What is Absorbable Polysaccharide Hemostatic Material - Global Market?

Absorbable polysaccharide hemostatic materials are specialized medical products designed to control bleeding during surgical procedures or after traumatic injuries. These materials are derived from natural polysaccharides, which are complex carbohydrates found in plants. When applied to a bleeding site, they work by accelerating the body's natural clotting process, effectively stopping the flow of blood. The global market for these materials is expanding as they offer several advantages over traditional hemostatic agents. They are biodegradable, meaning they are absorbed by the body over time, reducing the need for removal and minimizing the risk of infection or complications. This makes them particularly useful in surgeries where leaving foreign materials in the body could pose a risk. The demand for absorbable polysaccharide hemostatic materials is driven by the increasing number of surgical procedures worldwide, advancements in medical technology, and a growing awareness of the benefits of using biodegradable materials in medical applications. As healthcare systems continue to evolve, the adoption of these innovative hemostatic solutions is expected to rise, providing safer and more efficient options for bleeding control in various medical settings.

Cellulose, Starch, Chitosan, Others in the Absorbable Polysaccharide Hemostatic Material - Global Market:

Absorbable polysaccharide hemostatic materials are primarily composed of cellulose, starch, chitosan, and other polysaccharides, each offering unique properties that make them suitable for different medical applications. Cellulose, a natural polymer found in the cell walls of plants, is widely used due to its excellent biocompatibility and ability to form a gel-like structure when in contact with blood. This gel acts as a physical barrier, helping to stop bleeding by providing a scaffold for clot formation. Cellulose-based hemostatic agents are often used in surgeries where rapid hemostasis is required, such as in cardiovascular or orthopedic procedures. Starch, another polysaccharide, is valued for its rapid absorption and ability to swell upon contact with blood, creating a mechanical barrier that aids in clot formation. Starch-based hemostatic materials are particularly useful in situations where quick absorption is necessary, such as in minimally invasive surgeries or in patients with compromised healing abilities. Chitosan, derived from the shells of crustaceans, is known for its antimicrobial properties and ability to promote wound healing. It works by attracting red blood cells and platelets to the site of injury, facilitating the formation of a stable clot. Chitosan-based hemostatic agents are often used in trauma care and emergency settings due to their effectiveness in controlling severe bleeding. Other polysaccharides, such as alginate and dextran, are also used in the development of hemostatic materials, each offering distinct advantages in terms of absorption rate, biocompatibility, and ease of use. The choice of material depends on the specific requirements of the surgical procedure and the patient's condition. As research in this field continues to advance, new formulations and combinations of polysaccharides are being explored to enhance the efficacy and safety of absorbable hemostatic materials. The global market for these materials is characterized by a diverse range of products, each tailored to meet the needs of different medical specialties and surgical techniques. With ongoing innovations and increasing demand for safer and more effective hemostatic solutions, the market for absorbable polysaccharide hemostatic materials is poised for significant growth in the coming years.

Hospital, Clinic in the Absorbable Polysaccharide Hemostatic Material - Global Market:

In hospitals and clinics, absorbable polysaccharide hemostatic materials play a crucial role in managing bleeding during and after surgical procedures. In hospital settings, these materials are used across various departments, including surgery, emergency, and intensive care units. Surgeons rely on these hemostatic agents to control bleeding in complex procedures, such as cardiovascular, neurosurgery, and organ transplants, where precision and rapid hemostasis are critical. The use of absorbable materials reduces the risk of postoperative complications, such as infections or adhesions, as they are naturally absorbed by the body over time. This is particularly beneficial in surgeries where leaving foreign materials in the body could lead to adverse reactions. In clinics, where minor surgical procedures and wound care are common, absorbable polysaccharide hemostatic materials offer a convenient and effective solution for managing bleeding. They are easy to apply and do not require removal, making them ideal for outpatient settings where quick recovery and minimal follow-up are desired. In both hospitals and clinics, the use of these materials contributes to improved patient outcomes by reducing the risk of excessive bleeding and associated complications. Additionally, they help streamline surgical procedures by minimizing the time required for hemostasis, allowing healthcare providers to focus on other critical aspects of patient care. The versatility and effectiveness of absorbable polysaccharide hemostatic materials make them an essential component of modern medical practice, supporting healthcare professionals in delivering safe and efficient care to patients. As the demand for minimally invasive procedures and advanced wound care solutions continues to grow, the adoption of these innovative hemostatic materials is expected to increase, further enhancing their role in hospital and clinic settings worldwide.

Absorbable Polysaccharide Hemostatic Material - Global Market Outlook:

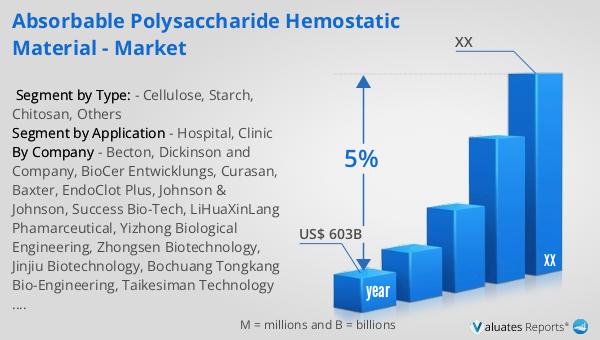

Our research indicates that the global market for medical devices, including absorbable polysaccharide hemostatic materials, is projected to reach approximately $603 billion in 2023. This market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and a growing aging population that requires more surgical interventions. The demand for innovative and effective medical devices, such as absorbable hemostatic materials, is rising as healthcare providers seek to improve patient outcomes and reduce the risk of complications. The adoption of these materials is further supported by the trend towards minimally invasive procedures, which require efficient hemostatic solutions to ensure patient safety and quick recovery. As healthcare systems worldwide continue to evolve, the market for absorbable polysaccharide hemostatic materials is expected to expand, offering new opportunities for manufacturers and healthcare providers alike. This growth reflects the ongoing commitment to enhancing the quality of care and improving the overall efficiency of medical procedures.

| Report Metric | Details |

| Report Name | Absorbable Polysaccharide Hemostatic Material - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Becton, Dickinson and Company, BioCer Entwicklungs, Curasan, Baxter, EndoClot Plus, Johnson & Johnson, Success Bio-Tech, LiHuaXinLang Phamarceutical, Yizhong Biological Engineering, Zhongsen Biotechnology, Jinjiu Biotechnology, Bochuang Tongkang Bio-Engineering, Taikesiman Technology Development |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |