What is Personal Use Defibrillator - Global Market?

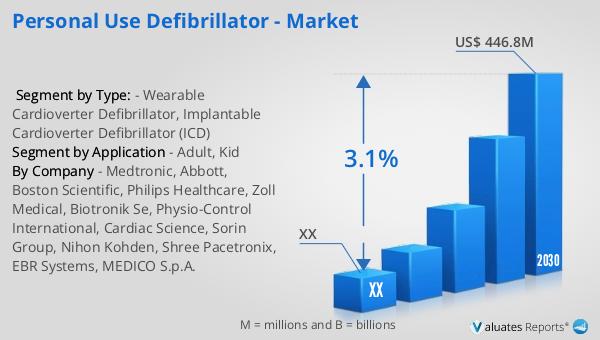

The global market for personal use defibrillators is a rapidly evolving sector within the broader medical devices industry. In 2023, this market was valued at approximately US$ 358.8 million, with projections indicating a growth to US$ 446.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.1% from 2024 to 2030. This growth is driven by increasing awareness of cardiac health, advancements in defibrillator technology, and the rising prevalence of cardiovascular diseases worldwide. Personal use defibrillators are designed for non-professional use, allowing individuals to respond quickly to cardiac emergencies, potentially saving lives. These devices are becoming more user-friendly, portable, and affordable, making them accessible to a broader audience. The market's expansion is also supported by initiatives from healthcare organizations and governments to promote heart health and emergency preparedness. As the global medical devices market, estimated at US$ 603 billion in 2023, continues to grow at a CAGR of 5% over the next six years, personal use defibrillators are expected to play a significant role in enhancing individual health management and emergency response capabilities.

Wearable Cardioverter Defibrillator, Implantable Cardioverter Defibrillator (ICD) in the Personal Use Defibrillator - Global Market:

Wearable cardioverter defibrillators (WCDs) and implantable cardioverter defibrillators (ICDs) are two critical components of the personal use defibrillator market. WCDs are non-invasive devices worn externally, typically around the chest, and are designed to monitor heart rhythms continuously. They automatically deliver a shock to restore normal heart rhythm if a life-threatening arrhythmia is detected. These devices are particularly beneficial for patients who are at temporary risk of sudden cardiac arrest but are not yet candidates for an ICD. WCDs offer a bridge to more permanent solutions, providing peace of mind and protection during critical periods. On the other hand, ICDs are surgically implanted devices that perform similar functions but are intended for long-term use. They are recommended for patients with a high risk of recurrent cardiac arrest due to conditions like heart failure or a history of heart attacks. ICDs continuously monitor heart rhythms and deliver electrical shocks or pacing to correct arrhythmias. The global market for these devices is driven by technological advancements, such as improved battery life, reduced device size, and enhanced monitoring capabilities. Additionally, increasing awareness of heart health and the importance of early intervention in cardiac emergencies contribute to market growth. Both WCDs and ICDs are integral to managing heart conditions, offering patients and healthcare providers effective tools to prevent sudden cardiac death. As the personal use defibrillator market expands, these devices are expected to become more accessible and affordable, further driving their adoption worldwide.

Adult, Kid in the Personal Use Defibrillator - Global Market:

The usage of personal use defibrillators in adults and children varies significantly due to differences in physiology, risk factors, and device design. For adults, personal use defibrillators are primarily used to address the high prevalence of cardiovascular diseases, which are a leading cause of death globally. Adults, particularly those with a history of heart disease, are at a higher risk of sudden cardiac arrest, making personal defibrillators a crucial tool for emergency response. These devices empower individuals and their families to act swiftly in the event of a cardiac emergency, potentially saving lives. The design of adult defibrillators focuses on ease of use, portability, and reliability, ensuring that even those without medical training can operate them effectively. In contrast, the use of personal defibrillators in children is less common but equally important. Pediatric defibrillators are specifically designed to accommodate the unique physiological characteristics of children, such as smaller body size and different heart rhythms. These devices are used in cases where children have congenital heart conditions or other risk factors for cardiac arrest. The market for pediatric defibrillators is smaller but growing, driven by increasing awareness of pediatric heart health and advancements in device technology. Both adult and pediatric defibrillators are essential components of comprehensive cardiac care, providing critical support in emergency situations. As the global market for personal use defibrillators continues to grow, these devices are expected to become more widely available and tailored to meet the specific needs of different age groups.

Personal Use Defibrillator - Global Market Outlook:

The global market for personal use defibrillators was valued at approximately US$ 358.8 million in 2023, with projections indicating growth to US$ 446.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.1% from 2024 to 2030. This growth is driven by increasing awareness of cardiac health, advancements in defibrillator technology, and the rising prevalence of cardiovascular diseases worldwide. Personal use defibrillators are designed for non-professional use, allowing individuals to respond quickly to cardiac emergencies, potentially saving lives. These devices are becoming more user-friendly, portable, and affordable, making them accessible to a broader audience. The market's expansion is also supported by initiatives from healthcare organizations and governments to promote heart health and emergency preparedness. As the global medical devices market, estimated at US$ 603 billion in 2023, continues to grow at a CAGR of 5% over the next six years, personal use defibrillators are expected to play a significant role in enhancing individual health management and emergency response capabilities.

| Report Metric | Details |

| Report Name | Personal Use Defibrillator - Market |

| Forecasted market size in 2030 | US$ 446.8 million |

| CAGR | 3.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Medtronic, Abbott, Boston Scientific, Philips Healthcare, Zoll Medical, Biotronik Se, Physio-Control International, Cardiac Science, Sorin Group, Nihon Kohden, Shree Pacetronix, EBR Systems, MEDICO S.p.A. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |