What is Naval Command and Control Systems - Global Market?

Naval Command and Control Systems are sophisticated technologies designed to enhance the operational efficiency and strategic capabilities of naval forces worldwide. These systems integrate various communication, navigation, and surveillance technologies to provide real-time data and situational awareness to naval commanders. By doing so, they enable more informed decision-making and effective coordination of naval operations. The global market for these systems is driven by the increasing need for advanced maritime security solutions, as well as the modernization of naval fleets across the globe. As geopolitical tensions rise and maritime threats become more complex, the demand for robust command and control systems is expected to grow. These systems not only improve the operational readiness of naval forces but also ensure the safety and security of maritime borders. With advancements in technology, naval command and control systems are becoming more sophisticated, incorporating artificial intelligence and machine learning to enhance their capabilities. This evolution is expected to further drive the market growth, as navies around the world seek to maintain a technological edge over potential adversaries.

Military, Homeland Security & Cyber Protection in the Naval Command and Control Systems - Global Market:

Naval Command and Control Systems play a crucial role in military operations, homeland security, and cyber protection. In the military domain, these systems are essential for coordinating naval operations, ensuring effective communication between ships, submarines, and aircraft. They provide commanders with a comprehensive view of the battlefield, enabling them to make strategic decisions quickly and efficiently. This is particularly important in modern warfare, where speed and accuracy are critical. In addition to military applications, these systems are also vital for homeland security. They help in monitoring and protecting national waters from various threats, including piracy, smuggling, and illegal fishing. By providing real-time data and situational awareness, naval command and control systems enable security forces to respond swiftly to any potential threats. Furthermore, these systems are integral to cyber protection efforts. As naval operations become increasingly reliant on digital technologies, the risk of cyberattacks has grown significantly. Naval command and control systems incorporate advanced cybersecurity measures to protect sensitive data and ensure the integrity of naval operations. This is essential for maintaining the operational readiness of naval forces and safeguarding national security. Overall, the integration of naval command and control systems into military, homeland security, and cyber protection efforts is critical for enhancing the effectiveness and resilience of these operations.

Industrial, Critical Infrastructure, Transportation, Smart City Command Center, Other in the Naval Command and Control Systems - Global Market:

The usage of Naval Command and Control Systems extends beyond military applications, finding relevance in various sectors such as industrial operations, critical infrastructure, transportation, smart city command centers, and more. In industrial settings, these systems are employed to enhance the security and efficiency of maritime logistics and supply chains. By providing real-time tracking and monitoring of vessels, they help in optimizing routes and ensuring timely delivery of goods. This is particularly important for industries that rely heavily on maritime transportation, such as oil and gas, shipping, and fisheries. In the realm of critical infrastructure, naval command and control systems are used to protect vital assets such as ports, offshore platforms, and underwater pipelines. They provide comprehensive surveillance and monitoring capabilities, enabling authorities to detect and respond to potential threats swiftly. In the transportation sector, these systems are utilized to improve the safety and efficiency of maritime traffic management. By providing real-time data on vessel movements, they help in preventing collisions and ensuring smooth navigation. Smart city command centers also benefit from naval command and control systems, as they provide enhanced situational awareness and coordination capabilities. This is particularly useful for managing maritime activities in urban coastal areas, where there is a high concentration of vessels and maritime infrastructure. Overall, the versatility and effectiveness of naval command and control systems make them invaluable tools for enhancing security and operational efficiency across various sectors.

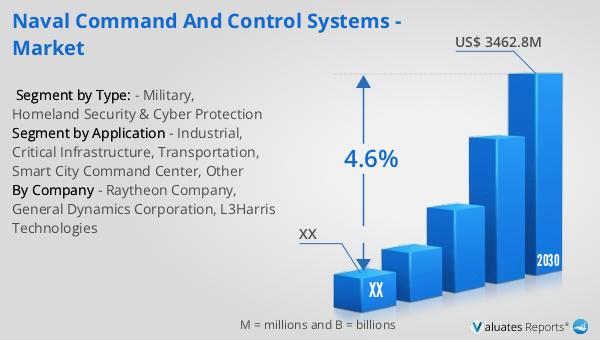

Naval Command and Control Systems - Global Market Outlook:

The global market for Naval Command and Control Systems was valued at approximately $2,538.7 million in 2023, with projections indicating a growth to around $3,462.8 million by 2030. This represents a compound annual growth rate (CAGR) of 4.6% over the forecast period from 2024 to 2030. In North America, the market for these systems was also valued at a significant amount in 2023, with expectations of continued growth through 2030. The CAGR for the North American market during this period is anticipated to reflect the global trend, driven by the increasing demand for advanced naval technologies and the modernization of naval fleets. This growth is fueled by the need for enhanced maritime security and the adoption of cutting-edge technologies in naval operations. As geopolitical tensions and maritime threats continue to evolve, the demand for sophisticated command and control systems is expected to rise, further driving market expansion. The integration of advanced technologies such as artificial intelligence and machine learning into naval command and control systems is also expected to contribute to market growth, as navies seek to maintain a technological edge over potential adversaries. Overall, the global market for naval command and control systems is poised for significant growth, driven by the increasing need for advanced maritime security solutions and the modernization of naval fleets worldwide.

| Report Metric | Details |

| Report Name | Naval Command and Control Systems - Market |

| Forecasted market size in 2030 | US$ 3462.8 million |

| CAGR | 4.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Raytheon Company, General Dynamics Corporation, L3Harris Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |