What is Global Aftershave Lotions & Creams Market?

The global aftershave lotions and creams market is a dynamic segment within the personal care industry, catering to the grooming needs of men worldwide. Aftershave products are designed to soothe and protect the skin after shaving, reducing irritation and providing a refreshing feel. These products come in various forms, including lotions, creams, balms, and splashes, each offering unique benefits. The market is driven by increasing awareness of personal grooming and skincare among men, along with the rising influence of social media and celebrity endorsements. Additionally, the growing trend of maintaining a well-groomed appearance in professional and social settings has further fueled the demand for aftershave products. The market is characterized by a wide range of products catering to different skin types and preferences, from alcohol-based splashes that provide a cooling sensation to moisturizing creams that offer hydration and nourishment. As consumer preferences continue to evolve, manufacturers are focusing on innovation and product differentiation to capture a larger share of the market. The global aftershave lotions and creams market is poised for steady growth, driven by the increasing emphasis on personal grooming and the expanding male grooming industry.

Lotions & Balm, Splash in the Global Aftershave Lotions & Creams Market:

Lotions and balms, as well as splash products, play a significant role in the global aftershave lotions and creams market, each catering to different consumer needs and preferences. Lotions and balms are typically designed to provide moisture and soothe the skin after shaving. They are often enriched with ingredients like aloe vera, chamomile, and vitamin E, which help to calm irritation and provide hydration. These products are particularly popular among individuals with sensitive skin, as they offer a gentle and nourishing post-shave experience. Lotions and balms are usually thicker in consistency compared to splashes, providing a protective barrier that locks in moisture and prevents dryness. On the other hand, splash products are alcohol-based solutions that offer a refreshing and invigorating sensation after shaving. They are known for their antiseptic properties, which help to disinfect the skin and prevent infections. The cooling effect of splash products is favored by many consumers, especially those who prefer a brisk and revitalizing post-shave feel. However, due to their alcohol content, splash products may not be suitable for individuals with sensitive or dry skin, as they can cause irritation or dryness. The choice between lotions, balms, and splashes often depends on personal preference, skin type, and the desired post-shave effect. In recent years, there has been a growing trend towards natural and organic aftershave products, as consumers become more conscious of the ingredients used in their skincare routines. This has led to the development of lotions and balms that are free from synthetic fragrances, parabens, and sulfates, catering to the demand for clean and sustainable grooming products. Additionally, the rise of e-commerce has made it easier for consumers to access a wide variety of aftershave products from around the world, allowing them to explore different formulations and brands. The global aftershave lotions and creams market continues to evolve, with manufacturers focusing on innovation and product differentiation to meet the diverse needs of consumers. As the market expands, there is a growing emphasis on creating products that not only provide effective post-shave care but also align with the values and preferences of modern consumers.

Online, Offline in the Global Aftershave Lotions & Creams Market:

The usage of global aftershave lotions and creams can be broadly categorized into online and offline channels, each offering unique advantages and challenges. Online platforms have revolutionized the way consumers purchase aftershave products, providing convenience and accessibility. With the rise of e-commerce, consumers can easily browse and compare a wide range of aftershave lotions and creams from the comfort of their homes. Online platforms offer detailed product descriptions, customer reviews, and ratings, helping consumers make informed purchasing decisions. Additionally, online shopping provides access to a global marketplace, allowing consumers to explore international brands and unique formulations that may not be available in local stores. The convenience of doorstep delivery and the ability to shop at any time further enhance the appeal of online channels. However, the online market also presents challenges, such as the inability to physically test or smell the products before purchase, which can be a significant factor for consumers when choosing aftershave products. On the other hand, offline channels, including supermarkets, drugstores, and specialty grooming stores, offer a tactile shopping experience. Consumers can physically examine the products, test samples, and seek advice from sales representatives, which can be particularly beneficial for those who are new to aftershave products or have specific skincare concerns. Offline shopping allows consumers to make immediate purchases without waiting for delivery, which can be advantageous for those who need products urgently. Additionally, offline channels often provide promotional offers and discounts, attracting price-sensitive consumers. However, the offline market is limited by geographical constraints, as consumers can only access products available in their local area. Despite the challenges, both online and offline channels play a crucial role in the distribution and consumption of aftershave lotions and creams. Manufacturers and retailers are increasingly adopting an omnichannel approach, integrating online and offline strategies to provide a seamless shopping experience for consumers. This includes offering click-and-collect services, where consumers can order products online and pick them up in-store, as well as leveraging social media and digital marketing to drive traffic to physical stores. As consumer preferences continue to evolve, the global aftershave lotions and creams market is likely to see further integration of online and offline channels, ensuring that consumers have access to a diverse range of products and shopping experiences.

Global Aftershave Lotions & Creams Market Outlook:

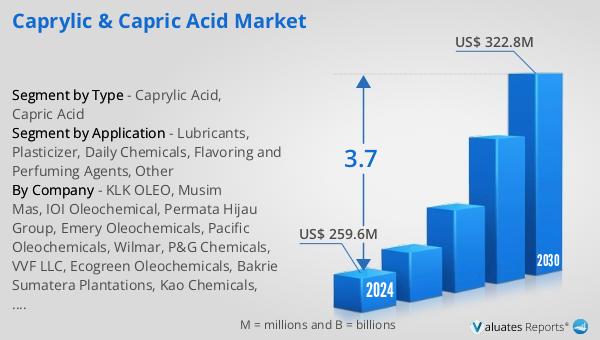

The global aftershave lotions and creams market is anticipated to experience growth over the coming years. Starting from a valuation of approximately $1,465.4 million in 2024, the market is expected to reach around $1,719.4 million by 2030. This growth trajectory reflects a compound annual growth rate (CAGR) of 2.7% throughout the forecast period. This steady increase can be attributed to several factors, including the rising awareness of personal grooming among men and the expanding male grooming industry. As more men become conscious of their appearance and skincare, the demand for aftershave products is likely to rise. Additionally, the influence of social media and celebrity endorsements has played a significant role in shaping grooming trends, further driving market growth. The market's expansion is also supported by the introduction of innovative products that cater to diverse consumer preferences, such as natural and organic formulations. As manufacturers continue to focus on product differentiation and innovation, the global aftershave lotions and creams market is poised for sustained growth, meeting the evolving needs of consumers worldwide.

| Report Metric | Details |

| Report Name | Aftershave Lotions & Creams Market |

| Accounted market size in 2024 | US$ 1465.4 million |

| Forecasted market size in 2030 | US$ 1719.4 million |

| CAGR | 2.7 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Procter and Gamble, Unilever, Beiersdorf, Godrej Consumer Products Limited, L’Oréal, Colgate-Palmolive Company, Coty Inc., D.R. Harris & Co Ltd., Vi-john Group, Herbacin Cosmetic GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |