What is Global Medicine Transportation Service Market?

The Global Medicine Transportation Service Market is a crucial component of the healthcare supply chain, ensuring that medicines and medical supplies are delivered safely and efficiently to various destinations worldwide. This market encompasses a range of services and solutions designed to transport pharmaceutical products, including prescription drugs, vaccines, and over-the-counter medications, from manufacturers to distributors, pharmacies, hospitals, and clinics. The transportation of these products requires specialized logistics to maintain their efficacy and safety, particularly for temperature-sensitive items. The market is driven by the increasing demand for pharmaceuticals, advancements in healthcare infrastructure, and the globalization of the pharmaceutical industry. Companies operating in this market must adhere to stringent regulations and standards to ensure the integrity of the products during transit. The market is also influenced by technological advancements, such as real-time tracking systems and automated logistics solutions, which enhance the efficiency and reliability of medicine transportation. Overall, the Global Medicine Transportation Service Market plays a vital role in ensuring that patients worldwide have timely access to essential medications, contributing to improved health outcomes and quality of life.

Cold Chain Transportation, Non-cold Chain Transportation in the Global Medicine Transportation Service Market:

Cold Chain Transportation and Non-cold Chain Transportation are two critical components of the Global Medicine Transportation Service Market, each serving distinct purposes based on the specific requirements of pharmaceutical products. Cold Chain Transportation refers to the transportation of temperature-sensitive medicines that require a controlled environment to maintain their stability and efficacy. This includes vaccines, biologics, and certain types of insulin, which must be kept within a specific temperature range throughout the supply chain. The cold chain involves a series of refrigerated production, storage, and distribution activities, supported by specialized equipment such as refrigerated trucks, containers, and warehouses. Maintaining the cold chain is essential to prevent degradation of the products, which could render them ineffective or even harmful. Advanced technologies, such as temperature monitoring devices and data loggers, are employed to ensure compliance with temperature requirements and to provide real-time visibility into the condition of the products during transit. On the other hand, Non-cold Chain Transportation involves the movement of pharmaceutical products that do not require temperature control. These include most oral solid dosage forms, such as tablets and capsules, which are stable at ambient temperatures. While the logistics for non-cold chain products are less complex compared to cold chain, they still require careful handling to prevent physical damage and contamination. Proper packaging, secure loading, and adherence to regulatory guidelines are essential to ensure the safe delivery of these products. Both cold chain and non-cold chain transportation are integral to the pharmaceutical supply chain, each addressing the unique needs of different types of medicines. The choice between the two depends on the nature of the product, its stability profile, and the regulatory requirements governing its transportation. As the demand for pharmaceuticals continues to grow, the Global Medicine Transportation Service Market is expected to expand, with cold chain logistics playing an increasingly important role due to the rising prevalence of biologics and personalized medicines. Companies operating in this market must invest in infrastructure, technology, and training to meet the evolving needs of the industry and to ensure the safe and efficient delivery of medicines to patients worldwide.

Hospital, Clinic in the Global Medicine Transportation Service Market:

The usage of the Global Medicine Transportation Service Market in hospitals and clinics is pivotal in ensuring that healthcare providers have timely access to the medications and medical supplies they need to deliver effective patient care. In hospitals, the transportation service is crucial for maintaining an uninterrupted supply of a wide range of pharmaceuticals, from routine medications to critical care drugs. Hospitals rely on these services to receive regular shipments of medicines, which are essential for treating patients with various medical conditions. The transportation service ensures that these medicines are delivered in optimal condition, preserving their efficacy and safety. For temperature-sensitive drugs, cold chain transportation is employed to maintain the required temperature throughout the supply chain, preventing any compromise in the quality of the medicines. In clinics, the transportation service plays a similar role, albeit on a smaller scale. Clinics often have limited storage capacity and rely on frequent deliveries to maintain their stock of essential medicines. The transportation service ensures that clinics receive their supplies promptly, enabling them to provide continuous care to their patients. This is particularly important for clinics in remote or underserved areas, where access to medicines can be a challenge. The transportation service helps bridge this gap, ensuring that patients in these areas have access to the medications they need. Additionally, the transportation service supports the distribution of vaccines and other preventive medicines, which are critical for public health initiatives. By ensuring the safe and efficient delivery of these products, the transportation service contributes to the success of vaccination programs and other health campaigns. Overall, the Global Medicine Transportation Service Market is an indispensable part of the healthcare system, supporting hospitals and clinics in their mission to provide high-quality care to patients. By facilitating the timely and safe delivery of medicines, the transportation service helps healthcare providers meet the needs of their patients, ultimately improving health outcomes and enhancing the quality of life for individuals and communities.

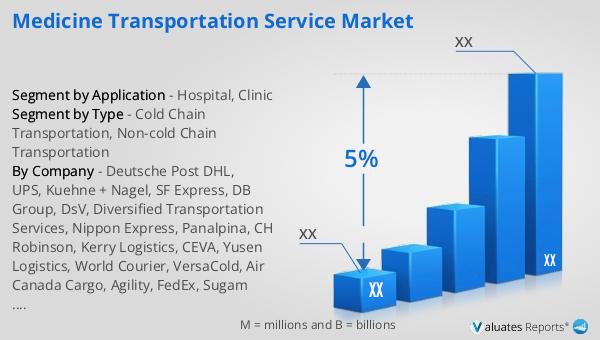

Global Medicine Transportation Service Market Outlook:

The outlook for the Global Medicine Transportation Service Market is closely tied to the trends and dynamics of the broader pharmaceutical industry. As of 2022, the global pharmaceutical market is valued at approximately 1,475 billion USD, with a projected compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for pharmaceutical products, driven by factors such as an aging population, the prevalence of chronic diseases, and advancements in medical research and development. In comparison, the chemical drug market, which forms a significant part of the pharmaceutical industry, has shown a steady increase from 1,005 billion USD in 2018 to 1,094 billion USD in 2022. This growth reflects the ongoing innovation and development of new chemical entities, as well as the expansion of existing drug portfolios. The transportation service market is expected to benefit from these trends, as the need for efficient and reliable logistics solutions becomes more critical. As pharmaceutical companies continue to expand their global reach, the demand for specialized transportation services that can ensure the safe and timely delivery of medicines will likely increase. This includes both cold chain and non-cold chain logistics, each addressing the specific needs of different types of pharmaceutical products. The transportation service market will need to adapt to the evolving requirements of the pharmaceutical industry, investing in technology and infrastructure to enhance the efficiency and reliability of their services. By doing so, the market can support the growth of the pharmaceutical industry and contribute to improved health outcomes for patients worldwide.

| Report Metric | Details |

| Report Name | Medicine Transportation Service Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Deutsche Post DHL, UPS, Kuehne + Nagel, SF Express, DB Group, DsV, Diversified Transportation Services, Nippon Express, Panalpina, CH Robinson, Kerry Logistics, CEVA, Yusen Logistics, World Courier, VersaCold, Air Canada Cargo, Agility, FedEx, Sugam Group, ARK Cryo, Expak Logistics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |