What is Boost Charge Pump ICs - Global Market?

Boost Charge Pump ICs are integral components in the electronics industry, playing a crucial role in power management by converting and regulating voltage levels. These integrated circuits (ICs) are designed to increase the voltage from a lower level to a higher one, which is essential for powering various electronic devices efficiently. The global market for Boost Charge Pump ICs is expanding due to the growing demand for portable and battery-operated devices. As technology advances, the need for efficient power management solutions becomes more critical, driving the adoption of these ICs across different sectors. The market is characterized by continuous innovation, with manufacturers focusing on developing ICs that offer higher efficiency, smaller size, and lower power consumption. This growth is further fueled by the increasing penetration of consumer electronics, industrial automation, and the automotive sector, which require reliable and efficient power solutions. As a result, the Boost Charge Pump ICs market is poised for significant growth, driven by technological advancements and the rising demand for energy-efficient electronic devices.

Switching Regulator Booster Pump ICs, Capacitive Non-Adjustable Charge Pump ICs, Capacitive Adjustable Charge Pump ICs in the Boost Charge Pump ICs - Global Market:

Switching Regulator Booster Pump ICs, Capacitive Non-Adjustable Charge Pump ICs, and Capacitive Adjustable Charge Pump ICs are three distinct types of Boost Charge Pump ICs, each serving specific functions within the global market. Switching Regulator Booster Pump ICs are designed to efficiently convert and regulate voltage levels in electronic devices. They use a switching mechanism to control the flow of electrical energy, making them highly efficient and suitable for applications requiring precise voltage regulation. These ICs are commonly used in portable devices, where battery life and power efficiency are critical. On the other hand, Capacitive Non-Adjustable Charge Pump ICs operate by transferring charge between capacitors to boost voltage levels. These ICs are simpler in design and are often used in applications where fixed voltage levels are sufficient. They are ideal for low-power applications, offering a cost-effective solution for boosting voltage without the need for complex control mechanisms. Capacitive Adjustable Charge Pump ICs, however, provide more flexibility by allowing users to adjust the output voltage levels according to specific requirements. This adaptability makes them suitable for a wide range of applications, from consumer electronics to industrial equipment, where varying voltage levels are needed. The global market for these ICs is driven by the increasing demand for efficient power management solutions across various industries. As electronic devices become more sophisticated, the need for reliable and adaptable power solutions grows, leading to the development and adoption of these advanced ICs. Manufacturers are continuously innovating to improve the performance and efficiency of these ICs, focusing on reducing size, increasing power density, and enhancing thermal management. This innovation is crucial in meeting the evolving needs of the market, particularly in sectors such as telecommunications, automotive, and consumer electronics, where power efficiency and reliability are paramount. The market for Switching Regulator Booster Pump ICs, Capacitive Non-Adjustable Charge Pump ICs, and Capacitive Adjustable Charge Pump ICs is expected to grow significantly, driven by technological advancements and the increasing demand for energy-efficient solutions. As industries continue to adopt more advanced electronic systems, the need for efficient power management solutions will only increase, further propelling the growth of this market.

Mobile and Consumer Electronics, Industrial, Computer, Automobile and Rail Transit, Telecommunications and Infrastructure, Medical in the Boost Charge Pump ICs - Global Market:

Boost Charge Pump ICs find extensive usage across various sectors, including Mobile and Consumer Electronics, Industrial, Computer, Automobile and Rail Transit, Telecommunications and Infrastructure, and Medical. In the Mobile and Consumer Electronics sector, these ICs are crucial for managing power in devices such as smartphones, tablets, and wearable gadgets. They help in extending battery life and ensuring efficient power usage, which is vital for portable devices. In the Industrial sector, Boost Charge Pump ICs are used in automation systems and machinery, where they provide stable and reliable power management solutions. These ICs help in optimizing energy consumption, reducing operational costs, and enhancing the performance of industrial equipment. In the Computer sector, they are used in laptops, desktops, and servers to manage power distribution and ensure efficient operation. The Automobile and Rail Transit sector also benefits from these ICs, as they are used in electric vehicles and rail systems to manage power efficiently, contributing to the overall performance and reliability of these transportation modes. In Telecommunications and Infrastructure, Boost Charge Pump ICs are used to ensure stable power supply in communication networks and data centers, which is essential for maintaining uninterrupted services. Lastly, in the Medical sector, these ICs are used in medical devices and equipment, where reliable power management is crucial for accurate diagnostics and patient care. The versatility and efficiency of Boost Charge Pump ICs make them indispensable across these sectors, driving their demand in the global market.

Boost Charge Pump ICs - Global Market Outlook:

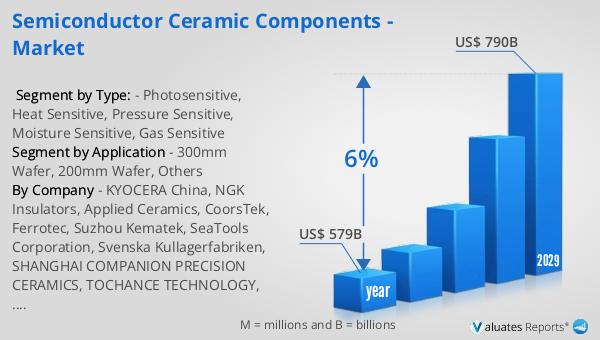

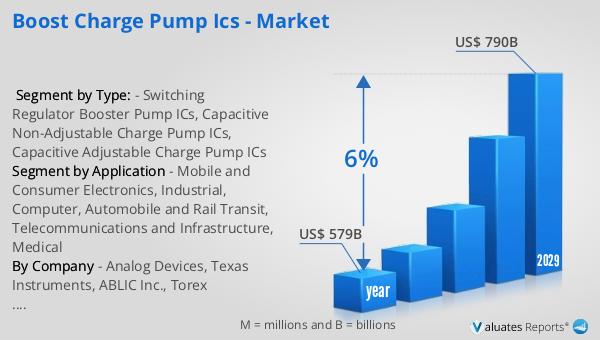

The semiconductor market, which includes Boost Charge Pump ICs, was valued at approximately $579 billion in 2022. This market is projected to grow significantly, reaching around $790 billion by 2029, with a compound annual growth rate (CAGR) of 6% during the forecast period. This growth is indicative of the increasing demand for semiconductors across various industries, driven by technological advancements and the rising need for efficient power management solutions. The expansion of the semiconductor market is fueled by the proliferation of electronic devices, the growth of the Internet of Things (IoT), and the increasing adoption of automation and smart technologies. As industries continue to evolve and integrate more advanced electronic systems, the demand for semiconductors, including Boost Charge Pump ICs, is expected to rise. This growth presents significant opportunities for manufacturers and stakeholders in the semiconductor industry, as they strive to meet the increasing demand for innovative and efficient solutions. The projected growth of the semiconductor market underscores the importance of continuous innovation and development in this field, as companies seek to capitalize on the expanding opportunities and address the evolving needs of various sectors.

| Report Metric | Details |

| Report Name | Boost Charge Pump ICs - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Analog Devices, Texas Instruments, ABLIC Inc., Torex Semiconductor Ltd., Boost Charge Pump ICAutomotive Magnetic Sensor ICEATX MotherboardShanghai Awinic Technology Co., Ltd., Southchip Semiconductor Technology Co., Ltd., Silergy Corp., Halo Microelectronics Co.,Ltd., Wuxi Hexin Semiconductor Co., Ltd., Meraki Integrated Shenzhen Technology Co., Ltd., SG Micro Corp., Shanghai Belling Corp.,Ltd., Shanghai Ctepower Technology Co.,Limited ETA., Shenzhen Boya Yingda Technology Co., Ltd., Shenzhen Yucan Electrical Co., Ltd., Nanjing Micro One Electronics Inc., JoulWatt Technology Co., Ltd., Microchip Technology Inc., Wuxi Chipown Micro-electronics Limited, Monolithic Power Systems, Inc., Qualcomm Inc., MediaTek Inc., Shanghai Bright Power Semiconductor Co.,Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |