technology advances and industries continue to evolve, the demand for both portable and stationary centrifugal air compressors is expected to grow, driven by the need for efficient and reliable air compression solutions.

Food and Beverages, Oil and Gas, Energy, Semiconductor and Electronics, Manufacturing, Others in the Global Centrifugal Air Compressor Market:

The Global Centrifugal Air Compressor Market finds extensive usage across various industries, each leveraging the unique capabilities of these compressors to enhance their operations. In the food and beverages industry, centrifugal air compressors are used to power pneumatic systems for packaging, bottling, and conveying products. They ensure a clean and oil-free air supply, which is crucial for maintaining hygiene and quality standards in food processing. The oil and gas industry relies on centrifugal air compressors for a range of applications, including gas compression, pipeline transportation, and enhanced oil recovery. These compressors are essential for maintaining pressure levels in pipelines and ensuring the efficient transportation of natural gas and other hydrocarbons. In the energy sector, centrifugal air compressors play a vital role in power generation and distribution. They are used in gas turbine power plants to provide compressed air for combustion, improving the efficiency and output of the turbines. Additionally, they are employed in renewable energy projects, such as wind and solar power, to store and manage energy. The semiconductor and electronics industry utilizes centrifugal air compressors for precision manufacturing processes, where clean and stable compressed air is required for operating sensitive equipment and maintaining controlled environments. In the manufacturing sector, these compressors are used for a wide range of applications, including powering pneumatic tools, operating machinery, and controlling automated systems. They provide the necessary air pressure to drive production lines and ensure smooth and efficient operations. Other industries, such as pharmaceuticals, chemicals, and automotive, also benefit from the use of centrifugal air compressors, leveraging their reliability and efficiency to optimize processes and reduce operational costs. As industries continue to innovate and expand, the demand for centrifugal air compressors is expected to grow, driven by the need for high-performance and energy-efficient air compression solutions.

Global Centrifugal Air Compressor Market Outlook:

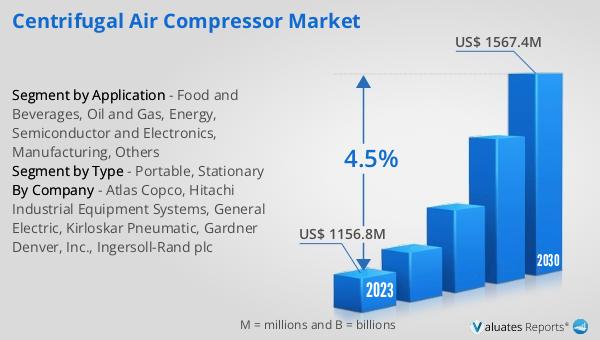

The outlook for the Global Centrifugal Air Compressor Market indicates a promising growth trajectory over the coming years. The market is anticipated to expand from a valuation of approximately US$ 1203.6 million in 2024 to around US$ 1567.4 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 4.5% during the forecast period. This upward trend can be attributed to several factors, including the increasing demand for energy-efficient and reliable air compression solutions across various industries. As industries continue to modernize and adopt advanced technologies, the need for high-performance centrifugal air compressors is expected to rise. Additionally, the growing emphasis on sustainability and reducing carbon footprints is driving the adoption of energy-efficient compressors, further boosting market growth. The expansion of industries such as manufacturing, oil and gas, energy, and food and beverages is also contributing to the increased demand for centrifugal air compressors. These industries rely on compressed air for a wide range of applications, from powering machinery to maintaining pressure levels in pipelines. As a result, the market is poised for steady growth, driven by the need for efficient and reliable air compression solutions.

| Report Metric | Details |

| Report Name | Centrifugal Air Compressor Market |

| Accounted market size in 2024 | US$ 1203.6 million |

| Forecasted market size in 2030 | US$ 1567.4 million |

| CAGR | 4.5 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Atlas Copco, Hitachi Industrial Equipment Systems, General Electric, Kirloskar Pneumatic, Gardner Denver, Inc., Ingersoll-Rand plc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |