What is Disposable Safety Pen Needles - Global Market?

Disposable safety pen needles are a crucial component in the global healthcare market, specifically designed for safe and efficient drug delivery. These needles are primarily used with pen injectors, which are devices that allow patients to self-administer medications, such as insulin, with ease and precision. The global market for disposable safety pen needles is driven by the increasing prevalence of chronic diseases like diabetes, which require regular and precise medication administration. These needles are designed to minimize pain and discomfort during injections, making them more user-friendly, especially for those who need frequent injections. Additionally, the safety features of these needles, such as automatic retraction or shielding mechanisms, help prevent needlestick injuries, which are a significant concern in both home and clinical settings. The demand for these needles is also fueled by the growing awareness of the importance of safety in medical procedures, as well as advancements in needle technology that enhance patient comfort and compliance. As healthcare systems worldwide continue to emphasize patient safety and convenience, the market for disposable safety pen needles is expected to expand, catering to a diverse range of medical needs and settings.

4mm, 5mm, 6mm, 8mm, Others in the Disposable Safety Pen Needles - Global Market:

In the global market for disposable safety pen needles, various sizes cater to different patient needs and preferences, including 4mm, 5mm, 6mm, 8mm, and other sizes. The 4mm needles are the shortest and are often preferred by patients who are new to self-injection or those who have a fear of needles. These needles are designed to minimize pain and anxiety, making them ideal for children or individuals with a low body mass index (BMI). The 5mm needles offer a slightly longer option, providing a balance between comfort and effective medication delivery. They are suitable for a broader range of patients, including those who require a bit more penetration depth for optimal drug absorption. The 6mm needles are commonly used by adults and are considered a standard size for many injectable medications. They provide sufficient depth to ensure the medication is delivered into the subcutaneous tissue, which is crucial for the efficacy of many drugs. The 8mm needles are longer and are typically used for patients with higher BMI or those who require deeper penetration to reach the subcutaneous layer. These needles are often used in clinical settings where precise drug delivery is critical. Other sizes are available to accommodate specific medical needs or patient preferences, ensuring that there is a suitable option for everyone. The availability of different needle sizes highlights the importance of personalized medicine, where treatment is tailored to the individual needs of the patient. This approach not only improves patient outcomes but also enhances the overall experience of self-injection, making it less daunting and more manageable. As the global market for disposable safety pen needles continues to grow, manufacturers are likely to focus on developing innovative solutions that address the diverse needs of patients worldwide. This includes improving needle technology to reduce pain, enhance safety, and increase the ease of use, ultimately contributing to better health outcomes and patient satisfaction.

Home Use, Medical Institutions, Others in the Disposable Safety Pen Needles - Global Market:

Disposable safety pen needles are widely used in various settings, including home use, medical institutions, and other areas, each with its unique requirements and benefits. In home use, these needles provide patients with the convenience and autonomy to manage their health conditions independently. This is particularly beneficial for individuals with chronic conditions like diabetes, who require regular insulin injections. The ease of use and safety features of these needles make them ideal for home settings, where patients may not have immediate access to professional medical assistance. The ability to self-administer medication safely and effectively empowers patients, reduces the need for frequent hospital visits, and enhances their quality of life. In medical institutions, disposable safety pen needles are essential for ensuring the safety of both patients and healthcare professionals. The safety mechanisms, such as automatic retraction or shielding, help prevent needlestick injuries, which are a significant concern in clinical environments. These needles also facilitate efficient and accurate drug delivery, which is crucial for patient care in hospitals and clinics. The use of disposable needles in medical institutions also helps maintain hygiene and prevent cross-contamination, as each needle is used only once and then safely disposed of. In other areas, such as community health programs or emergency medical services, disposable safety pen needles play a vital role in providing quick and safe access to medication. These settings often require portable and easy-to-use solutions for drug administration, and disposable pen needles meet these needs effectively. The versatility and reliability of these needles make them an indispensable tool in various healthcare scenarios, contributing to improved health outcomes and patient safety across the board. As the demand for safe and convenient drug delivery solutions continues to rise, the usage of disposable safety pen needles is expected to expand, reaching more patients and healthcare providers worldwide.

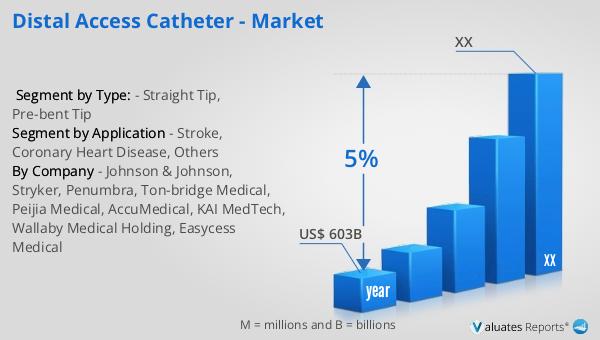

Disposable Safety Pen Needles - Global Market Outlook:

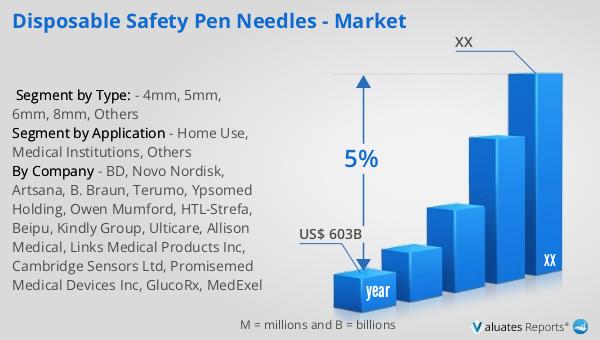

Based on our research, the global market for medical devices, which includes disposable safety pen needles, is projected to be valued at approximately USD 603 billion in 2023. This market is anticipated to experience a steady growth rate, with a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and a growing emphasis on patient safety and convenience. The demand for medical devices, such as disposable safety pen needles, is expected to rise as healthcare systems worldwide continue to prioritize efficient and safe drug delivery methods. The market's expansion is also supported by the growing awareness of the importance of preventing needlestick injuries and ensuring patient comfort during injections. As more patients and healthcare providers recognize the benefits of using disposable safety pen needles, the market is likely to see increased adoption and innovation in this area. Manufacturers are expected to focus on developing new and improved needle designs that cater to the diverse needs of patients, enhancing both the safety and efficacy of drug delivery. Overall, the global market for medical devices, including disposable safety pen needles, is poised for significant growth, driven by the ongoing advancements in healthcare and the increasing demand for safe and convenient medical solutions.

| Report Metric | Details |

| Report Name | Disposable Safety Pen Needles - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BD, Novo Nordisk, Artsana, B. Braun, Terumo, Ypsomed Holding, Owen Mumford, HTL-Strefa, Beipu, Kindly Group, Ulticare, Allison Medical, Links Medical Products Inc, Cambridge Sensors Ltd, Promisemed Medical Devices Inc, GlucoRx, MedExel |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |