What is Industrial Microsensors - Global Market?

Industrial microsensors are tiny devices that play a crucial role in various industries by detecting and measuring physical quantities such as temperature, pressure, flow, and position. These sensors are integral to the global market, providing essential data that helps in monitoring and controlling industrial processes. The global market for industrial microsensors is vast and continuously growing, driven by the increasing demand for automation and precision in industries like manufacturing, automotive, and healthcare. These sensors are designed to be highly sensitive and accurate, allowing for real-time data collection and analysis, which is vital for optimizing operations and ensuring safety. The market is characterized by rapid technological advancements, leading to the development of more sophisticated and efficient sensors. As industries strive for greater efficiency and sustainability, the demand for industrial microsensors is expected to rise, making them a key component in the future of industrial automation and control systems. The versatility and adaptability of these sensors make them indispensable in various applications, from monitoring environmental conditions to ensuring the proper functioning of complex machinery. With the ongoing advancements in sensor technology, the industrial microsensors market is poised for significant growth, offering numerous opportunities for innovation and development.

Level Sensor, Temperature Sensor, Flow Sensor, Position Sensor, Pressure Sensor, Others in the Industrial Microsensors - Global Market:

Industrial microsensors encompass a variety of sensor types, each serving a specific function in monitoring and controlling industrial processes. Level sensors are used to detect the level of substances such as liquids, powders, or granular materials within a container or space. They are crucial in industries like water treatment, food and beverage, and pharmaceuticals, where maintaining precise levels is essential for quality control and safety. Temperature sensors, on the other hand, measure the temperature of an environment or object, providing critical data for processes that require specific thermal conditions. These sensors are widely used in industries such as manufacturing, automotive, and electronics, where temperature control is vital for product quality and equipment longevity. Flow sensors measure the rate of fluid movement through a system, which is essential for applications in water management, chemical processing, and HVAC systems. They help ensure that fluids are moving at the correct rate, preventing issues such as leaks or blockages. Position sensors detect the position or movement of an object, playing a key role in automation and robotics by providing feedback on the location and movement of components. These sensors are used in industries like automotive, aerospace, and manufacturing, where precise positioning is crucial for efficient operations. Pressure sensors measure the force exerted by a fluid or gas, providing data that is essential for maintaining safe and efficient operations in industries such as oil and gas, chemical processing, and HVAC systems. They help prevent equipment failure and ensure that systems are operating within safe pressure limits. Other types of industrial microsensors include humidity sensors, which measure the moisture content in the air, and gas sensors, which detect the presence of specific gases in an environment. These sensors are used in a variety of applications, from environmental monitoring to ensuring air quality in industrial settings. The diversity of industrial microsensors and their applications highlights their importance in modern industrial processes, where precision and reliability are paramount.

Energy & Power, Oil & Gas, Mining, Chemical, Others in the Industrial Microsensors - Global Market:

Industrial microsensors are widely used across various sectors, including energy and power, oil and gas, mining, chemical, and others, due to their ability to provide precise and reliable data. In the energy and power sector, these sensors are essential for monitoring and controlling the generation, transmission, and distribution of electricity. They help ensure the efficient operation of power plants and grids by providing real-time data on parameters such as temperature, pressure, and flow. This data is crucial for optimizing performance, reducing downtime, and preventing equipment failures. In the oil and gas industry, industrial microsensors are used to monitor drilling operations, pipeline integrity, and refinery processes. They provide critical data on pressure, temperature, and flow rates, helping to ensure safe and efficient operations. These sensors are also used in exploration activities to gather data on geological formations and assess the viability of potential drilling sites. In the mining industry, industrial microsensors are used to monitor environmental conditions, equipment performance, and worker safety. They provide data on parameters such as air quality, temperature, and vibration, helping to ensure safe and efficient operations. In the chemical industry, these sensors are used to monitor and control chemical reactions, ensuring that processes are carried out safely and efficiently. They provide data on parameters such as temperature, pressure, and flow rates, helping to optimize production and reduce waste. Other industries that use industrial microsensors include automotive, aerospace, and healthcare, where they are used to monitor and control various processes and systems. The versatility and adaptability of industrial microsensors make them indispensable in a wide range of applications, where precision and reliability are essential.

Industrial Microsensors - Global Market Outlook:

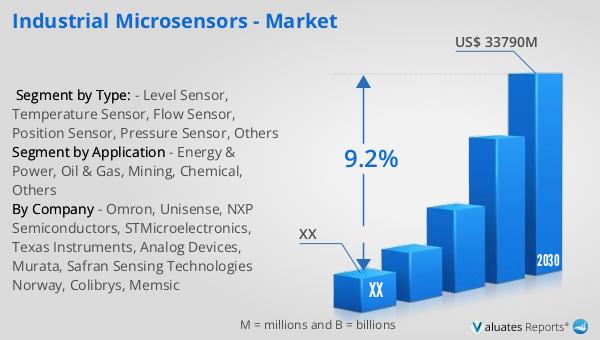

The global market for industrial microsensors was valued at approximately $18,960 million in 2023, with projections indicating a significant increase to around $33,790 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 9.2% during the forecast period from 2024 to 2030. The North American market for industrial microsensors, although not specified in exact figures, is anticipated to follow a similar growth trajectory, contributing to the overall expansion of the global market. This growth is driven by the increasing demand for automation and precision in various industries, as well as the ongoing advancements in sensor technology. The rising adoption of industrial microsensors in sectors such as manufacturing, automotive, and healthcare is expected to further fuel market growth. As industries continue to seek greater efficiency and sustainability, the demand for industrial microsensors is likely to increase, making them a key component in the future of industrial automation and control systems. The versatility and adaptability of these sensors, combined with their ability to provide precise and reliable data, make them indispensable in a wide range of applications. With the ongoing advancements in sensor technology, the industrial microsensors market is poised for significant growth, offering numerous opportunities for innovation and development.

| Report Metric | Details |

| Report Name | Industrial Microsensors - Market |

| Forecasted market size in 2030 | US$ 33790 million |

| CAGR | 9.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Omron, Unisense, NXP Semiconductors, STMicroelectronics, Texas Instruments, Analog Devices, Murata, Safran Sensing Technologies Norway, Colibrys, Memsic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |