What is Global Fully Automatic Vending Machines Market?

The Global Fully Automatic Vending Machines Market refers to the worldwide industry focused on the production, distribution, and utilization of vending machines that operate without human intervention. These machines are designed to dispense a variety of products, ranging from snacks and beverages to electronics and personal care items, with the simple push of a button or tap of a screen. The market has seen significant growth due to advancements in technology, which have enhanced the efficiency and user-friendliness of these machines. Features such as cashless payment options, touch screens, and remote monitoring have made fully automatic vending machines more appealing to both consumers and businesses. Additionally, the convenience offered by these machines aligns well with the fast-paced lifestyle of modern consumers, who often seek quick and easy access to products. As urbanization continues to rise globally, the demand for such vending solutions is expected to increase, making the Global Fully Automatic Vending Machines Market a dynamic and evolving sector. The market's expansion is also driven by the increasing need for automation in retail and the growing trend of self-service technologies.

Single Product Vending Machines, Multiple Product Vending Machines in the Global Fully Automatic Vending Machines Market:

Single Product Vending Machines and Multiple Product Vending Machines are two primary categories within the Global Fully Automatic Vending Machines Market. Single Product Vending Machines are designed to dispense only one type of product. These machines are often used for high-demand items such as bottled water, soda, or specific snacks. They are typically found in locations where there is a consistent demand for a particular product, such as gyms, schools, or office buildings. The simplicity of these machines makes them easy to maintain and operate, as they require less frequent restocking and have fewer mechanical components that can fail. On the other hand, Multiple Product Vending Machines offer a variety of products within a single unit. These machines are more complex and are often equipped with advanced technology to manage inventory and transactions. They are commonly found in places with diverse consumer needs, such as airports, shopping malls, and hospitals. Multiple Product Vending Machines can include a mix of snacks, beverages, and even non-food items like electronics or personal care products. The versatility of these machines makes them a popular choice for locations with high foot traffic and varied consumer preferences. Both types of vending machines benefit from technological advancements that enhance their functionality and user experience. For instance, many modern vending machines are equipped with digital displays, cashless payment systems, and remote monitoring capabilities. These features not only improve the convenience for consumers but also provide valuable data to operators about sales trends and inventory levels. This data can be used to optimize product offerings and improve the overall efficiency of vending operations. Furthermore, the integration of IoT (Internet of Things) technology allows vending machines to communicate with operators in real-time, alerting them to issues such as low stock levels or technical malfunctions. This proactive approach to maintenance and inventory management helps to minimize downtime and ensure a consistent supply of products to consumers. As the Global Fully Automatic Vending Machines Market continues to evolve, both Single Product and Multiple Product Vending Machines are expected to play a crucial role in meeting the diverse needs of consumers and businesses alike.

Shopping Center, Retail Stores, Hotel, Other in the Global Fully Automatic Vending Machines Market:

The usage of Global Fully Automatic Vending Machines Market extends across various sectors, including shopping centers, retail stores, hotels, and other areas. In shopping centers, vending machines provide a convenient solution for shoppers looking for quick snacks or beverages without having to wait in long lines at food courts. These machines are strategically placed in high-traffic areas to maximize visibility and accessibility. They often offer a range of products, from healthy snacks to indulgent treats, catering to the diverse preferences of shoppers. In retail stores, vending machines serve as an additional revenue stream by offering products that complement the store's main offerings. For example, a clothing store might have a vending machine that sells accessories or personal care items. This not only enhances the shopping experience for customers but also increases the store's profitability. In hotels, vending machines are a valuable amenity for guests who may need a quick snack or beverage outside of restaurant hours. They are typically located in common areas such as lobbies or near elevators for easy access. Some hotels even offer vending machines with travel essentials like toiletries or phone chargers, providing added convenience for guests. Beyond these traditional settings, vending machines are also found in a variety of other locations, such as schools, hospitals, and office buildings. In schools, they provide students with access to snacks and drinks during breaks, while in hospitals, they offer a convenient option for visitors and staff who may not have time to visit the cafeteria. In office buildings, vending machines serve as a quick and easy solution for employees looking for a snack or drink during their workday. The versatility and convenience of fully automatic vending machines make them an attractive option for a wide range of settings, and their usage is expected to continue growing as more businesses recognize the benefits they offer.

Global Fully Automatic Vending Machines Market Outlook:

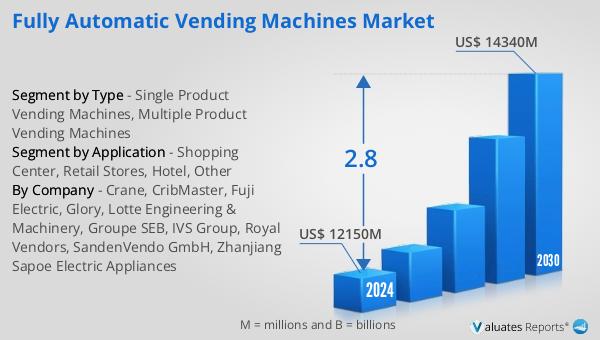

The outlook for the Global Fully Automatic Vending Machines Market indicates a steady growth trajectory over the coming years. According to projections, the market is expected to expand from a valuation of US$ 12,150 million in 2024 to approximately US$ 14,340 million by 2030. This growth represents a Compound Annual Growth Rate (CAGR) of 2.8% during the forecast period. This positive trend can be attributed to several factors, including the increasing demand for convenient and efficient retail solutions, advancements in vending machine technology, and the growing popularity of cashless payment systems. As consumers continue to seek quick and easy access to products, the demand for fully automatic vending machines is likely to rise. Additionally, businesses are recognizing the potential of these machines to enhance customer experience and generate additional revenue streams. The integration of advanced features such as touch screens, remote monitoring, and IoT capabilities further enhances the appeal of vending machines, making them a valuable asset for businesses across various sectors. As the market continues to evolve, it is expected to offer new opportunities for innovation and growth, driven by changing consumer preferences and technological advancements.

| Report Metric | Details |

| Report Name | Fully Automatic Vending Machines Market |

| Accounted market size in 2024 | US$ 12150 million |

| Forecasted market size in 2030 | US$ 14340 million |

| CAGR | 2.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Crane, CribMaster, Fuji Electric, Glory, Lotte Engineering & Machinery, Groupe SEB, IVS Group, Royal Vendors, SandenVendo GmbH, Zhanjiang Sapoe Electric Appliances |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |