What is Automotive Music Platform - Global Market?

The Automotive Music Platform - Global Market is a rapidly evolving sector that integrates music streaming services into vehicles, enhancing the driving experience by providing seamless access to music. This market encompasses a variety of platforms and services that allow drivers and passengers to stream music directly through their vehicle's audio system. With advancements in technology, these platforms are becoming increasingly sophisticated, offering features such as voice control, personalized playlists, and integration with other in-car systems. The growth of this market is driven by the increasing demand for connected vehicles and the rising popularity of music streaming services. As more consumers seek to personalize their in-car experience, automotive manufacturers and tech companies are collaborating to offer innovative solutions that cater to this demand. The global reach of this market is significant, with major players operating across different regions to provide localized content and services. As the automotive industry continues to embrace digital transformation, the integration of music platforms into vehicles is expected to become a standard feature, further driving the growth of this market.

Free, Subscription in the Automotive Music Platform - Global Market:

The Automotive Music Platform - Global Market offers both free and subscription-based services, catering to a wide range of consumer preferences. Free services typically provide basic access to music streaming with limited features and are often supported by advertisements. These platforms allow users to listen to music without any upfront cost, making them an attractive option for budget-conscious consumers. However, the presence of ads and limited functionality can be a drawback for some users. On the other hand, subscription-based services offer a premium experience with enhanced features such as ad-free listening, offline downloads, and high-quality audio. These services require a monthly or annual fee, providing a steady revenue stream for service providers. Subscription models are popular among users who value a seamless and uninterrupted music experience. The choice between free and subscription-based services often depends on individual preferences and the level of convenience desired. In the global market, there is a growing trend towards subscription-based models as consumers increasingly prioritize quality and convenience over cost. This shift is also influenced by the rising disposable income and changing lifestyle patterns, particularly in emerging markets. As a result, many automotive music platforms are expanding their subscription offerings to capture this growing demand. Additionally, partnerships between automotive manufacturers and music streaming companies are becoming more common, allowing for integrated subscription services that enhance the overall in-car experience. These collaborations often result in exclusive content and features that are only available to subscribers, further incentivizing consumers to opt for paid services. The competitive landscape of the Automotive Music Platform - Global Market is characterized by a mix of established players and new entrants, each vying for a share of the growing market. Companies are investing in research and development to innovate and differentiate their offerings, focusing on aspects such as user interface, content library, and integration capabilities. As the market continues to evolve, the balance between free and subscription-based services will play a crucial role in shaping consumer preferences and driving growth.

Commercial Vehicle, Passenger Car in the Automotive Music Platform - Global Market:

The usage of Automotive Music Platforms in commercial vehicles and passenger cars varies significantly, reflecting the distinct needs and preferences of these two segments. In commercial vehicles, such as trucks and buses, music platforms are primarily used to enhance the driving experience for long-haul drivers and passengers. These platforms provide a source of entertainment and relaxation, helping to alleviate the monotony of long journeys. For commercial drivers, access to a wide range of music genres and playlists can improve mood and concentration, contributing to safer driving conditions. Additionally, music platforms in commercial vehicles often include features such as voice control and hands-free operation, allowing drivers to manage their music selection without distraction. This integration of music platforms into commercial vehicles is increasingly seen as a value-added feature, enhancing the overall appeal of these vehicles to fleet operators and individual owners alike. In passenger cars, the use of automotive music platforms is more focused on personalization and convenience. With the growing trend of connected cars, passengers expect seamless access to their favorite music and playlists while on the go. Music platforms in passenger cars offer a range of features, including personalized recommendations, curated playlists, and integration with other in-car systems such as navigation and voice assistants. This level of integration allows passengers to enjoy a customized music experience that aligns with their preferences and enhances their overall journey. The demand for automotive music platforms in passenger cars is driven by the increasing consumer expectation for a connected and personalized in-car experience. As a result, automotive manufacturers are investing in partnerships with music streaming companies to offer integrated solutions that cater to this demand. These collaborations often result in exclusive content and features that enhance the appeal of passenger cars to tech-savvy consumers. Overall, the usage of automotive music platforms in both commercial vehicles and passenger cars is a reflection of the broader trend towards digitalization and connectivity in the automotive industry. As technology continues to advance, the integration of music platforms into vehicles is expected to become more sophisticated, offering an even greater range of features and capabilities to enhance the driving experience.

Automotive Music Platform - Global Market Outlook:

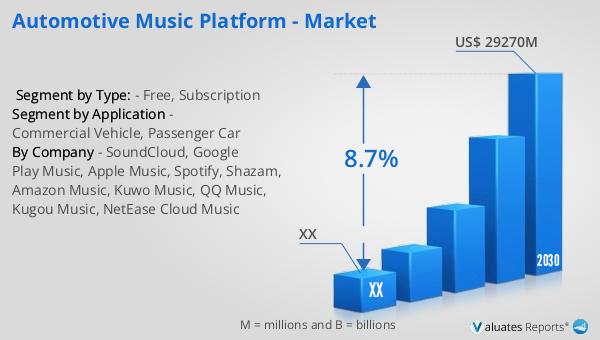

The global market for Automotive Music Platforms was valued at approximately $16,490 million in 2023 and is projected to grow to a revised size of $29,270 million by 2030, with a compound annual growth rate (CAGR) of 8.7% during the forecast period from 2024 to 2030. Currently, over 90% of the world's automobiles are concentrated in three major continents: Asia, Europe, and North America. Asia leads the way in automobile production, accounting for 56% of the global output, followed by Europe at 20%, and North America at 16%. This distribution highlights the significant role these regions play in the automotive industry and, by extension, the automotive music platform market. The concentration of automobile production in these regions is a key driver for the growth of the automotive music platform market, as manufacturers and service providers focus on catering to the needs of consumers in these areas. The increasing demand for connected vehicles and the rising popularity of music streaming services are further fueling the growth of this market. As the automotive industry continues to evolve, the integration of music platforms into vehicles is expected to become a standard feature, driving further growth and innovation in this sector.

| Report Metric | Details |

| Report Name | Automotive Music Platform - Market |

| Forecasted market size in 2030 | US$ 29270 million |

| CAGR | 8.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | SoundCloud, Google Play Music, Apple Music, Spotify, Shazam, Amazon Music, Kuwo Music, QQ Music, Kugou Music, NetEase Cloud Music |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |