What is Zinc Selenide Raw Material - Global Market?

Zinc Selenide (ZnSe) is a chemical compound that plays a crucial role in various industries due to its unique properties. It is primarily used as a raw material in the global market for applications that require high optical transparency and thermal resistance. ZnSe is a yellowish, crystalline solid that is known for its ability to transmit infrared light, making it an essential component in optical devices. The global market for Zinc Selenide raw material is driven by its demand in sectors such as electronics, semiconductors, medical fields, and thermal imaging systems. Its ability to withstand high temperatures and its non-reactive nature make it suitable for use in harsh environments. The market is characterized by a steady demand due to its applications in cutting-edge technologies and industries that require precision and reliability. As industries continue to innovate and develop new technologies, the demand for Zinc Selenide is expected to grow, further solidifying its position as a vital raw material in the global market. The versatility and efficiency of ZnSe in various applications underscore its importance and ensure its continued relevance in the market.

<50mm, 50-150mm, 150-250mm, Above 250mm in the Zinc Selenide Raw Material - Global Market:

Zinc Selenide raw material is available in various sizes, each catering to specific applications and industries. The size categories include <50mm, 50-150mm, 150-250mm, and above 250mm, each offering distinct advantages and uses. The <50mm size is typically used in applications where precision and compactness are crucial. This size is ideal for small-scale optical devices and components that require high accuracy and minimal space. The 50-150mm size range is more versatile, often used in medium-sized optical systems and devices. It provides a balance between size and performance, making it suitable for a wide range of applications, including some medical devices and imaging systems. The 150-250mm size is generally used in larger systems where more substantial components are necessary. This size is often found in industrial applications and larger optical systems that require robust and durable materials. Finally, the above 250mm size category is used in specialized applications that demand large-scale components. These are typically found in industrial and research settings where the size and durability of the material are critical. Each size category of Zinc Selenide raw material offers unique benefits, allowing it to be tailored to specific needs and applications across various industries. The availability of different sizes ensures that Zinc Selenide can meet the diverse requirements of its users, from small-scale precision devices to large industrial systems. This adaptability is one of the key factors driving the demand for Zinc Selenide in the global market. As technology continues to advance, the need for materials that can be customized to specific applications will only increase, further highlighting the importance of Zinc Selenide in the market. The ability to choose from a range of sizes allows manufacturers and developers to optimize their products and systems, ensuring that they meet the highest standards of performance and reliability. This flexibility is crucial in industries where precision and efficiency are paramount, and Zinc Selenide's ability to deliver on these fronts makes it an indispensable material in the global market.

Electronics and Semiconductors, Medical Field, Thermal Imaging System, Others in the Zinc Selenide Raw Material - Global Market:

Zinc Selenide raw material is widely used in various fields due to its exceptional properties, particularly in electronics and semiconductors, the medical field, thermal imaging systems, and other applications. In the electronics and semiconductor industry, ZnSe is valued for its optical properties and thermal stability. It is used in the production of laser diodes, optical windows, and lenses, where its ability to transmit infrared light is crucial. The material's high resistance to thermal shock and its non-reactive nature make it ideal for use in environments where precision and reliability are essential. In the medical field, Zinc Selenide is used in imaging systems and diagnostic equipment. Its ability to provide clear and accurate imaging makes it a valuable component in medical devices that require high precision and reliability. The material's non-toxic nature also makes it suitable for use in medical applications where safety is a priority. In thermal imaging systems, ZnSe is used for its ability to transmit infrared light, which is essential for capturing thermal images. This makes it a critical component in systems used for surveillance, security, and industrial inspections. The material's durability and resistance to harsh environments make it ideal for use in these demanding applications. Beyond these specific fields, Zinc Selenide is also used in other applications that require high optical clarity and thermal resistance. Its versatility and efficiency make it a popular choice for a wide range of industries, from aerospace to telecommunications. The material's ability to meet the diverse needs of these industries underscores its importance in the global market. As technology continues to evolve, the demand for materials like Zinc Selenide that can deliver high performance and reliability will only increase, further solidifying its position as a key raw material in the global market.

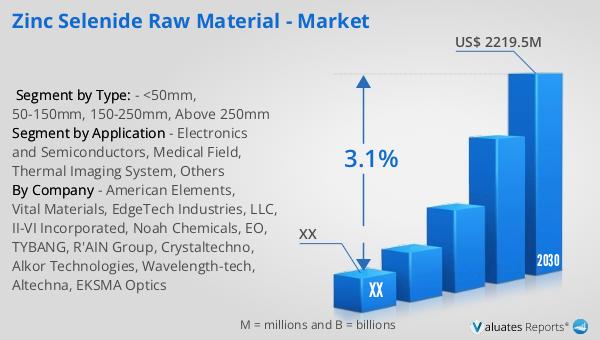

Zinc Selenide Raw Material - Global Market Outlook:

The global market for Zinc Selenide raw material was valued at approximately $1,798 million in 2023. Looking ahead, it is projected to grow to a revised size of about $2,219.5 million by the year 2030. This growth represents a compound annual growth rate (CAGR) of 3.1% over the forecast period from 2024 to 2030. This steady growth rate indicates a consistent demand for Zinc Selenide across various industries, driven by its unique properties and wide range of applications. The market's expansion is likely fueled by the increasing need for advanced materials in sectors such as electronics, semiconductors, and medical devices, where precision and reliability are paramount. As industries continue to innovate and develop new technologies, the demand for materials like Zinc Selenide that can meet these evolving needs is expected to rise. This growth trajectory highlights the importance of Zinc Selenide as a critical raw material in the global market, with its ability to deliver high performance and adaptability to various applications ensuring its continued relevance and demand. The projected increase in market size reflects the ongoing advancements in technology and the growing need for materials that can support these innovations, making Zinc Selenide an indispensable component in the global market landscape.

| Report Metric | Details |

| Report Name | Zinc Selenide Raw Material - Market |

| Forecasted market size in 2030 | US$ 2219.5 million |

| CAGR | 3.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | American Elements, Vital Materials, EdgeTech Industries, LLC, II-VI Incorporated, Noah Chemicals, EO, TYBANG, R'AIN Group, Crystaltechno, Alkor Technologies, Wavelength-tech, Altechna, EKSMA Optics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |