What is Pharmaceutical Grade Ergothioneine - Global Market?

Pharmaceutical Grade Ergothioneine is a naturally occurring amino acid derivative that has garnered significant attention in the global market due to its potent antioxidant properties. This compound is primarily found in mushrooms, certain bacteria, and some animal tissues. Its unique ability to protect cells from oxidative stress makes it a valuable ingredient in various health and wellness products. The global market for Pharmaceutical Grade Ergothioneine is expanding as more industries recognize its potential benefits. It is used in dietary supplements, skincare products, and even in the food and beverage industry as a preservative. The demand is driven by increasing consumer awareness about health and wellness, coupled with a growing interest in natural and effective antioxidants. As research continues to uncover more about its benefits, the market is expected to grow, with more companies investing in its development and application. The versatility and effectiveness of Pharmaceutical Grade Ergothioneine make it a promising component in the global health and wellness industry.

Chemical Synthesis Method, Extraction Method, Biofermentation Synthesis Method in the Pharmaceutical Grade Ergothioneine - Global Market:

The production of Pharmaceutical Grade Ergothioneine involves several methods, each with its own advantages and challenges. The Chemical Synthesis Method is one of the traditional approaches, where ergothioneine is synthesized through a series of chemical reactions. This method allows for the production of ergothioneine in a controlled environment, ensuring high purity and consistency. However, it can be costly and may involve the use of hazardous chemicals, which require careful handling and disposal. On the other hand, the Extraction Method involves isolating ergothioneine from natural sources, such as mushrooms or certain bacteria. This method is often considered more sustainable and environmentally friendly, as it utilizes renewable resources. However, the yield can be variable, and the process may require extensive purification steps to achieve pharmaceutical-grade quality. Lastly, the Biofermentation Synthesis Method is a more recent development that uses genetically modified microorganisms to produce ergothioneine. This method combines the benefits of both chemical synthesis and extraction, offering high yields and purity while minimizing environmental impact. It involves the fermentation of microorganisms in a controlled environment, where they are engineered to produce ergothioneine as a byproduct. This method is gaining popularity due to its efficiency and scalability, making it a promising option for large-scale production. Each of these methods plays a crucial role in the global market for Pharmaceutical Grade Ergothioneine, catering to different needs and preferences of manufacturers and consumers. As the demand for this compound continues to grow, advancements in production technologies are likely to enhance the efficiency and sustainability of these methods, further driving the market expansion.

Skin Protective Agents, Ophthalmology, Other in the Pharmaceutical Grade Ergothioneine - Global Market:

Pharmaceutical Grade Ergothioneine is utilized in various applications, each benefiting from its unique properties. In the realm of skincare, it serves as a potent skin protective agent. Its antioxidant capabilities help neutralize free radicals, which are responsible for premature aging and skin damage. By incorporating ergothioneine into skincare products, manufacturers aim to offer consumers solutions that can protect against environmental stressors, such as UV radiation and pollution. This makes it a sought-after ingredient in anti-aging creams, serums, and sunscreens. In ophthalmology, ergothioneine is explored for its potential to protect eye health. The eyes are particularly susceptible to oxidative stress, which can lead to conditions like cataracts and age-related macular degeneration. Ergothioneine's ability to mitigate oxidative damage makes it a promising candidate for eye drops and supplements designed to support ocular health. Beyond skincare and ophthalmology, ergothioneine finds applications in other areas as well. It is used in dietary supplements aimed at boosting overall health and wellness, thanks to its antioxidant properties. Additionally, it is being researched for its potential benefits in neurological health, as oxidative stress is a known factor in neurodegenerative diseases. The versatility of Pharmaceutical Grade Ergothioneine in these diverse applications underscores its growing importance in the global market, as consumers increasingly seek products that offer natural and effective health benefits.

Pharmaceutical Grade Ergothioneine - Global Market Outlook:

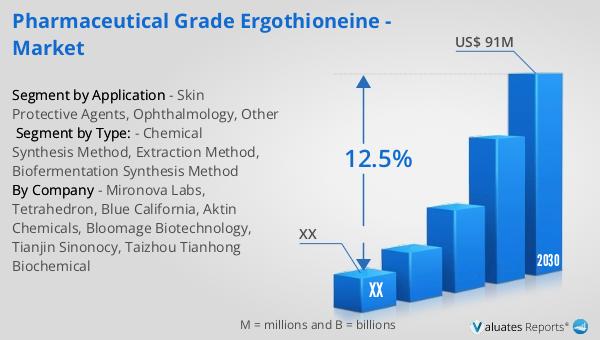

The global market for Pharmaceutical Grade Ergothioneine was valued at approximately $33 million in 2023. Projections indicate that this market is poised for significant growth, with expectations to reach an adjusted size of around $91 million by 2030. This growth trajectory reflects a compound annual growth rate (CAGR) of 12.5% during the forecast period from 2024 to 2030. The North American segment of this market also shows promising potential, although specific figures for 2023 and 2030 are not provided. The anticipated growth in this region is driven by increasing consumer awareness and demand for health and wellness products that incorporate natural antioxidants like ergothioneine. The robust CAGR suggests a strong market interest and investment in the development and application of Pharmaceutical Grade Ergothioneine across various industries. As more research highlights its benefits, and as production methods become more efficient and sustainable, the market is expected to continue its upward trend. This growth not only reflects the increasing demand for ergothioneine but also underscores the broader trend towards natural and effective health solutions in the global market.

| Report Metric | Details |

| Report Name | Pharmaceutical Grade Ergothioneine - Market |

| Forecasted market size in 2030 | US$ 91 million |

| CAGR | 12.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Mironova Labs, Tetrahedron, Blue California, Aktin Chemicals, Bloomage Biotechnology, Tianjin Sinonocy, Taizhou Tianhong Biochemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |