What is Ultra-High Purity Metal Sputtering Targets - Global Market?

Ultra-high purity metal sputtering targets are essential components in the manufacturing processes of various high-tech industries. These targets are made from metals that have been refined to an extremely high level of purity, often exceeding 99.99%. This high purity is crucial because it ensures that the thin films deposited during the sputtering process are free from impurities that could affect the performance of the final product. The global market for these sputtering targets is driven by the increasing demand for advanced electronic devices, solar panels, and other high-tech applications. As technology continues to advance, the need for materials that can deliver superior performance and reliability becomes more critical. This demand is reflected in the growing market for ultra-high purity metal sputtering targets, which are used in the production of semiconductors, flat panel displays, and other electronic components. The market is characterized by a high level of competition, with numerous manufacturers striving to produce targets that meet the stringent quality standards required by their customers.

Aluminum Sputtering Target, Titanium Sputtering Target, Copper Sputtering Target, Tantalum Sputtering Target, Tungsten Sputtering Target, Molybdenum Sputtering Target, Others in the Ultra-High Purity Metal Sputtering Targets - Global Market:

Aluminum sputtering targets are widely used in the electronics industry due to their excellent conductivity and corrosion resistance. These targets are essential in the production of thin films for semiconductors and flat panel displays. The demand for aluminum sputtering targets is driven by the increasing production of electronic devices and the need for efficient and reliable materials. Titanium sputtering targets, on the other hand, are known for their high strength and resistance to corrosion. They are commonly used in the aerospace and medical industries, where durability and reliability are paramount. The use of titanium sputtering targets in the production of medical implants and aerospace components is a testament to their versatility and performance. Copper sputtering targets are highly valued for their excellent electrical conductivity and thermal properties. They are widely used in the production of printed circuit boards and other electronic components. The demand for copper sputtering targets is closely linked to the growth of the electronics industry and the increasing need for high-performance materials. Tantalum sputtering targets are known for their high melting point and excellent corrosion resistance. They are used in the production of capacitors and other electronic components that require materials that can withstand extreme conditions. The demand for tantalum sputtering targets is driven by the need for reliable and durable materials in the electronics industry. Tungsten sputtering targets are valued for their high density and melting point. They are used in the production of X-ray tubes and other high-temperature applications. The demand for tungsten sputtering targets is driven by the need for materials that can withstand extreme temperatures and provide reliable performance. Molybdenum sputtering targets are known for their excellent thermal and electrical conductivity. They are used in the production of thin films for solar panels and other electronic components. The demand for molybdenum sputtering targets is closely linked to the growth of the solar energy industry and the increasing need for efficient and reliable materials. Other sputtering targets, such as those made from nickel, cobalt, and other metals, are also used in various high-tech applications. The demand for these targets is driven by the need for materials that can deliver superior performance and reliability in a wide range of applications.

Semiconductor, Solar Photovoltaic, Others in the Ultra-High Purity Metal Sputtering Targets - Global Market:

Ultra-high purity metal sputtering targets play a crucial role in the semiconductor industry, where they are used to deposit thin films on silicon wafers. These thin films are essential for the production of integrated circuits and other semiconductor devices. The demand for ultra-high purity metal sputtering targets in the semiconductor industry is driven by the increasing complexity of electronic devices and the need for materials that can deliver superior performance and reliability. In the solar photovoltaic industry, ultra-high purity metal sputtering targets are used to deposit thin films on solar cells. These thin films are essential for improving the efficiency and performance of solar panels. The demand for ultra-high purity metal sputtering targets in the solar photovoltaic industry is driven by the increasing adoption of solar energy and the need for materials that can deliver superior performance and reliability. In addition to the semiconductor and solar photovoltaic industries, ultra-high purity metal sputtering targets are also used in a wide range of other applications. These include the production of flat panel displays, optical coatings, and other high-tech products. The demand for ultra-high purity metal sputtering targets in these applications is driven by the need for materials that can deliver superior performance and reliability in a wide range of applications. As technology continues to advance, the demand for ultra-high purity metal sputtering targets is expected to grow, driven by the increasing need for materials that can deliver superior performance and reliability in a wide range of applications.

Ultra-High Purity Metal Sputtering Targets - Global Market Outlook:

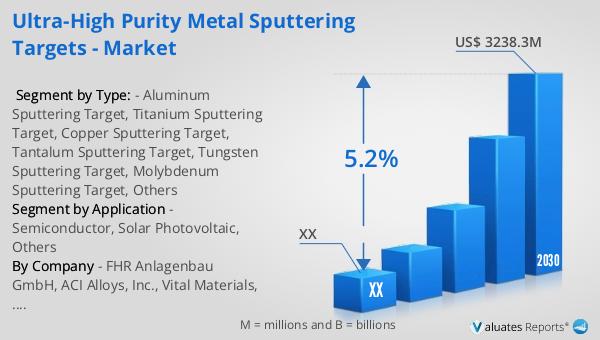

The global market for ultra-high purity metal sputtering targets was valued at approximately $2,248 million in 2023. It is projected to grow to a revised size of around $3,238.3 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.2% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for high-purity materials in various high-tech industries, including electronics, solar energy, and others. The North American market for these sputtering targets was also valued at a significant amount in 2023, with expectations of reaching a higher value by 2030, although specific figures are not provided. The growth in this region is expected to align with the global trend, driven by advancements in technology and the increasing need for reliable and efficient materials. The market outlook suggests a positive trajectory for ultra-high purity metal sputtering targets, underscoring their importance in the production of advanced electronic devices and other high-tech applications. As industries continue to evolve and demand more sophisticated materials, the market for these sputtering targets is poised for significant growth.

| Report Metric | Details |

| Report Name | Ultra-High Purity Metal Sputtering Targets - Market |

| Forecasted market size in 2030 | US$ 3238.3 million |

| CAGR | 5.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | FHR Anlagenbau GmbH, ACI Alloys, Inc., Vital Materials, Matsurf Technologies Inc, Plasmaterials, Inc., Creative Semiconductor Engineering, Sputtering Target and Evaporation Material, American Elements, AEM, CHINA RARE METAL MATERLAL CO.,LTD., Changsha Xinkang Advanced Materials Co.,Ltd, JX Nippon Mining & Metals Corporation, Plansee SE, Praxair, Honeywell, ULVAC, Hitachi Metals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |