What is Global Retail Shelving and Racks Market?

The Global Retail Shelving and Racks Market is a crucial component of the retail industry, providing the necessary infrastructure for displaying products in stores. These shelving and rack systems are designed to optimize space, enhance product visibility, and improve the overall shopping experience for customers. They come in various materials, sizes, and designs to cater to different retail environments, from small boutiques to large supermarkets. The market is driven by the need for efficient space utilization and the growing demand for organized and aesthetically pleasing store layouts. Retailers are increasingly investing in advanced shelving solutions to accommodate a wide range of products and to create a more engaging shopping environment. The market is also influenced by trends such as the rise of e-commerce, which has led to changes in physical store layouts, and the increasing focus on sustainability, prompting the use of eco-friendly materials in shelving systems. Overall, the Global Retail Shelving and Racks Market plays a vital role in the retail sector, helping businesses to effectively display their products and attract customers.

Metal Shelving System, Wood Shelving System, Others in the Global Retail Shelving and Racks Market:

In the Global Retail Shelving and Racks Market, different types of shelving systems are used to meet the diverse needs of retailers. Metal shelving systems are popular due to their durability, strength, and versatility. They are often used in environments that require heavy-duty storage solutions, such as warehouses and large retail stores. Metal shelves can support a significant amount of weight, making them ideal for storing bulk items or heavy products. They are also resistant to wear and tear, which ensures a long lifespan even in high-traffic areas. Additionally, metal shelving systems can be easily customized with various accessories like hooks, baskets, and dividers to enhance their functionality. Wood shelving systems, on the other hand, are favored for their aesthetic appeal and ability to create a warm and inviting atmosphere in retail spaces. They are commonly used in boutique stores, high-end retail outlets, and places where the visual presentation of products is crucial. Wood shelves can be crafted in various finishes and styles, allowing retailers to align their store design with their brand image. While they may not be as robust as metal shelves, wood shelving systems offer a unique charm and elegance that can enhance the overall shopping experience. Apart from metal and wood, there are other shelving systems available in the market that cater to specific needs. For instance, glass shelving systems are often used in luxury retail stores to display high-end products like jewelry and cosmetics. They provide a sleek and modern look, allowing products to stand out. Plastic shelving systems are another option, known for their lightweight and cost-effectiveness. They are suitable for temporary displays or areas where frequent reconfiguration is needed. Additionally, wire shelving systems are popular in grocery stores and supermarkets due to their open design, which allows for better air circulation and visibility of products. Each type of shelving system has its own advantages and is chosen based on the specific requirements of the retail environment. Retailers must consider factors such as the type of products being displayed, the available space, and the overall store design when selecting shelving solutions. By choosing the right shelving system, retailers can optimize their store layout, improve product accessibility, and create an inviting shopping atmosphere for customers.

Department Stores, Grocery, Hypermarket & Supermarket, Pharmacy, Others in the Global Retail Shelving and Racks Market:

The usage of Global Retail Shelving and Racks Market solutions varies across different retail sectors, each with its unique requirements and challenges. In department stores, shelving and racks are essential for organizing a wide range of products, from clothing and accessories to home goods and electronics. These stores often use a combination of shelving systems to create distinct sections and enhance the shopping experience. Adjustable shelving units are particularly useful in department stores, allowing for flexibility in product displays and easy reconfiguration to accommodate seasonal changes or promotional events. In grocery stores, shelving systems play a crucial role in ensuring the efficient display and accessibility of products. Gondola shelving is commonly used in grocery stores due to its versatility and ability to maximize space. These shelves can be easily adjusted to fit different product sizes and are often equipped with additional features like end caps for promotional displays. Wire shelving is also popular in grocery stores, especially in areas like produce sections, where air circulation is important to maintain the freshness of products. Hypermarkets and supermarkets require robust shelving solutions to handle the large volume of products they offer. These stores often use heavy-duty metal shelving systems to support bulk items and ensure stability. The layout of shelving in hypermarkets and supermarkets is strategically designed to guide customers through the store and encourage impulse purchases. End-of-aisle displays and promotional racks are commonly used to highlight special offers and new products. Pharmacies have specific shelving needs due to the nature of the products they sell. Shelving systems in pharmacies must ensure easy access to medications and health products while maintaining a clean and organized appearance. Modular shelving units are often used in pharmacies, allowing for customization and efficient use of space. Additionally, pharmacies may use lockable cabinets or secure shelving for storing controlled substances and high-value items. Other retail sectors, such as electronics stores, bookstores, and specialty shops, also rely on shelving and racks to display their products effectively. In electronics stores, shelving systems must accommodate a variety of product sizes and weights, from small gadgets to large appliances. Bookstores often use wooden shelving to create a cozy and inviting atmosphere, while specialty shops may require custom shelving solutions to showcase unique products. Overall, the Global Retail Shelving and Racks Market provides essential solutions for various retail sectors, helping businesses to organize their products, optimize space, and create an appealing shopping environment. By selecting the right shelving systems, retailers can enhance the customer experience, improve product visibility, and ultimately drive sales.

Global Retail Shelving and Racks Market Outlook:

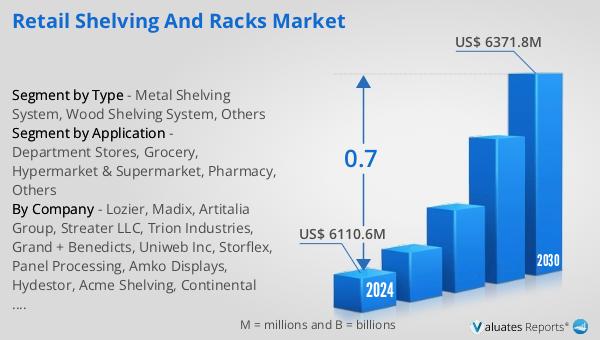

The outlook for the Global Retail Shelving and Racks Market indicates a steady growth trajectory over the coming years. The market is expected to expand from $6,110.6 million in 2024 to $6,371.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 0.7% during the forecast period. This growth is driven by several factors, including the increasing demand for efficient and aesthetically pleasing retail environments, the need for effective space utilization, and the rising trend of organized store layouts. As retailers continue to invest in advanced shelving solutions to enhance the shopping experience and accommodate a diverse range of products, the market is poised for sustained growth. Additionally, the shift towards sustainable and eco-friendly materials in shelving systems is expected to contribute to market expansion. Retailers are increasingly focusing on creating engaging and visually appealing store environments to attract customers and drive sales, further fueling the demand for innovative shelving and rack solutions. Overall, the Global Retail Shelving and Racks Market is set to experience moderate growth, supported by evolving retail trends and the continuous need for efficient product display solutions.

| Report Metric | Details |

| Report Name | Retail Shelving and Racks Market |

| Accounted market size in 2024 | US$ 6110.6 in million |

| Forecasted market size in 2030 | US$ 6371.8 million |

| CAGR | 0.7 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Lozier, Madix, Artitalia Group, Streater LLC, Trion Industries, Grand + Benedicts, Uniweb Inc, Storflex, Panel Processing, Amko Displays, Hydestor, Acme Shelving, Continental Store Fixture, Nabco, Handy Store Fixtures, Sumetall, CAEM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |