What is Pet Premixed Feed - Global Market?

Pet premixed feed is a specialized product designed to provide pets with a balanced diet that meets their nutritional needs. This feed is a blend of various ingredients, including vitamins, minerals, proteins, and other essential nutrients, pre-mixed to ensure consistency and convenience for pet owners. The global market for pet premixed feed has been growing steadily, driven by the increasing awareness among pet owners about the importance of proper nutrition for their pets. As more people consider pets as part of their family, they are willing to invest in high-quality food products that promote health and longevity. The market is characterized by a wide range of products catering to different types of pets, including dogs, cats, birds, and small mammals. Manufacturers are continuously innovating to develop new formulations that address specific health concerns, such as weight management, digestive health, and skin and coat care. Additionally, the rise of e-commerce has made it easier for consumers to access a variety of pet premixed feed products, further fueling market growth. As a result, the pet premixed feed market is poised for continued expansion, with opportunities for both established players and new entrants to capture a share of this lucrative market.

Powder, Liquid in the Pet Premixed Feed - Global Market:

In the global market for pet premixed feed, products are typically available in two main forms: powder and liquid. Each form has its own set of advantages and is chosen based on the specific needs of the pet and the preferences of the pet owner. Powdered pet premixed feed is popular due to its long shelf life and ease of storage. It is often used for dry pet food formulations and can be easily mixed with water or other liquids to create a palatable meal for pets. The powdered form allows for precise control over the nutrient content, making it ideal for pets with specific dietary requirements. Additionally, powdered feed is lightweight and easy to transport, making it a convenient option for pet owners who travel frequently with their pets. On the other hand, liquid pet premixed feed is gaining popularity due to its ease of use and quick absorption by pets. Liquid formulations are often used for wet pet food products and are particularly beneficial for pets with dental issues or those that have difficulty chewing dry food. The liquid form ensures that pets receive a consistent and balanced intake of nutrients with every meal. Moreover, liquid feed can be easily mixed with other food items, allowing pet owners to customize their pet's diet according to their preferences. The choice between powder and liquid pet premixed feed often depends on factors such as the pet's age, health condition, and dietary preferences. For instance, puppies and kittens may benefit from liquid feed due to its ease of digestion, while adult pets may thrive on powdered formulations that offer a higher concentration of nutrients. Additionally, the growing trend of pet humanization has led to an increased demand for premium and specialized pet premixed feed products. Pet owners are increasingly seeking out products that are free from artificial additives and preservatives, opting instead for natural and organic ingredients. This shift in consumer preferences has prompted manufacturers to develop innovative formulations that cater to the evolving needs of pet owners. Furthermore, the rise of e-commerce platforms has made it easier for consumers to access a wide range of pet premixed feed products, allowing them to compare prices and read reviews before making a purchase. This increased accessibility has contributed to the growth of the global pet premixed feed market, as more pet owners are able to find products that meet their specific needs. In conclusion, the global market for pet premixed feed is characterized by a diverse range of products available in both powder and liquid forms. Each form offers unique benefits and is chosen based on the specific needs of the pet and the preferences of the pet owner. As the market continues to grow, manufacturers are likely to focus on developing innovative formulations that cater to the evolving needs of pet owners, ensuring that pets receive the best possible nutrition.

Cat, Dog in the Pet Premixed Feed - Global Market:

The usage of pet premixed feed in the global market is particularly significant for cats and dogs, as these are among the most popular pets worldwide. For cats, premixed feed provides a convenient and reliable source of nutrition that meets their unique dietary needs. Cats are obligate carnivores, meaning they require a diet high in animal protein and specific nutrients such as taurine, arachidonic acid, and vitamin A, which are not found in plant-based foods. Pet premixed feed for cats is formulated to provide these essential nutrients in the right proportions, ensuring that cats receive a balanced diet that supports their overall health and well-being. Additionally, premixed feed for cats often includes ingredients that promote urinary tract health, reduce hairballs, and support a healthy skin and coat. For dogs, premixed feed offers a convenient way to provide a balanced diet that meets their diverse nutritional needs. Dogs are omnivores and require a diet that includes a mix of proteins, carbohydrates, fats, vitamins, and minerals. Pet premixed feed for dogs is designed to provide these nutrients in the right balance, supporting their growth, energy levels, and overall health. Many premixed feed products for dogs also include ingredients that promote joint health, support a healthy digestive system, and enhance the immune system. The convenience of premixed feed is particularly appealing to pet owners who may not have the time or expertise to prepare homemade meals for their pets. By choosing premixed feed, pet owners can ensure that their cats and dogs receive a consistent and balanced diet without the need for additional supplements. Moreover, the availability of specialized formulations allows pet owners to address specific health concerns, such as weight management, allergies, or age-related issues. As the global market for pet premixed feed continues to grow, manufacturers are likely to focus on developing innovative products that cater to the evolving needs of pet owners. This includes the development of premium and specialized formulations that address specific dietary requirements and health concerns. Additionally, the rise of e-commerce platforms has made it easier for pet owners to access a wide range of premixed feed products, allowing them to compare prices and read reviews before making a purchase. This increased accessibility has contributed to the growth of the global pet premixed feed market, as more pet owners are able to find products that meet their specific needs. In conclusion, the usage of pet premixed feed in the global market is particularly significant for cats and dogs, as these pets have unique dietary needs that require a balanced and consistent source of nutrition. The convenience and reliability of premixed feed make it an appealing choice for pet owners, ensuring that their pets receive the best possible nutrition.

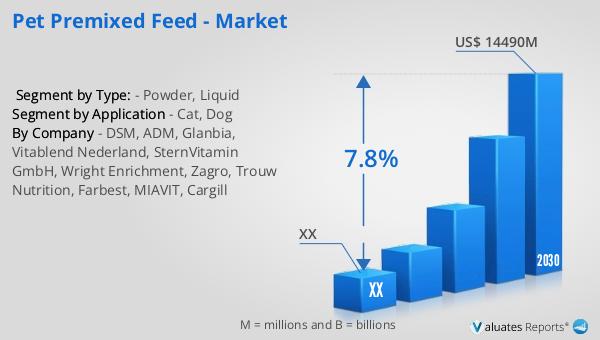

Pet Premixed Feed - Global Market Outlook:

The global market for pet premixed feed was valued at approximately $8,519 million in 2023, and it is projected to grow to a revised size of $14,490 million by 2030, reflecting a compound annual growth rate (CAGR) of 7.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for high-quality pet nutrition products as pet owners become more aware of the importance of providing balanced diets for their pets. According to data from the PET Supplies Research Center, the global pet industry reached a value of $261 billion in 2022, marking an impressive year-on-year increase of 11.3%. This growth in the pet industry is driven by several factors, including the rising trend of pet humanization, where pets are increasingly seen as family members, leading to higher spending on pet care products. Additionally, the expansion of e-commerce platforms has made it easier for consumers to access a wide range of pet products, further fueling market growth. As the pet premixed feed market continues to expand, manufacturers are likely to focus on developing innovative products that cater to the evolving needs of pet owners, ensuring that pets receive the best possible nutrition. This growth presents significant opportunities for both established players and new entrants to capture a share of this lucrative market.

| Report Metric | Details |

| Report Name | Pet Premixed Feed - Market |

| Forecasted market size in 2030 | US$ 14490 million |

| CAGR | 7.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | DSM, ADM, Glanbia, Vitablend Nederland, SternVitamin GmbH, Wright Enrichment, Zagro, Trouw Nutrition, Farbest, MIAVIT, Cargill |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |