What is Industrial Pipe Insulation Materials - Global Market?

Industrial pipe insulation materials are essential components in various industries, serving to maintain temperature, conserve energy, and ensure safety. These materials are used to insulate pipes that transport fluids, gases, or other substances, helping to prevent heat loss or gain, reduce energy consumption, and protect personnel from extreme temperatures. The global market for industrial pipe insulation materials is driven by the increasing demand for energy efficiency and the need to comply with stringent environmental regulations. These materials are used in a wide range of industries, including chemical, food and beverages, oil and gas, power, and metal manufacturing, among others. The market is characterized by a diverse range of insulation materials, each offering unique properties and benefits. As industries continue to seek ways to improve operational efficiency and reduce costs, the demand for effective pipe insulation solutions is expected to grow. This market is also influenced by technological advancements and innovations in insulation materials, which offer improved performance and sustainability. Overall, the industrial pipe insulation materials market plays a crucial role in supporting industrial operations and contributing to energy conservation efforts worldwide.

Fiberglass, Mineral Wool, Cellular Glass, Polyurethane, Polystyrene, Others in the Industrial Pipe Insulation Materials - Global Market:

Fiberglass is one of the most commonly used materials in industrial pipe insulation due to its excellent thermal insulation properties and cost-effectiveness. It is made from fine strands of glass and is known for its ability to withstand high temperatures, making it suitable for a variety of industrial applications. Fiberglass insulation is lightweight, easy to install, and provides good resistance to moisture and chemicals, which enhances its durability in harsh environments. Mineral wool, another popular insulation material, is made from natural or synthetic minerals and offers superior fire resistance and sound absorption properties. It is often used in applications where fire safety is a critical concern, such as in chemical plants and power stations. Mineral wool is also effective in reducing noise pollution, making it a preferred choice in industries where noise control is important. Cellular glass is a rigid insulation material known for its excellent moisture resistance and compressive strength. It is often used in applications where moisture control is essential, such as in oil and gas pipelines. Cellular glass is also resistant to most chemicals, making it suitable for use in aggressive environments. Polyurethane is a versatile insulation material that offers high thermal resistance and low thermal conductivity. It is commonly used in applications where space is limited, as it provides effective insulation with a relatively thin layer. Polyurethane insulation is also lightweight and easy to handle, which makes it a popular choice in various industrial settings. Polystyrene, available in both expanded and extruded forms, is known for its excellent moisture resistance and thermal insulation properties. It is often used in applications where water resistance is a priority, such as in food and beverage processing plants. Polystyrene insulation is also lightweight and easy to cut, which simplifies installation. Other materials used in industrial pipe insulation include aerogel, calcium silicate, and elastomeric foam, each offering unique benefits and applications. Aerogel is known for its exceptional thermal insulation properties and is often used in high-temperature applications. Calcium silicate is valued for its high compressive strength and durability, making it suitable for heavy-duty industrial applications. Elastomeric foam is flexible and provides good resistance to moisture and UV radiation, making it ideal for outdoor applications. Each of these materials plays a vital role in the industrial pipe insulation market, offering solutions tailored to specific needs and requirements.

Chemical, Food & Beverages, Oil & Gas, Power, Metal Manufacturing, Other Industrial in the Industrial Pipe Insulation Materials - Global Market:

Industrial pipe insulation materials are used extensively across various sectors to enhance efficiency, safety, and sustainability. In the chemical industry, these materials are crucial for maintaining the temperature of chemical processes, preventing heat loss, and ensuring the safe transport of hazardous substances. Proper insulation helps in reducing energy consumption and minimizing the risk of accidents due to temperature fluctuations. In the food and beverages industry, pipe insulation is essential for maintaining the quality and safety of products. It helps in preserving the temperature of food and beverage products during processing and transport, ensuring that they remain fresh and safe for consumption. Insulation also plays a role in preventing condensation, which can lead to contamination and spoilage. The oil and gas industry relies heavily on pipe insulation to maintain the temperature of fluids and gases during extraction, processing, and transport. Insulation helps in preventing heat loss, reducing energy consumption, and ensuring the safe operation of pipelines. It also plays a role in preventing the formation of hydrates and waxes, which can clog pipelines and disrupt operations. In the power industry, pipe insulation is used to improve the efficiency of power plants by reducing heat loss and conserving energy. It helps in maintaining the temperature of steam and other fluids used in power generation, ensuring optimal performance and reducing operational costs. In metal manufacturing, pipe insulation is used to maintain the temperature of molten metals and other materials during processing. It helps in reducing energy consumption and ensuring the quality of the final product. Other industrial sectors, such as pharmaceuticals and textiles, also use pipe insulation to enhance efficiency and safety. In pharmaceuticals, insulation helps in maintaining the temperature of sensitive materials and processes, ensuring product quality and safety. In textiles, insulation is used to maintain the temperature of dyes and other materials, ensuring consistent quality and reducing energy consumption. Overall, industrial pipe insulation materials play a vital role in enhancing the efficiency, safety, and sustainability of various industrial operations.

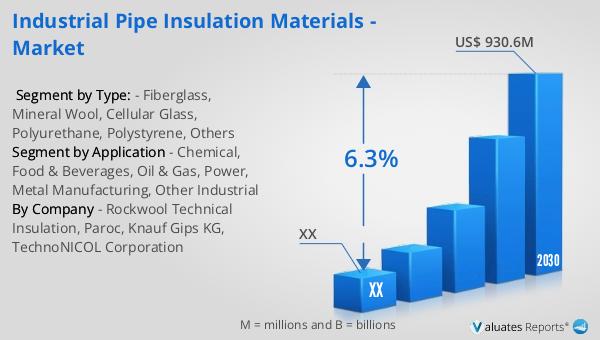

Industrial Pipe Insulation Materials - Global Market Outlook:

The global market for industrial pipe insulation materials was valued at approximately $624 million in 2023. It is projected to grow significantly, reaching an estimated size of $930.6 million by 2030, with a compound annual growth rate (CAGR) of 6.3% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for energy-efficient solutions and the need to comply with environmental regulations across various industries. The North American market for industrial pipe insulation materials is also expected to experience growth during this period. Although specific figures for the North American market in 2023 and 2030 are not provided, it is anticipated to follow a similar upward trend, driven by advancements in insulation technology and the growing emphasis on energy conservation. The market's expansion is supported by the rising awareness of the benefits of pipe insulation in reducing energy consumption and operational costs. As industries continue to prioritize sustainability and efficiency, the demand for high-performance insulation materials is expected to increase, contributing to the overall growth of the global market. This positive outlook reflects the critical role that industrial pipe insulation materials play in supporting industrial operations and promoting energy conservation worldwide.

| Report Metric | Details |

| Report Name | Industrial Pipe Insulation Materials - Market |

| Forecasted market size in 2030 | US$ 930.6 million |

| CAGR | 6.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Rockwool Technical Insulation, Paroc, Knauf Gips KG, TechnoNICOL Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |