What is Mobile Medical Clinic - Global Market?

Mobile medical clinics represent a transformative approach in the healthcare industry, offering a flexible and accessible solution to deliver medical services directly to communities. These clinics are essentially healthcare facilities on wheels, equipped with necessary medical equipment and staffed by healthcare professionals. They are designed to reach underserved populations, rural areas, and regions where traditional healthcare facilities are scarce or non-existent. The global market for mobile medical clinics is expanding rapidly, driven by the increasing demand for accessible healthcare services, technological advancements, and the need for cost-effective healthcare solutions. These clinics provide a wide range of services, including primary care, preventive screenings, vaccinations, and chronic disease management. They play a crucial role in disaster response, providing immediate medical care in emergencies. The market is also influenced by government initiatives and funding aimed at improving healthcare access and reducing healthcare disparities. As healthcare systems worldwide strive to become more inclusive and efficient, mobile medical clinics are poised to become an integral part of the healthcare delivery model, bridging the gap between healthcare providers and patients. Their ability to adapt to various healthcare needs makes them a vital component in the global healthcare landscape.

Mobile Health Clinic, Mobile Crisis Clinic, Mobile Dental Clinic, Others in the Mobile Medical Clinic - Global Market:

Mobile health clinics are a subset of mobile medical clinics that focus on delivering a broad spectrum of healthcare services directly to patients in their communities. These clinics are equipped with the necessary medical tools and staffed by healthcare professionals who provide services such as health screenings, vaccinations, and chronic disease management. They are particularly beneficial in reaching underserved populations, including those in rural or remote areas where access to traditional healthcare facilities is limited. Mobile health clinics play a critical role in preventive care, helping to identify health issues early and reduce the need for more intensive medical interventions. On the other hand, mobile crisis clinics are specialized units designed to provide immediate mental health support and crisis intervention. These clinics are crucial in addressing mental health emergencies, offering on-the-spot counseling, and connecting individuals with ongoing mental health services. They are often deployed in response to community crises, such as natural disasters or incidents of violence, providing essential support to those affected. Mobile dental clinics focus on delivering dental care services, including routine check-ups, cleanings, and minor dental procedures. They are instrumental in promoting oral health, particularly in areas where dental services are not readily available. These clinics help in reducing the prevalence of dental diseases and improving overall health outcomes. Other types of mobile medical clinics include those that offer specialized services such as ophthalmology, dermatology, or pediatrics. These clinics cater to specific healthcare needs, ensuring that specialized care is accessible to all. The global market for mobile medical clinics is diverse, with each type of clinic addressing unique healthcare challenges and contributing to the overall goal of improving healthcare access and quality. As the demand for mobile healthcare solutions continues to grow, these clinics are expected to play an increasingly important role in the global healthcare system.

Hospital, Clinic, Government, Others in the Mobile Medical Clinic - Global Market:

Mobile medical clinics are utilized in various settings, including hospitals, clinics, government programs, and other areas, to enhance healthcare delivery and accessibility. In hospitals, mobile medical clinics serve as an extension of the hospital's services, allowing healthcare providers to reach patients who may not be able to visit the hospital due to distance, mobility issues, or other barriers. These clinics can provide follow-up care, chronic disease management, and preventive services, reducing the burden on hospital facilities and improving patient outcomes. In clinics, mobile medical units offer a flexible solution to expand services beyond the physical location of the clinic. They enable clinics to reach a broader patient base, particularly in rural or underserved areas, and provide essential healthcare services such as vaccinations, screenings, and health education. This approach helps clinics to increase their reach and impact, ensuring that more individuals have access to necessary healthcare services. Government programs often utilize mobile medical clinics as part of public health initiatives aimed at improving healthcare access and reducing disparities. These clinics are deployed in areas with limited healthcare infrastructure, providing essential services such as immunizations, maternal and child health care, and health education. They play a crucial role in public health campaigns, such as vaccination drives or health screenings, ensuring that these services reach the most vulnerable populations. Other areas where mobile medical clinics are used include corporate wellness programs, community health events, and disaster response efforts. In corporate settings, mobile clinics provide on-site health services to employees, promoting wellness and reducing absenteeism. During community health events, these clinics offer free or low-cost health services, increasing awareness and encouraging preventive care. In disaster response, mobile medical clinics are deployed to provide immediate medical care to affected populations, offering a lifeline in times of crisis. Overall, the use of mobile medical clinics in these various settings highlights their versatility and importance in enhancing healthcare delivery and accessibility.

Mobile Medical Clinic - Global Market Outlook:

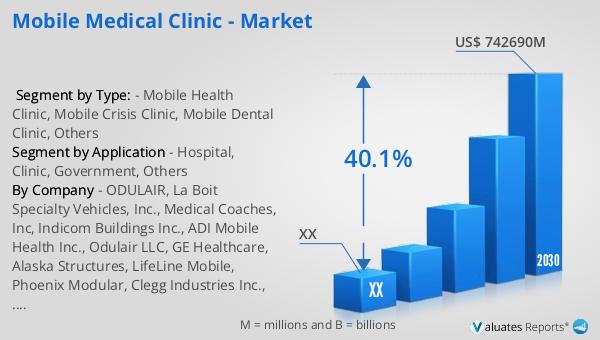

The global market for mobile medical clinics was valued at approximately US$ 9,425 million in 2023. It is projected to grow significantly, reaching an adjusted size of US$ 742,690 million by 2030, with a compound annual growth rate (CAGR) of 40.1% during the forecast period from 2024 to 2030. This remarkable growth is indicative of the increasing demand for mobile healthcare solutions worldwide. The expansion of this market is driven by several factors, including the need for accessible healthcare services, technological advancements, and government initiatives aimed at improving healthcare access. In comparison, the global market for medical devices was estimated at US$ 603 billion in 2023, with a projected CAGR of 5% over the next six years. This highlights the rapid growth of the mobile medical clinic market, which is outpacing the broader medical device market. The increasing adoption of mobile medical clinics is a testament to their effectiveness in addressing healthcare challenges and improving access to care. As healthcare systems continue to evolve, mobile medical clinics are expected to play a crucial role in shaping the future of healthcare delivery, providing flexible and cost-effective solutions to meet the diverse needs of patients worldwide.

| Report Metric | Details |

| Report Name | Mobile Medical Clinic - Market |

| Forecasted market size in 2030 | US$ 742690 million |

| CAGR | 40.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ODULAIR, La Boit Specialty Vehicles, Inc., Medical Coaches, Inc, Indicom Buildings Inc., ADI Mobile Health Inc., Odulair LLC, GE Healthcare, Alaska Structures, LifeLine Mobile, Phoenix Modular, Clegg Industries Inc., Summit Bodyworks, Mission Mobile Medical, Craftsmen Industries, Matthews Specialty Vehicles |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |