What is Submarine Telecommunication Cable - Global Market?

Submarine telecommunication cables are the backbone of global communication, forming an extensive network beneath the ocean's surface that connects continents and facilitates international data transfer. These cables are crucial for the internet, phone services, and data exchange, enabling seamless communication across the globe. The global market for submarine telecommunication cables is a dynamic and rapidly evolving sector, driven by the increasing demand for high-speed internet and data services. As digital transformation accelerates worldwide, the need for robust and reliable communication infrastructure becomes more critical. These cables are designed to withstand harsh underwater conditions, ensuring uninterrupted service. The market encompasses various stakeholders, including manufacturers, service providers, and technology developers, all working together to enhance the efficiency and capacity of these underwater networks. With advancements in technology, the market is witnessing innovations that improve the durability and performance of submarine cables, making them more efficient and cost-effective. As the world becomes more interconnected, the importance of submarine telecommunication cables continues to grow, making them a vital component of the global communication infrastructure.

Optical Fiber Cable, Copper Cable, Others in the Submarine Telecommunication Cable - Global Market:

Submarine telecommunication cables are primarily composed of optical fiber cables, copper cables, and other specialized materials, each serving distinct roles in the global market. Optical fiber cables are the most prevalent type used in submarine networks due to their superior data transmission capabilities. These cables use light to transmit data, allowing for high-speed and high-capacity communication over long distances. Optical fibers are made of glass or plastic and are designed to carry large amounts of data with minimal loss, making them ideal for international communication. The demand for optical fiber cables is driven by the increasing need for high-speed internet and data services, as they provide the backbone for global connectivity. Copper cables, on the other hand, are used in submarine networks for power transmission and short-distance communication. While they do not offer the same data transmission capabilities as optical fibers, copper cables are essential for powering the repeaters and other equipment necessary for maintaining the integrity of the network. These cables are robust and durable, capable of withstanding the harsh underwater environment. In addition to optical fiber and copper cables, the submarine telecommunication cable market also includes other specialized materials and technologies designed to enhance the performance and reliability of the network. These may include protective coatings, armoring, and advanced monitoring systems that ensure the cables remain operational even in challenging conditions. The integration of these materials and technologies is crucial for maintaining the efficiency and longevity of submarine networks, as they help prevent damage from environmental factors such as ocean currents, marine life, and human activities. As the demand for global connectivity continues to rise, the submarine telecommunication cable market is expected to grow, with ongoing innovations and advancements in cable technology playing a key role in shaping the future of international communication.

Shallow Sea, Deep Sea in the Submarine Telecommunication Cable - Global Market:

Submarine telecommunication cables are deployed in both shallow and deep-sea environments, each presenting unique challenges and opportunities for the global market. In shallow seas, cables are typically laid closer to the shore and are more susceptible to damage from human activities such as fishing, anchoring, and dredging. To mitigate these risks, cables in shallow waters are often buried beneath the seabed or protected with additional armoring to prevent accidental damage. The installation and maintenance of cables in shallow seas require specialized equipment and techniques to ensure their integrity and performance. Despite these challenges, shallow-sea cables play a crucial role in connecting coastal regions and facilitating regional communication networks. In contrast, deep-sea cables are laid in the open ocean, often at depths of several thousand meters. These cables are designed to withstand extreme pressure and temperature variations, as well as the corrosive effects of saltwater. The installation of deep-sea cables is a complex and costly process, requiring advanced technology and expertise to ensure their successful deployment. However, once installed, deep-sea cables provide a reliable and efficient means of connecting continents and supporting global communication networks. The usage of submarine telecommunication cables in both shallow and deep-sea environments highlights the importance of these networks in facilitating international data transfer and communication. As the demand for high-speed internet and data services continues to grow, the global market for submarine telecommunication cables is expected to expand, with ongoing advancements in technology and infrastructure playing a key role in meeting the needs of an increasingly interconnected world.

Submarine Telecommunication Cable - Global Market Outlook:

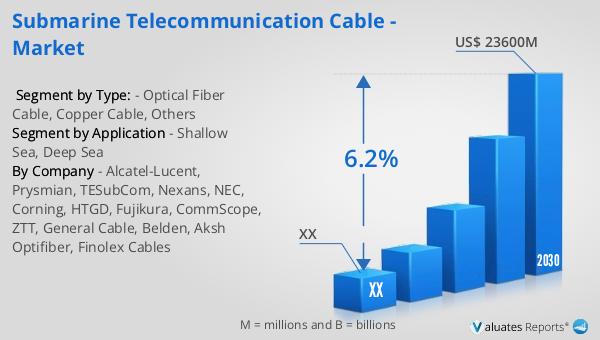

The global market for submarine telecommunication cables was valued at approximately $15.64 billion in 2023, with projections indicating a growth to around $23.6 billion by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 6.2% from 2024 to 2030. The expansion of this market is driven by the increasing demand for reliable and high-speed communication infrastructure, as highlighted in the Global Mobile Economy Development Report 2023 by GSMA Intelligence. The report noted that by the end of 2022, the number of global mobile users had surpassed 5.4 billion, underscoring the growing need for robust telecommunication networks. Additionally, data from China's Ministry of Industry and Information Technology revealed that the cumulative revenue of telecommunications services in 2022 reached 1.58 trillion, marking an 8% increase from the previous year. This growth reflects the rising demand for advanced communication solutions and the critical role of submarine telecommunication cables in supporting global connectivity. As the market continues to evolve, stakeholders are focusing on enhancing the efficiency and capacity of these underwater networks to meet the needs of an increasingly digital world.

| Report Metric | Details |

| Report Name | Submarine Telecommunication Cable - Market |

| Forecasted market size in 2030 | US$ 23600 million |

| CAGR | 6.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Alcatel-Lucent, Prysmian, TESubCom, Nexans, NEC, Corning, HTGD, Fujikura, CommScope, ZTT, General Cable, Belden, Aksh Optifiber, Finolex Cables |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |