What is Starch Hydrolysis Crystalline Fructose - Global Market?

Starch Hydrolysis Crystalline Fructose is a specialized product derived from the breakdown of starch into simpler sugars, primarily fructose. This process involves the enzymatic conversion of starch, a complex carbohydrate, into crystalline fructose, which is a highly pure form of sugar. The global market for this product is driven by its increasing demand across various industries due to its unique properties. Crystalline fructose is sweeter than regular sugar, which means less is needed to achieve the same level of sweetness, making it an attractive option for manufacturers looking to reduce sugar content in their products. Additionally, it has a low glycemic index, making it a preferred choice for health-conscious consumers and those managing blood sugar levels. The market is witnessing growth due to the rising awareness of health and wellness trends, as well as the increasing demand for low-calorie and sugar-reduced products. As a result, the starch hydrolysis crystalline fructose market is expanding, with significant opportunities for innovation and development in various applications.

Fine Granular, Standard Granular in the Starch Hydrolysis Crystalline Fructose - Global Market:

In the global market for starch hydrolysis crystalline fructose, two primary forms are prevalent: fine granular and standard granular. Fine granular crystalline fructose is characterized by its small particle size, which allows for quick dissolution and even distribution in various applications. This form is particularly favored in the food and beverage industry, where it is used to enhance the sweetness of products without altering their texture. Its fine consistency makes it ideal for use in powdered drink mixes, baked goods, and confectionery items, where a smooth and uniform texture is desired. On the other hand, standard granular crystalline fructose has a slightly larger particle size, which can provide a different texture and mouthfeel in finished products. This form is often used in applications where a more substantial sugar presence is needed, such as in certain types of candies and desserts. Both forms of crystalline fructose offer manufacturers the ability to reduce the overall sugar content in their products while maintaining the desired level of sweetness. This is particularly important in today's market, where consumers are increasingly seeking healthier alternatives to traditional sugar-laden products. The choice between fine granular and standard granular crystalline fructose often depends on the specific requirements of the product being developed, as well as the desired sensory attributes. In addition to their use in food and beverage applications, both forms of crystalline fructose are also utilized in the pharmaceutical and cosmetics industries. In pharmaceuticals, crystalline fructose is used as a sweetening agent in syrups and chewable tablets, providing a pleasant taste without the need for artificial sweeteners. Its low glycemic index also makes it suitable for use in products aimed at diabetic patients. In the cosmetics industry, crystalline fructose is used in formulations where a natural sweetener is preferred, such as in lip balms and flavored skincare products. The versatility of crystalline fructose, in both fine and standard granular forms, makes it a valuable ingredient across multiple sectors. As the demand for healthier and more natural products continues to grow, the market for starch hydrolysis crystalline fructose is expected to expand, offering new opportunities for innovation and development. Manufacturers are increasingly exploring ways to incorporate this ingredient into their products, driven by consumer preferences for reduced sugar content and natural sweeteners. The global market for starch hydrolysis crystalline fructose is poised for growth, with both fine granular and standard granular forms playing a crucial role in meeting the diverse needs of various industries.

Food, Beverage, Pharmaceutical, Cosmetics, Others in the Starch Hydrolysis Crystalline Fructose - Global Market:

Starch hydrolysis crystalline fructose finds extensive usage across several industries, including food, beverage, pharmaceutical, cosmetics, and others, due to its unique properties and benefits. In the food industry, crystalline fructose is used as a sweetener in a wide range of products, from baked goods to dairy items. Its high sweetness level allows manufacturers to use less of it compared to regular sugar, helping to reduce the overall calorie content of the product. This is particularly appealing in the current market, where there is a strong demand for healthier food options. Additionally, crystalline fructose's ability to enhance flavors makes it a popular choice in the production of jams, jellies, and sauces. In the beverage industry, crystalline fructose is used to sweeten soft drinks, energy drinks, and flavored waters. Its high solubility ensures that it dissolves quickly and evenly, providing a consistent sweetness throughout the beverage. This is especially important in the production of low-calorie and sugar-free drinks, where maintaining the desired taste profile is crucial. The low glycemic index of crystalline fructose also makes it an attractive option for beverages targeted at health-conscious consumers and those managing their blood sugar levels. In the pharmaceutical industry, crystalline fructose is used as a sweetening agent in various formulations, including syrups, chewable tablets, and lozenges. Its pleasant taste and low glycemic index make it suitable for use in products aimed at diabetic patients and those seeking to reduce their sugar intake. Additionally, crystalline fructose's ability to mask the bitter taste of certain active ingredients makes it a valuable component in the formulation of palatable medications. In the cosmetics industry, crystalline fructose is used in products where a natural sweetener is preferred, such as in lip balms, flavored skincare products, and oral care items. Its ability to provide a pleasant taste without the need for artificial sweeteners aligns with the growing consumer preference for natural and organic products. Beyond these industries, crystalline fructose is also used in other applications, such as in the production of pet foods and animal feed, where its sweetness and palatability can enhance the appeal of the product. The versatility of starch hydrolysis crystalline fructose makes it a valuable ingredient across multiple sectors, with its usage continuing to expand as manufacturers seek to meet the evolving demands of consumers.

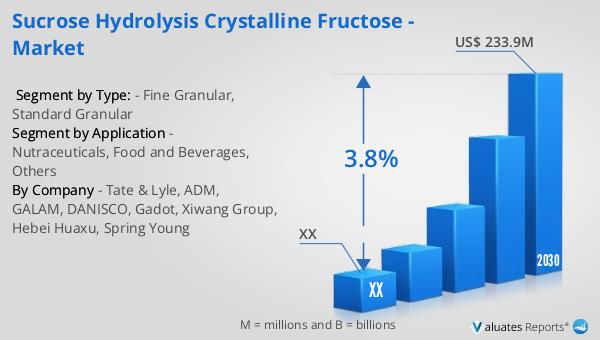

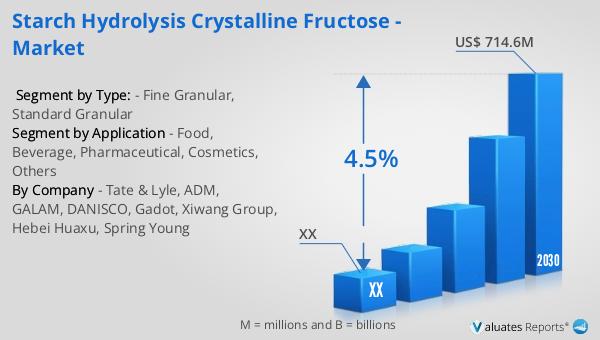

Starch Hydrolysis Crystalline Fructose - Global Market Outlook:

The global market for starch hydrolysis crystalline fructose was valued at approximately US$ 521.1 million in 2023. Looking ahead, it is projected to grow to a revised size of US$ 714.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030. This growth is largely driven by the increasing demand for healthier and more natural sweeteners across various industries. The chemical properties of crystalline fructose, such as its high sweetness level and low glycemic index, make it an attractive option for manufacturers looking to reduce sugar content in their products while maintaining the desired taste profile. As consumers become more health-conscious and seek out products with reduced sugar content, the demand for crystalline fructose is expected to rise. Additionally, the versatility of crystalline fructose in applications ranging from food and beverages to pharmaceuticals and cosmetics further contributes to its market growth. The ability to use crystalline fructose in a variety of formulations allows manufacturers to cater to diverse consumer preferences and dietary needs. As a result, the starch hydrolysis crystalline fructose market is poised for continued expansion, with significant opportunities for innovation and development in the coming years. The chemical characteristics of crystalline fructose play a crucial role in driving this growth, as they enable manufacturers to create products that align with current health and wellness trends.

| Report Metric | Details |

| Report Name | Starch Hydrolysis Crystalline Fructose - Market |

| Forecasted market size in 2030 | US$ 714.6 million |

| CAGR | 4.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Tate & Lyle, ADM, GALAM, DANISCO, Gadot, Xiwang Group, Hebei Huaxu, Spring Young |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |