What is SoC Deep Learning Chip - Global Market?

The System on Chip (SoC) Deep Learning Chip market is a rapidly evolving segment within the broader semiconductor industry. These chips are designed to handle complex computations required for deep learning tasks, which are a subset of artificial intelligence (AI). Deep learning involves training algorithms to recognize patterns and make decisions based on large datasets, and SoC chips are integral in processing these tasks efficiently. Unlike traditional processors, SoC deep learning chips integrate multiple components such as CPUs, GPUs, memory, and other peripherals into a single chip, optimizing performance and energy efficiency. This integration allows for faster data processing and reduced latency, making them ideal for applications that require real-time data analysis. The global market for these chips is expanding as industries increasingly adopt AI technologies to enhance their operations, improve customer experiences, and drive innovation. As a result, the demand for SoC deep learning chips is expected to grow, driven by advancements in AI and machine learning technologies, as well as the increasing need for efficient data processing solutions across various sectors.

Graphics Processing Units, Central Processing Units, Application Specific Integrated Circuits, Field Programmable Gate Arrays, Others in the SoC Deep Learning Chip - Global Market:

Graphics Processing Units (GPUs), Central Processing Units (CPUs), Application Specific Integrated Circuits (ASICs), and Field Programmable Gate Arrays (FPGAs) are key components in the SoC Deep Learning Chip market, each playing a unique role in processing deep learning tasks. GPUs are highly efficient at handling parallel processing tasks, making them ideal for deep learning applications that require simultaneous computations. They excel in training deep learning models due to their ability to process multiple data streams concurrently, significantly speeding up the learning process. CPUs, on the other hand, are versatile processors that handle a wide range of tasks. While not as specialized as GPUs for deep learning, CPUs are essential for managing general-purpose computing tasks and coordinating the operations of other components within the SoC. ASICs are custom-designed chips tailored for specific applications, offering high performance and energy efficiency for deep learning tasks. They are optimized for particular algorithms, providing faster processing speeds and lower power consumption compared to general-purpose processors. FPGAs are reconfigurable chips that can be programmed to perform specific tasks, offering flexibility and adaptability in deep learning applications. They are particularly useful in scenarios where the deep learning models or algorithms are frequently updated, as they can be reprogrammed to accommodate changes without the need for new hardware. Each of these components contributes to the overall performance and efficiency of SoC deep learning chips, enabling them to meet the diverse needs of various industries. As the demand for AI-driven solutions continues to rise, the integration and optimization of these components within SoC chips will play a crucial role in advancing the capabilities of deep learning technologies.

BFSI, Telecommunication, Automotive, Healthcare, Others in the SoC Deep Learning Chip - Global Market:

The usage of SoC Deep Learning Chips spans across various industries, including Banking, Financial Services, and Insurance (BFSI), Telecommunication, Automotive, Healthcare, and others. In the BFSI sector, these chips are used to enhance fraud detection systems, automate customer service through chatbots, and improve risk management by analyzing large volumes of financial data in real-time. The ability to process data quickly and accurately allows financial institutions to make informed decisions and provide better services to their customers. In the telecommunication industry, SoC deep learning chips are employed to optimize network performance, enhance security, and improve customer experience through personalized services. They enable telecom companies to analyze vast amounts of data generated by users and networks, allowing for more efficient management of resources and faster response to customer needs. In the automotive sector, these chips are crucial for developing advanced driver-assistance systems (ADAS) and autonomous vehicles. They process data from various sensors and cameras in real-time, enabling vehicles to make split-second decisions and improve safety on the roads. In healthcare, SoC deep learning chips are used for medical imaging analysis, drug discovery, and personalized medicine. They help in processing complex medical data, leading to more accurate diagnoses and tailored treatment plans for patients. Other industries, such as retail and manufacturing, also benefit from these chips by using them to enhance supply chain management, improve customer insights, and optimize production processes. The versatility and efficiency of SoC deep learning chips make them indispensable in driving innovation and improving operational efficiency across different sectors.

SoC Deep Learning Chip - Global Market Outlook:

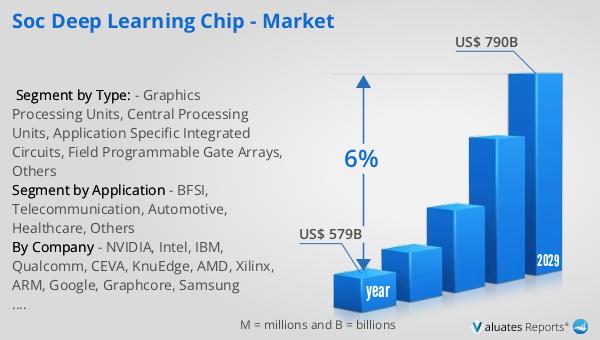

The semiconductor market, which includes SoC Deep Learning Chips, was valued at approximately $579 billion in 2022. This market is anticipated to grow significantly, reaching around $790 billion by 2029. This growth represents a compound annual growth rate (CAGR) of 6% over the forecast period. The expansion of the semiconductor market is driven by the increasing demand for advanced technologies such as artificial intelligence, machine learning, and the Internet of Things (IoT), which require efficient and powerful processing capabilities. SoC deep learning chips, with their ability to integrate multiple processing units and optimize performance, are at the forefront of this growth. As industries continue to adopt AI-driven solutions to enhance their operations and improve customer experiences, the demand for these chips is expected to rise. The growing need for real-time data processing and analysis across various sectors, including automotive, healthcare, and telecommunications, further fuels the demand for SoC deep learning chips. Additionally, advancements in semiconductor manufacturing technologies are enabling the production of more efficient and powerful chips, contributing to the overall growth of the market. As a result, the semiconductor market is poised for significant expansion in the coming years, driven by the increasing adoption of AI and machine learning technologies and the growing need for efficient data processing solutions.

| Report Metric | Details |

| Report Name | SoC Deep Learning Chip - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | NVIDIA, Intel, IBM, Qualcomm, CEVA, KnuEdge, AMD, Xilinx, ARM, Google, Graphcore, Samsung Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |